Earn To Die 2102 Part 2

2.1 Global income inequality dynamics

The information in this chapter draws on "The Elephant Curve of Global Inequality and Growth," by Facundo Alvaredo, Lucas Chancel, Thomas Piketty, Emmanuel Saez, and Gabriel Zucman, 2017. WID.world Working Paper Series (No. 2017/20), forthcoming in American Economic Association Papers and Proceedings.

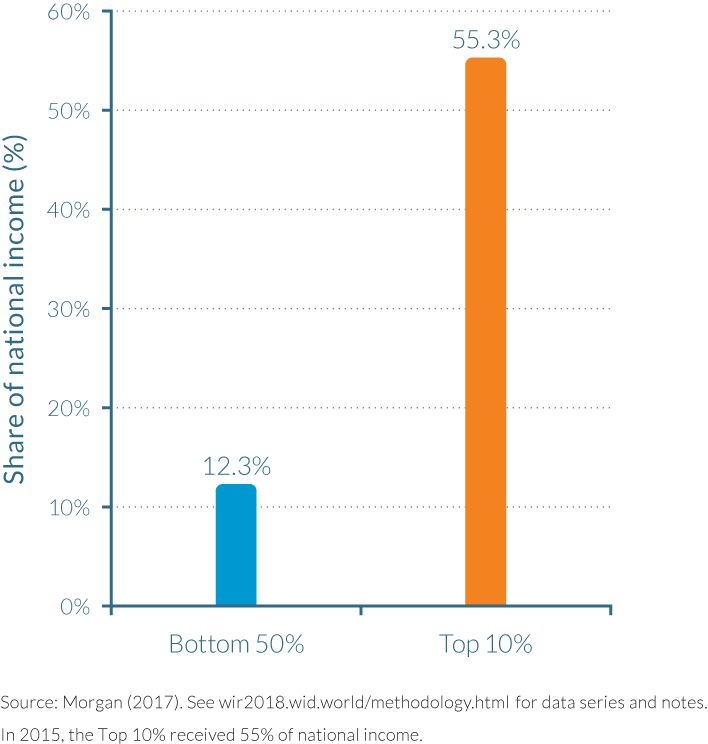

- Data series on global inequality are scarce and caution is required in interpreting them. However, by combining consistent and comparable data, as we have done in this World Inequality Report, we can provide striking insights.

- Since 1980, income inequality has increased rapidly in North America and Asia, grown moderately in Europe, and stabilized at an extremely high level in the Middle East, sub-Saharan Africa, and Brazil.

- The poorest half of the global population has seen its income grow significantly thanks to high growth in Asia. But the top 0.1% has captured as much growth as the bottom half of the world adult population since 1980.

- Income growth has been sluggish or even nil for individuals between the global bottom 50% and top 1%. This includes North American and European lower- and middle-income groups.

- The rise of global inequality has not been steady. While the global top 1% income share increased from 16% in 1980 to 22% in 2000, it declined slightly thereafter to 20%. The trend break after 2000 is due to a reduction in between-country average income inequality, as within-country inequality has continued to increase.

- When measured using market exchange rates, the top 10% share reaches 60% today, instead of 53% when using purchasing power parity (PPP) exchange rates.

- Global income growth dynamics are driven by strong forces of convergence between countries and divergence within countries. Standard economic trade models fail to explain these dynamics properly—in particular, the rise of inequality at the very top and within emerging countries. Global dynamics are shaped by a variety of national institutional and political contexts, described and discussed in the following chapters of this report.

Managing data limitations to construct a global distribution of income

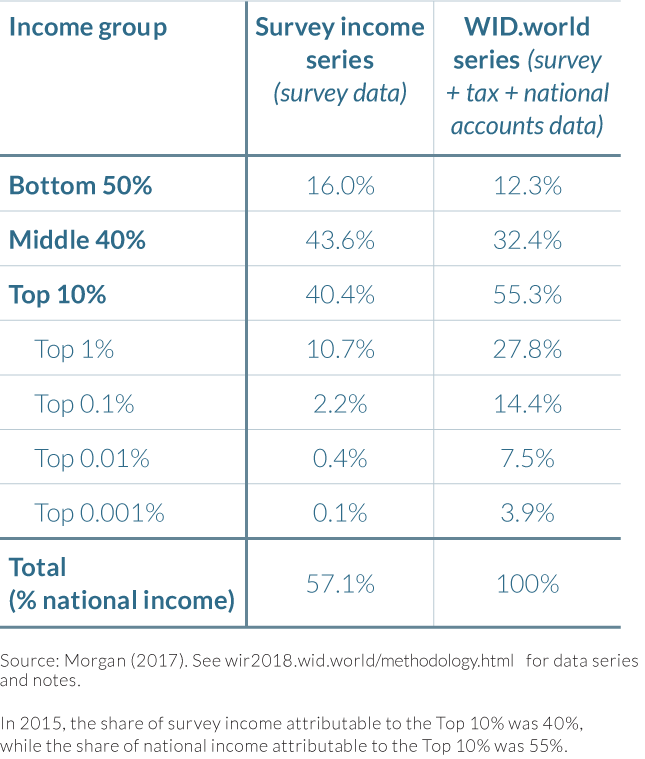

The dynamics of global inequality have attracted growing attention in recent years.1 However, we still know relatively little about how the distribution of global income and wealth is evolving. Available studies have largely relied on household surveys, a useful source of information, but one that does not accurately track the evolution of inequality at the top of the distribution. New methodological and empirical work carried out in the context of WID.world allows a better understanding of global income dynamics.

We stress at the outset that the production of global inequality dynamics is in its infancy and will still require much more work. It is critical that national statistical and tax institutions release income and wealth inequality data in many countries where data are not available currently—in particular, in developing and emerging countries. Researchers also need to thoroughly harmonize and analyze these data to produce consistent, comparable estimates. The World Inequality Lab and the WID.world research consortium intend to continue contributing to these tasks in the coming years.

Even if there are uncertainties involved, it is already possible to produce meaningful global income inequality estimates. The WID.world database contains internationally comparable income inequality estimates covering the entire population, from the lowest to the highest income earners, for many countries: the United States, China, India, Russia, Brazil, the Middle East, and the major European countries (such as France, Germany, and the United Kingdom). A great deal can already be inferred by comparing inequality trends in these regions. Using simple assumptions, we have estimated the evolution of incomes in the rest of the world so as to distribute 100% of global income every year since 1980 (Box 2.1.1). This exercise should be seen as a first step towards the construction of a fully consistent global distribution of income. We plan to present updated and extended versions of these estimates in the future editions of the World Inequality Report and on WID.world, as we gradually manage to access more data sources, particularly in Africa, Latin America, and Asia.

Box 2.1.1

How did we construct global income inequality measures?

Global estimates in the World Inequality Report are based on a combination of sources used at the national level (including tax receipts, household surveys and national accounts as discussed in Part 1). Consistent estimates of national income inequality are now available for the USA, Western Europe (and in particular France, Germany, the United Kingdom) as well as China, India, Brazil, Russia and the Middle East. These regions represent approximately two thirds of the world adult population and three quarters of global income.

In this chapter on global income inequality, we have ultimately distributed the totality of global income, to the totality of the world population. To achieve this, we had to distribute the quarter of global income to the third of the global population for which there is currently no consistent income inequality data available. One crucial information we have, however, is total national income in each country. This information is essential, as it already determines a large part of global income inequality among individuals.

How then to distribute national income to individuals in countries without inequality data? We tested different ways and found that these had very moderate impacts on the distribution of global income, given the limited share of income and population concerned by these assumptions. In the end, we assumed that countries with missing inequality information had similar levels of inequality as other countries in their region. Take an example, we know the average income level in Malaysia, but not (yet) how national income is distributed to all individuals in this country. We then assumed that the distribution of income in Malaysia was the same, and followed the same trends, as in the region formed by China and India. This is indeed an over simplification, but to some extent this is an acceptable method as alternative assumptions have a limited impact on our general conclusions.

Sub-Saharan Africa is a particular case: we did not have any country with consistent income inequality data over the past decades (whereas in Asia we have consistent estimates for China and India, in Latin America, we have estimates for Brazil, etc.). For Sub-Saharan Africa, we thus relied on household surveys available from the World Bank (these estimates cover 70% of Sub-Saharan Africa's population and yet a higher proportion of the region's income). These surveys were matched with fiscal data available from WID.world so as to provide a better representation of inequality at the top of the social pyramid (see Part 1).

Doing so then allowed us to produce a global distribution of income. The methodology we followed is available on wir2018.wid.world, as well as all the computer codes we used, so as to allow anyone make alternative assumptions or contribute to extend this work. In future editions of the World Inequality Report, we will progressively expand the geographical coverage of our data.

a See L. Chancel and A. Gethin, "Building a global income distribution brick by brick", WID.world Technical Note, 2017/20 as well as L. Chancel. and L. Czajka. "Estimating the regional distribution of income in Sub-Saharan Africa". WID.world Technical Note, 2017/21.

The exploration of global inequality dynamics presented here starts in 1980, for two main reasons. First, 1980 corresponds to a turning point in inequality and redistributive policies in many countries. The early 1980s mark the start of a rising trend in inequality and major policy changes, both in the West (with the elections of Ronald Reagan and Margaret Thatcher, in particular) and in emerging economies (with deregulation policies in China and India). Second, 1980 is the date from which data become available for a large enough number of countries to allow a sound analysis of global dynamics.

We start by presenting our basic findings regarding the evolution of income inequality within the main world regions. Three main findings emerge.

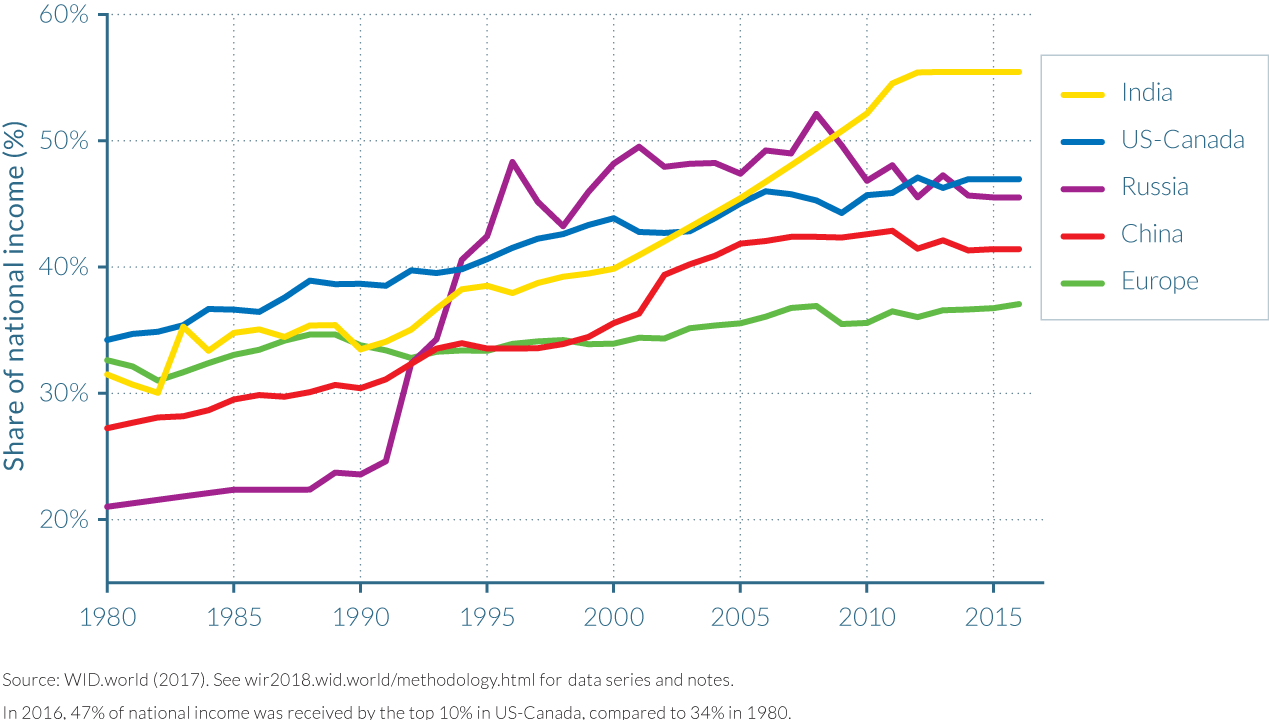

First, we observe rising inequality in most of the world's regions, but with very different magnitudes. More specifically, we display in Figure 2.1.1a the evolution of the top 10% income share in Europe (Western and Eastern Europe combined, excluding Ukraine, Belorussia, and Russia), North America (defined as the United States and Canada), China, India, and Russia. The top 10% share has increased in all five of these large world regions since 1980. The top 10% share was around 30–35% in Europe, North America, China, and India in 1980, and only about 20–25% in Russia. If we put these 1980 inequality levels into broader and longer perspective, we find that they were in place since approximately the Second World War, and that these are relatively low inequality levels by historical standards (Piketty, 2014). In effect, despite their many differences, all these world regions went through a relatively egalitarian phase between 1950 and 1980. For simplicity, and for the time being, this relatively low inequality regime can be described as the "post-war egalitarian regime," with obvious important variations between social-democratic, New Deal, socialist, and communist variants to which we will return.

Figure 2.1.1a

Top 10% income shares across the world, 1980–2016: Rising inequality almost everywhere, but at different speeds

Top 10% income shares then increased in all these regions between 1980 and 2016, but with large variations in magnitude. In Europe, the rise was moderate, with the top 10% share increasing to about 35–40% by 2016. However, in North America, China, India, and even more so in Russia (where the change in policy regime was particularly dramatic), the rise was much more pronounced. In all these regions, the top 10% share rose to about 45–50% of total income in 2016. The fact that the magnitude of rising inequality differs substantially across regions suggests that policies and institutions matter: rising inequality cannot be viewed as a mechanical, deterministic consequence of globalization.

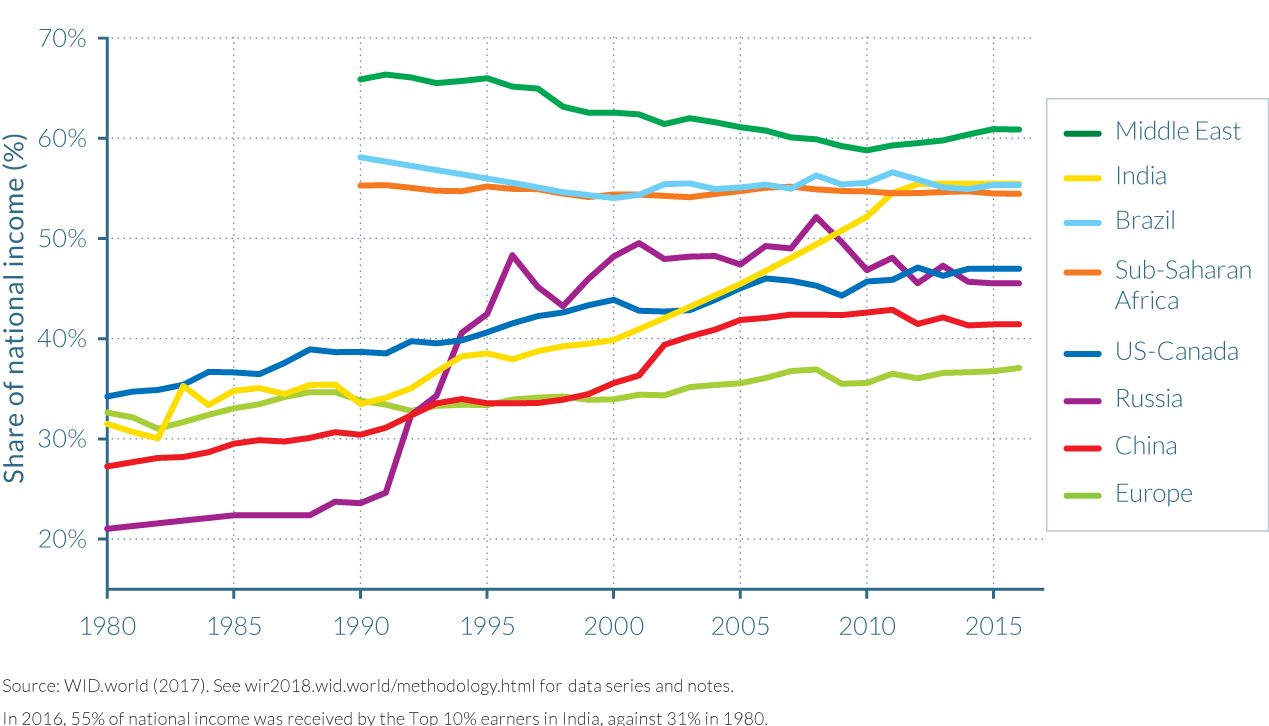

Next, there are exceptions to this general pattern. That is, there are regions—in particular, the Middle East, Brazil (and to some extent Latin America as a whole), and South Africa (and to some extent sub-Saharan Africa as a whole)—where income inequality has remained relatively stable at extremely high levels in recent decades. Unfortunately, data availability is more limited for these three regions, which explains why the series start in 1990, and why we are not able to properly cover all countries in these regions (see Figure 2.1.1b).

Figure 2.1.1b

Top 10% income shares across the world, 1980–2016: Is world inequality moving toward the high-inequality frontier?

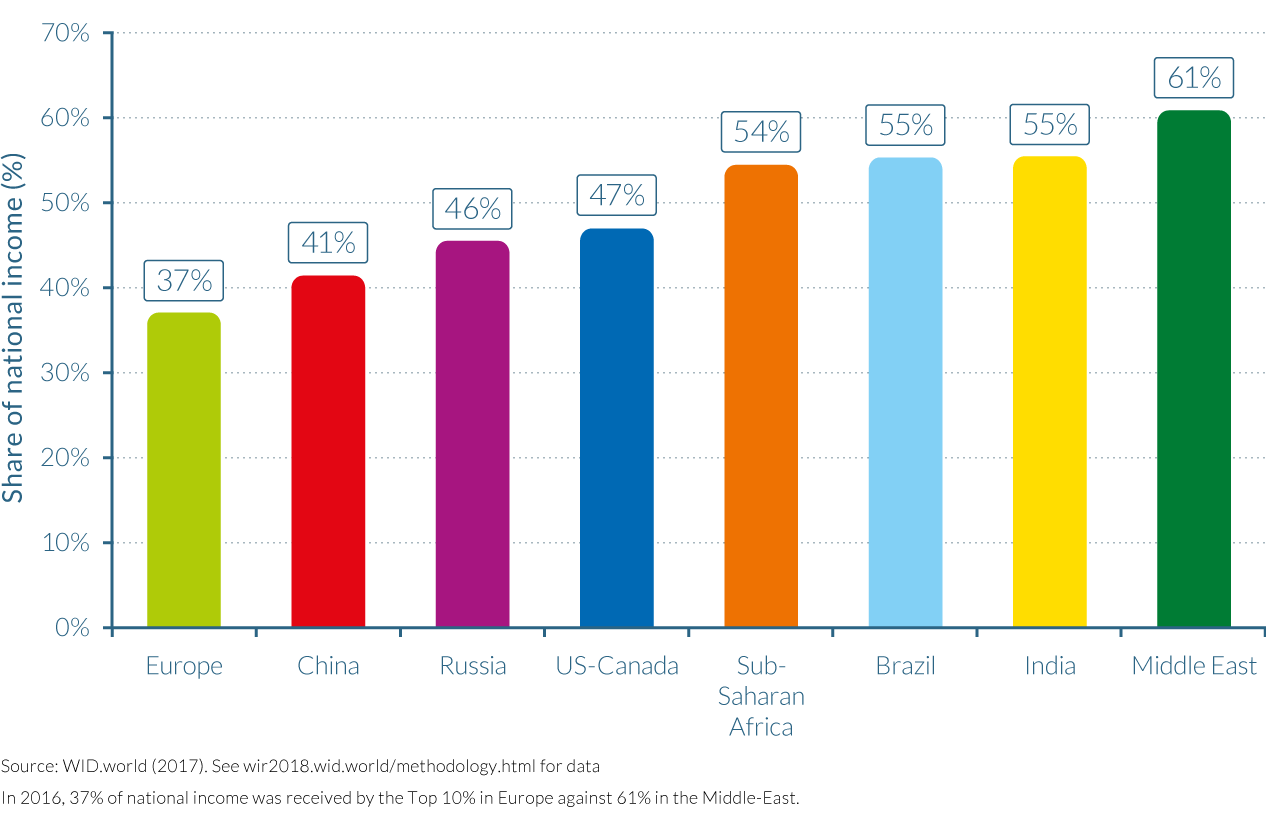

In spite of their many differences, the striking commonality in these three regions is the extreme and persistent level of inequality. The top 10% receives about 55% of total income in Brazil and sub-Saharan Africa, and in the Middle East, the top 10% income share is typically over 60% (see Figure 2.1.1c). In effect, for various historical reasons, these three regions never went through the post-war egalitarian regime and have always been at the world's high-inequality frontier.

Figure 2.1.1c

Top 10% income shares across the world, 2016

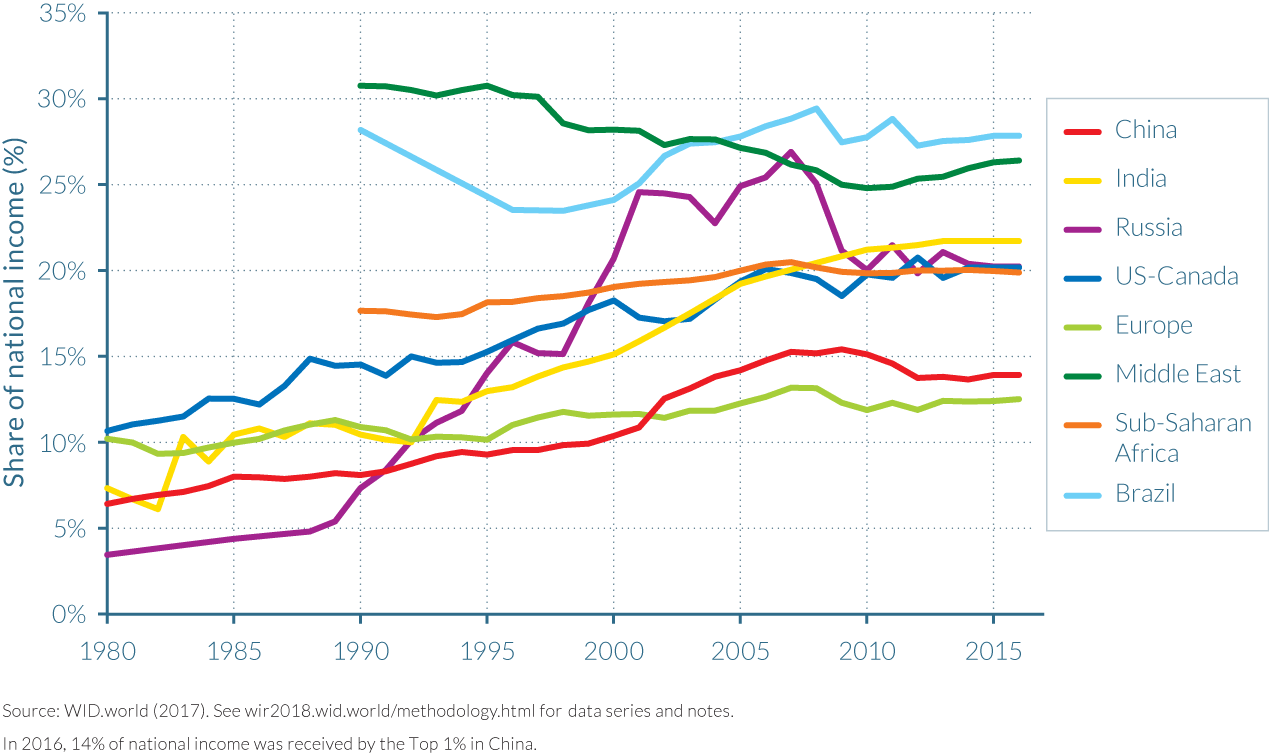

The third striking finding is that the variations in top-income shares over time and across countries are very large in magnitude, and have a major impact on the income shares and levels of the bottom 50% of the population. It is worth keeping in mind the following orders of magnitude: top 10% income shares vary from 20–25% to 60–65% of total income (see Figures 2.1.1a and 2.1.1b). If we focus upon very top incomes, we find that top 1% income shares vary from about 5% to 30% (see Figure 2.1.1d), just like the share of income going to the bottom 50% of the population (see Figure 2.1.1e).

Figure 2.1.1d

Top 1% income shares across the world, 1980–2016

Figure 2.1.1e

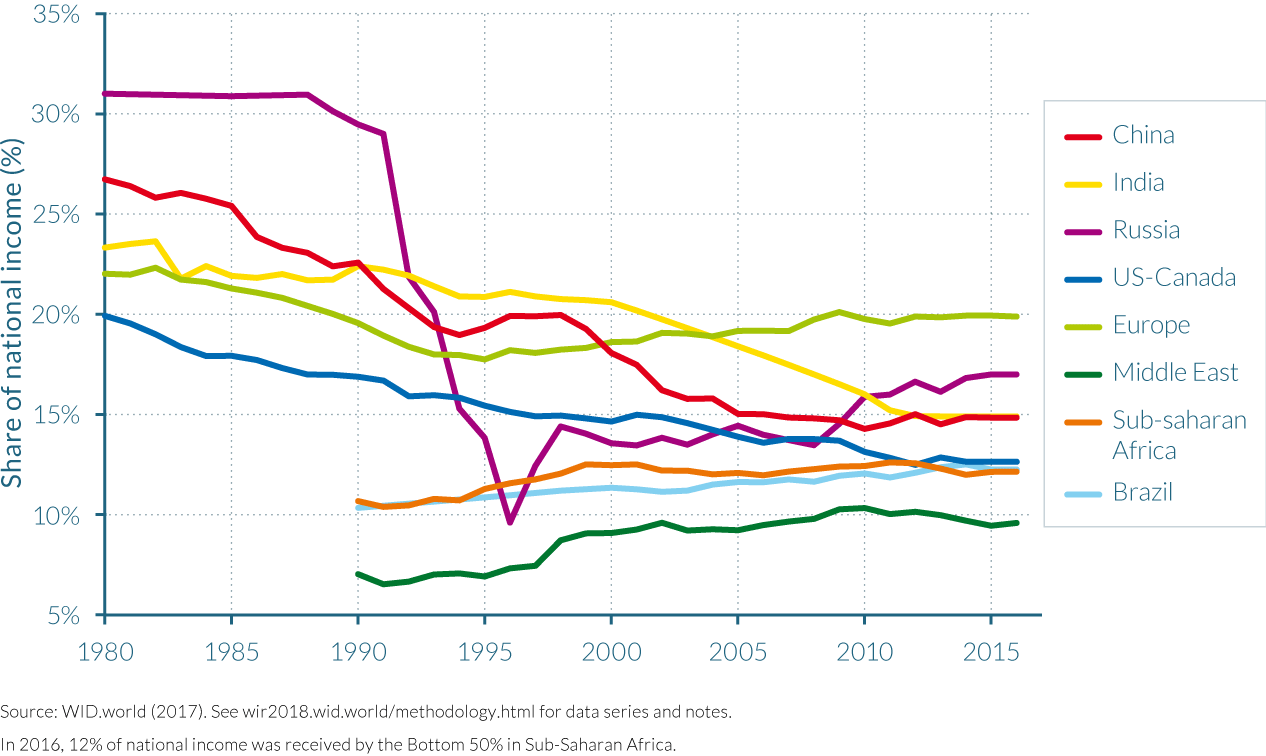

Bottom 50% income shares across the world, 1980–2016

In other words, the same aggregate income level can give rise to widely different income levels for the bottom and top groups depending on the distribution of income prevailing in the specific country and time period under consideration. In brief, the distribution matters quite a bit.

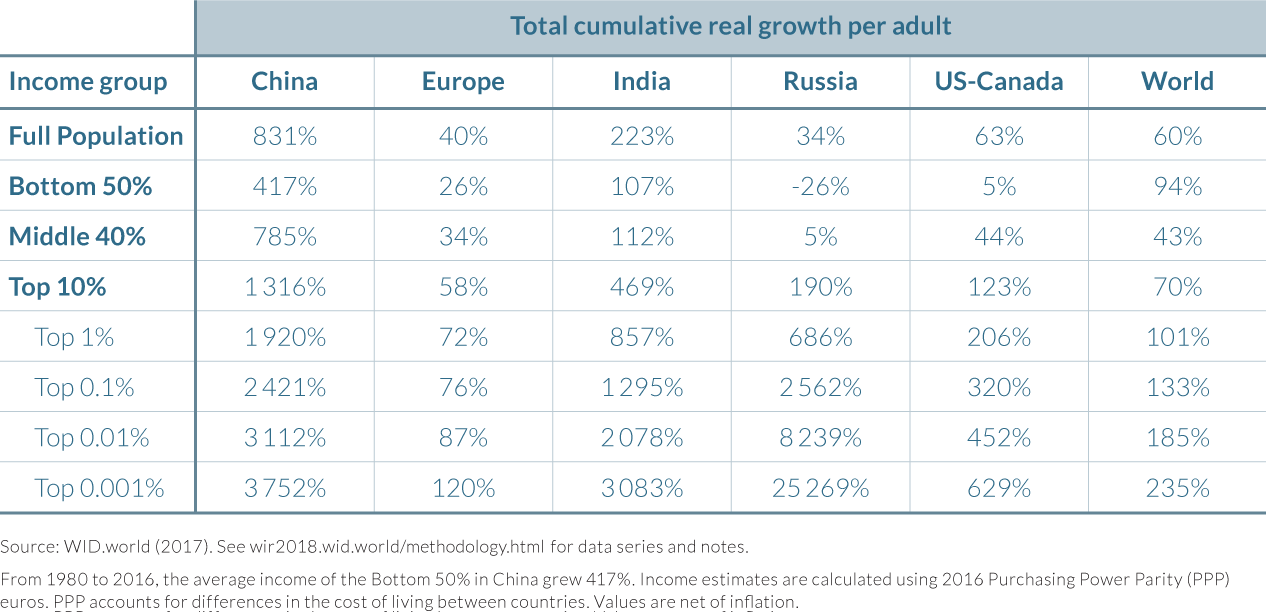

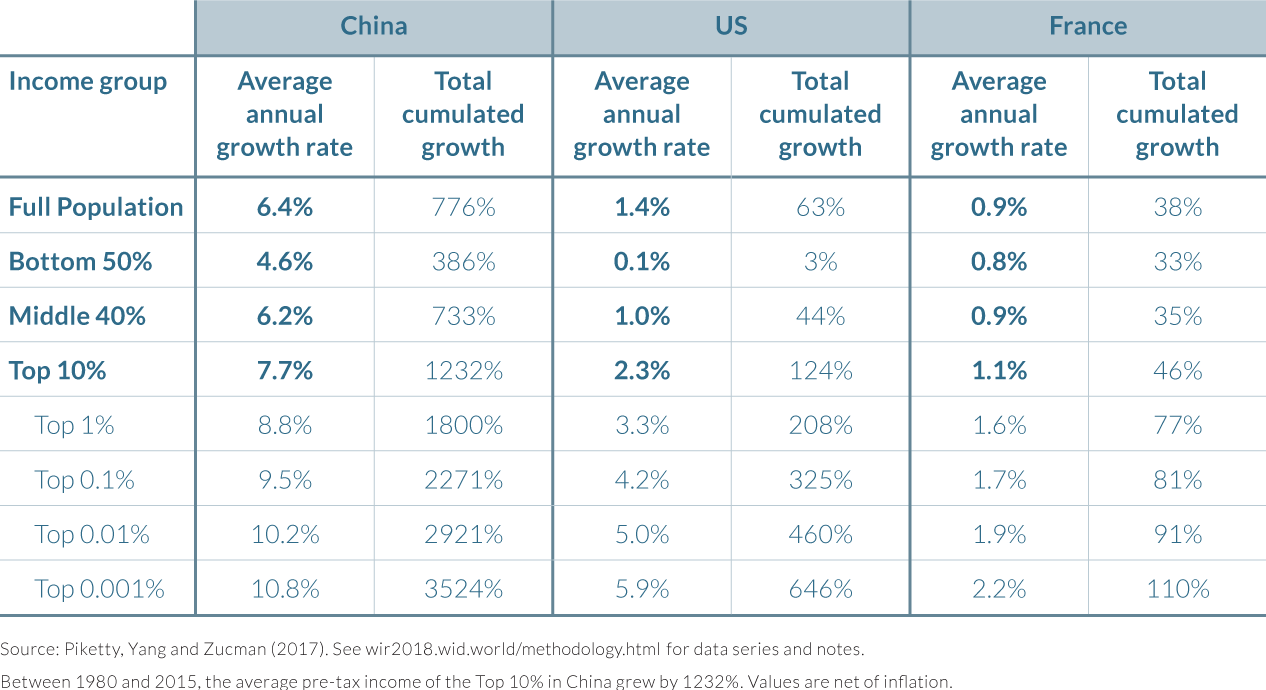

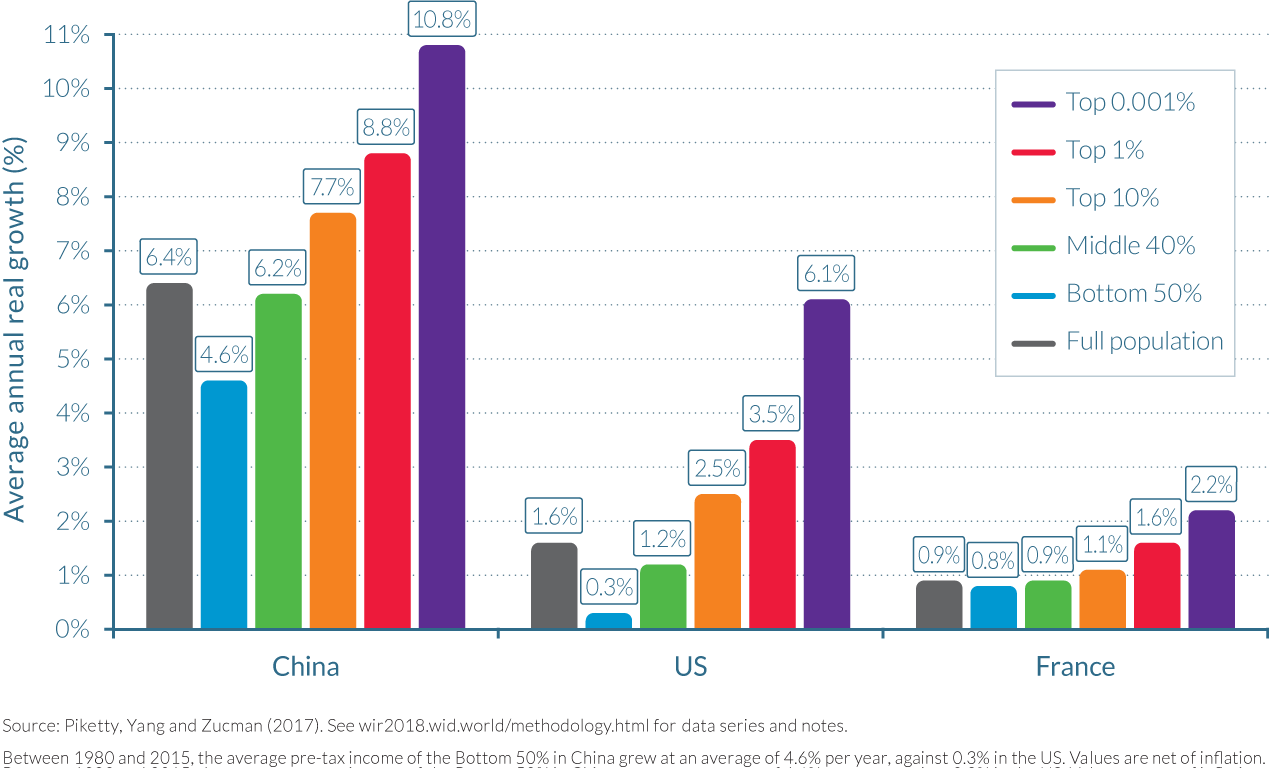

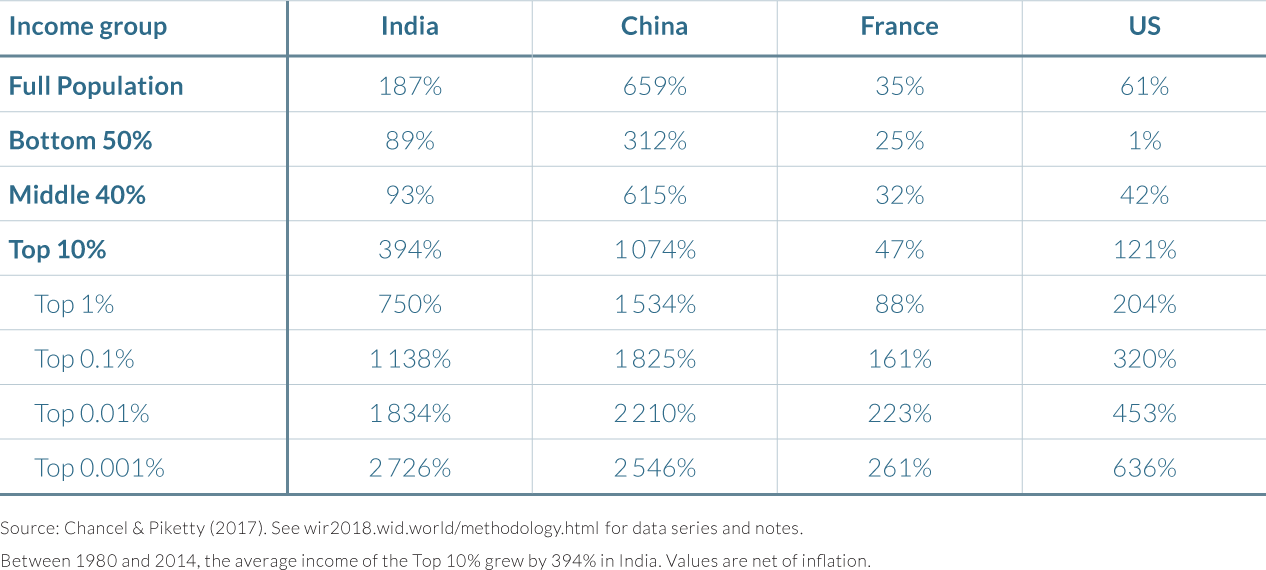

What have been the growth trajectories of different income groups in these regions since 1980? Table 2.1.1 presents income growth rates in China, Europe, India, Russia, and North America for key groups of the distribution. The full population grew at very different rates in the five regions. Real per-adult, national income growth reached an impressive 831% in China and 223% in India. In Europe, Russia, and North America, income growth was lower than 100% (40%, 34%, and 74%, respectively). Behind these heterogeneous average growth trajectories, the different regions all share a common, striking characteristic.

Table 2.1.1

Global income growth and inequality, 1980–2016

In all these countries, income growth is systematically higher for upper income groups. In China, the bottom 50% earners grew at less than 420% while the top 0.001% grew at more than 3 750%. The gap between the bottom 50% and the top 0.001% is even more important in India (less than 110% versus more than 3 000%). In Russia, the top of the distribution had extreme growth rates; this reflects the shift from a regime in which top incomes were constrained by the communist system towards a market economy with few regulations constraining top incomes. In this global picture, in line with Figure 2.1.1, Europe stands as the region with the lowest growth gap between the bottom 50% and the full population, and with the lowest growth gap between the bottom 50% and top 0.001%.

The right-hand column of table 2.1.1 presents income growth rates of different groups at the level of the entire world. These growth rates are obtained once all the individuals of the different regions are pooled together to reconstruct global income groups. Incomes across countries are compared using purchasing power parity (PPP) so that a given income can in principle buy the same bundle of goods and services in all countries. Average global growth is relatively low (60%) compared to emerging countries' growth rates. Interestingly enough, at the world level, growth rates do not rise monotonically with income groups' positions in the distribution. Instead, we observe high growth at the bottom 50% (94%), low growth in the middle 40% (43%), and high growth at the top 1% (more than 100%)—and especially at the top 0.001% (close to 235%).

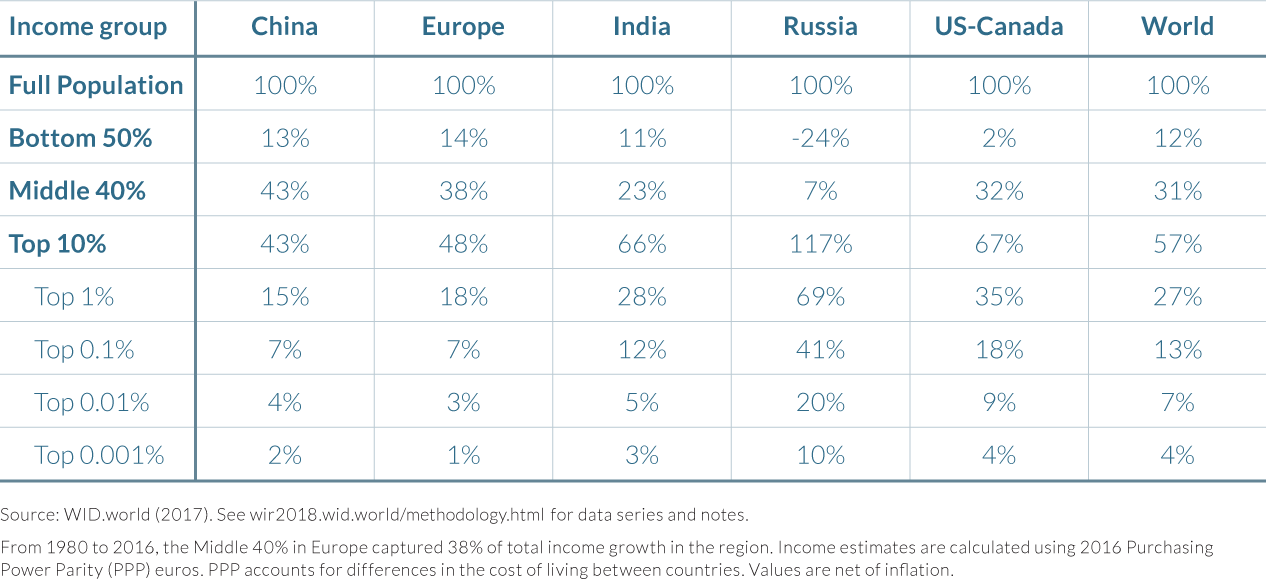

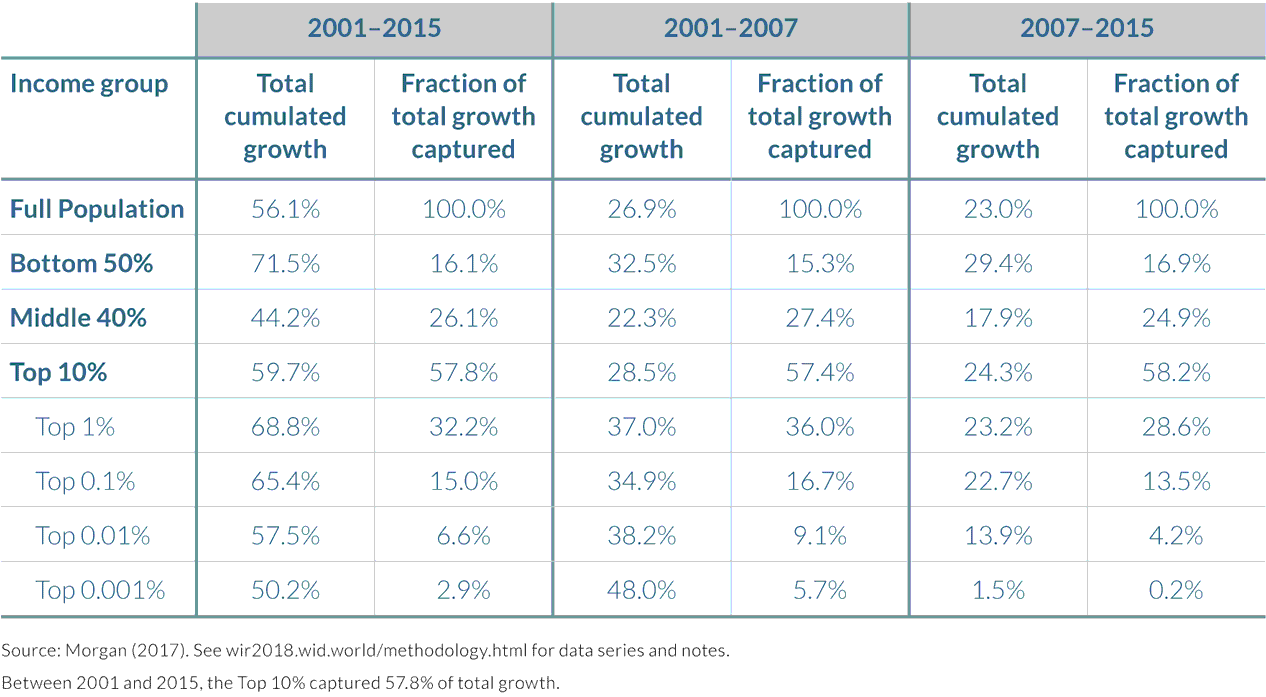

To better understand the significance of these unequal rates of growth, it is useful to focus on the share of total growth captured by each group over the entire period. Table 2.1.2 presents the share of growth per adult captured by each group. Focusing on both metrics is important because the top 1% global income group could have enjoyed a substantial growth rate of more than 100% over the past four decades (meaningful at the individual level), but still represent only a little share of total growth. The top 1% captured 35% of total growth in the US-Canada, and an astonishing 69% in Russia.

Table 2.1.2

Share of global growth captured by income groups, 1980–2016

At the global level, the top 1% captured 27% of total growth—that is, twice as much as the share of growth captured by the bottom 50%. The top 0.1% captured about as much growth as the bottom half of the world population. Therefore, the income growth captured by very top global earners since 1980 was very large, even if demographically they are a very small group.

Building a global inequality distribution brick by brick

A powerful way to visualize the evolution of global income inequality dynamics is to plot the total growth rate of each income groups (see Box 2.1.2). This provides a more precise representation of growth dynamics than Table 2.1.1. To properly understand the role played by each region in global inequality dynamics, we follow a step-by-step approach to construct this global growth curve by adding one region after another and discussing each step of the exercise.

Box 2.1.2

Interpreting inequality graphs in this report

Total growth curves (or "growth incidence curves") shed light on the income growth rate of each income group in a given country or at the world level. The popularization of such graphs is largely due to their use by Christoph Lakner and Branko Milanovic. In this report we are able to provide novel insights on global income dynamics thanks to the new inequality series constructed in WID.world (as detailed in Part 1). In particular, we are able to decompose the top 1% of the global distribution into smaller groups and observe their relative importance in total growth. If anything, our general conclusion is that the "elephant curve" is even more marked than what was initially pointed out by Lakner and Milanovic.

How to interpret these graphs? The horizontal axis sorts global income groups in ascending order from the poorest (left-hand side) to the richest (right-hand side). The first ninety-nine brackets correspond to each of the bottom ninety-nine percentiles of the global population. Each bracket represents 1% of the global population and occupies the same length on the graph. The global top 1% group is not represented on the same scale as the bottom 99%. We split it into twenty-eight smaller groups in the following way. The group is first split into ten groups of equal size (representing each 0.1% of the population). The richest of these groups is then itself split into ten groups of equal size (each representing 0.01% of the global population). The richest of these groups is again split into ten groups of equal size. The richest group represented on the horizontal axis (group 99.999) thus corresponds to the top 0.001% richest individuals in the world. This represents 49 000 individuals in 2016.

Each of these twenty-eight groups comprising the top 1% earners occupies the same space as percentiles of the bottom 99%. This is a simple way to represent clearly the importance of these groups in total income growth. The global top 1% group captured 27% of total growth from 1980 to 2016—that is, about a quarter of total growth. On the horizontal axis, this group occupies about a quarter of the scale.

There are other ways to scale percentiles on the horizontal axis. Appendices A2.1 and A2.2 show two variants. In the first, each group occupies a space that is proportional to its population size; in effect, the 28 groups decomposing the top 1% are squeezed together. In the other, each group is given a segment that is proportional to its share of total growth captured. In this case, it is the groups at the bottom of the global distribution that are squeezed. Our benchmark representation is a combination of these two variants.

The vertical axis presents the total real pre-tax income growth rate for each of the 127 groups defined above. Real income means that incomes are corrected for inflation. "Pre-tax" refers to incomes before taxes and transfers (but after the operation of the pension system). Note that the values are presented as total growth rates over the period rather than as annualized growth rates, which are perhaps somewhat more common in economic debates. Over long time spans such as the 1980–2016 period analyzed here, it is generally more meaningful to discuss total growth rates than to discuss average annual growth rates. Because of the multiplicative power of growth rates, small differences in annualized growth rates lead to large differences in total growth rates over long time spans. To illustrate this, let us take two income groups whose incomes grow at 4% and 5% over thirty-five years, respectively. The first group does not grow as fast as the second one, but the difference may seem limited. In fact, over thirty-five years, the total income growth is 295% in the first case and 452% in the second, which indeed represents a substantial difference in terms of purchasing power and standards of living.

We start with the distribution of growth in a region regrouping Europe and North America (Figure 2.1.2). These two regions have a total of 880 million individuals in 2016 (520 million in Europe and 360 million in North America) and represent most of the population of high-income countries. In Euro-America, cumulative per-adult income growth over the 1980–2016 period was +28%, which is relatively low as compared to the global average (+66%). While the bottom 10% income group saw their income decrease over the period, all individuals between percentile 20 and percentile 80 had a growth rate close to the average growth rate. At the very top of the distribution, incomes grew very rapidly; individuals in the top 1% group saw their incomes rise by more than 100% over the time period and those in the top 0.01% and above grew at more than 200%.

Figure 2.1.2

Total income growth by percentile in US-Canada and Western Europe, 1980–2016

How did this translate into shares of growth captured by different groups? The top 1% of earners captured 28% of total growth—that is, as much growth as the bottom 81% of the population. The bottom 50% earners captured 9% of growth, which is less than the top 0.1%, which captured 14% of total growth over the 1980–2016 period. These values, however, hide large differences in the inequality trajectories followed by Europe and North America. In the former, the top 1% captured as much growth as the bottom 51% of the population, whereas in the latter, the top 1% captured as much growth as the bottom 88% of the population. (See chapter 2.3 for more details.)

The next step is to add the population of India and China to the distribution of Euro-America. The global region now considered represents 3.5 billion individuals in total (including 1.4 billion individuals from China and 1.3 billion from India). Adding India and China remarkably modifies the shape of the global growth curve (Figure 2.1.3).

Figure 2.1.3

Total income growth by percentile in China, India, US-Canada, and Western Europe, 1980–2016

The first half of the distribution is now marked by a "rising tide" as total income growth rates increase substantially from the bottom of the distribution to the middle. The bottom half of the population records growth rates which go as high as 260%, largely above the global average income growth of 146%. This is due to the fact that Chinese and Indians, who make up the bulk of the bottom half of this global distribution, enjoyed much higher growth rates than their European and North American counterparts. In addition, growth was also very unequally distributed in India and China, as revealed by Table 2.1.1.

Between percentiles 70 and 99 (individuals above the poorest 70% of the population but below the richest 1%), income growth was substantially lower than the global average, reaching only 40–50%. This corresponds to the lower- and middle-income groups in rich countries which grew at a very low rates. The extreme case of these is the bottom half of the population in the United States, which grew at only 3% over the period considered. (See Chapter 2.4.)

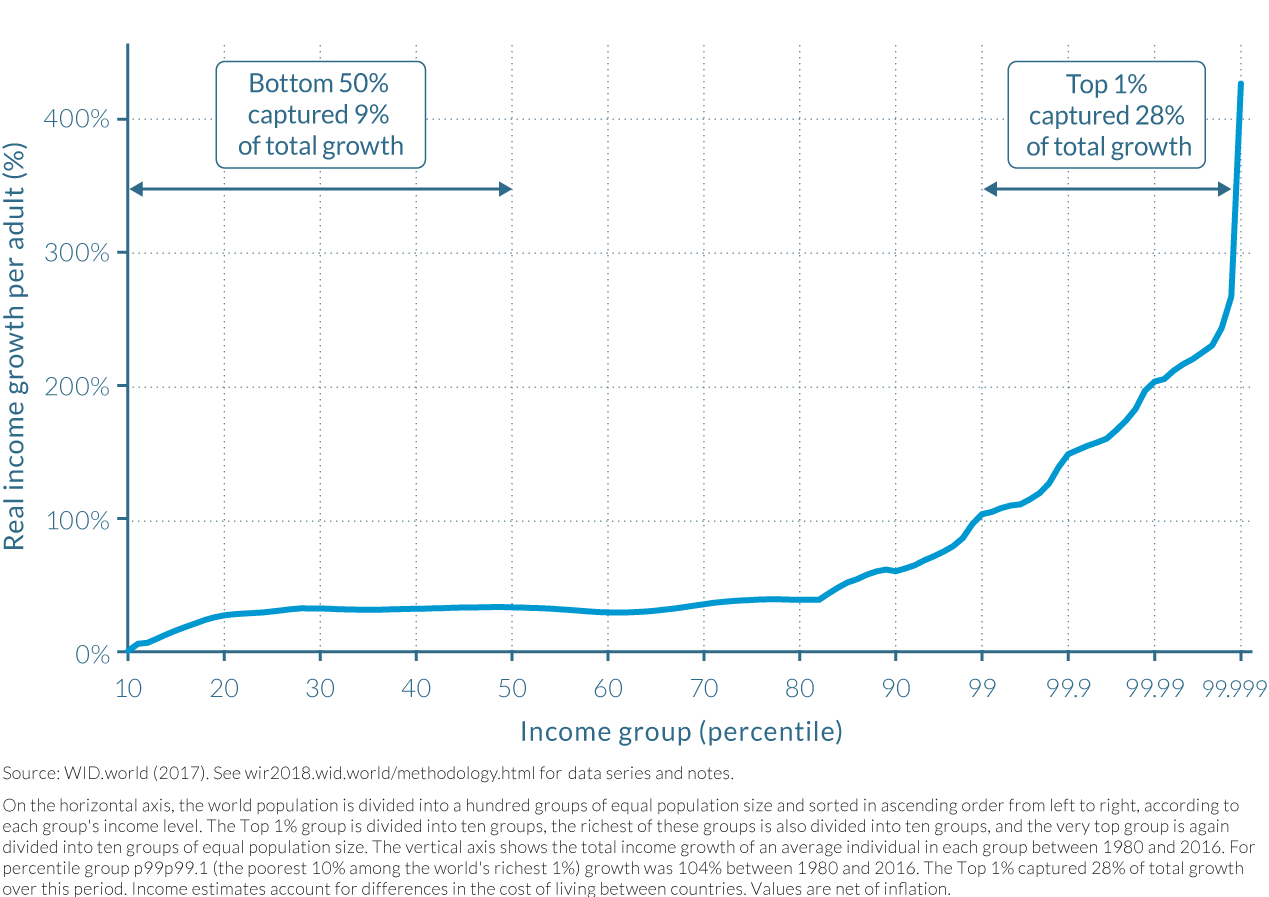

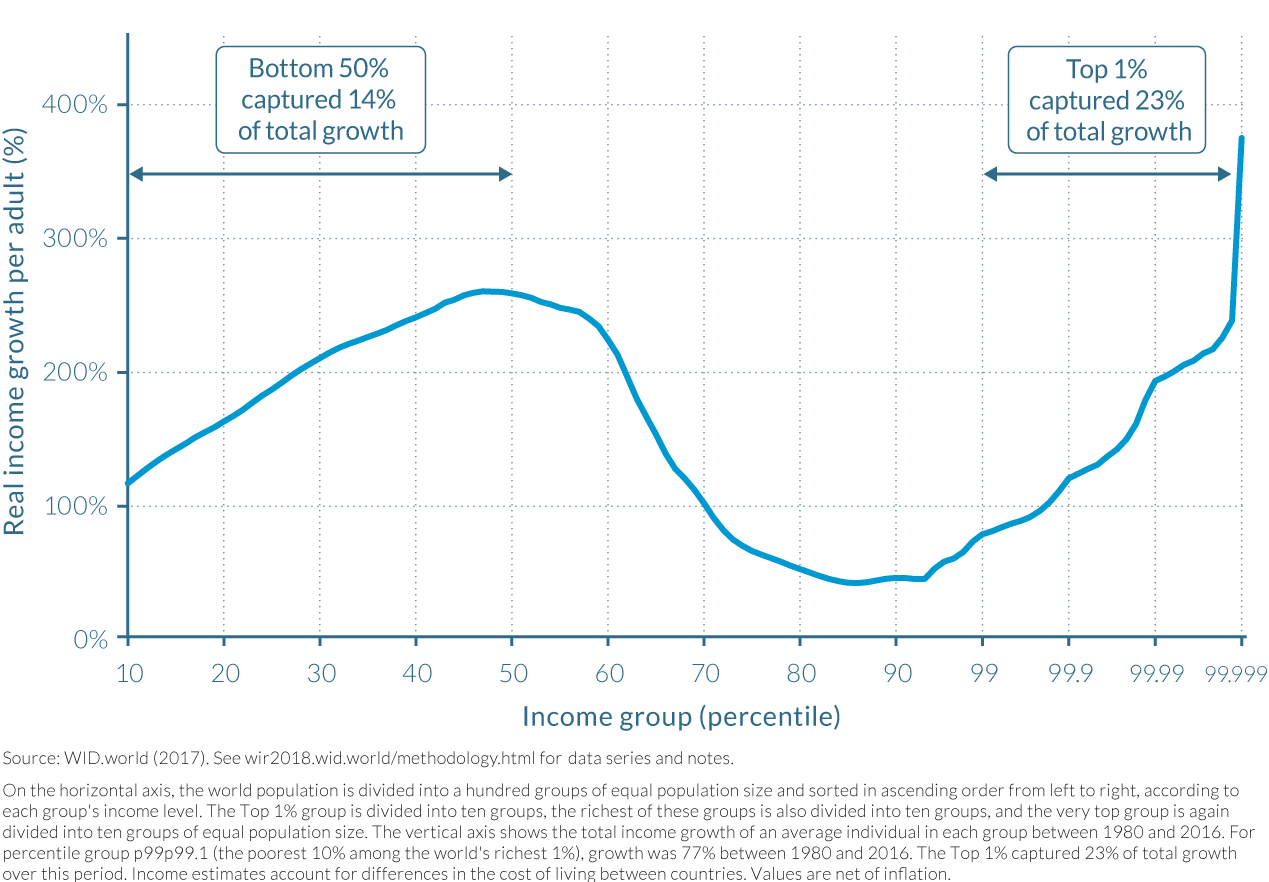

Earlier versions of this graph have been termed "the elephant curve," as the shape of the curve resembles the silhouette of the animal. These new findings confirm and amplify earlier results.2 In particular they make it possible to measure much more reliably the share of income growth captured at the top of the global income distribution—a figure which couldn't be properly measured before.

At the top of the global distribution, incomes grew extremely rapidly—around 200% for the top 0.01% and above 360% for the top 0.001%. Not only were these growth rates important from the perspective of individuals, they also matter a lot in terms of global growth. The top 1% captured 23% of total growth over the period—that is, as much as the bottom 61% of the population. Such figures help make sense of the very high growth rates enjoyed by Indians and Chinese sitting at the bottom of the distribution. Whereas growth rates were substantial among the global bottom 50%, this group captured only 14% of total growth, just slightly more than the global top 0.1%—which captured 12% of total growth. Such a small share of total growth captured by the bottom half of the population is partly due to the fact that when individuals are very poor, their incomes can double or triple but still remain relatively small—so that the total increase in their incomes does not necessarily add up at the global level. But this is not the only explanation. Incomes at the very top must also be extraordinarily high to dwarf the growth captured by the bottom half of the world population.

The next step of the exercise consists of adding the populations and incomes of Russia (140 million), Brazil (210 million), and the Middle East (410 million) to the analysis. These additional groups bring the total population now considered to more than 4.3 billion individuals—that is, close to 60% of the world total population and two thirds of the world adult population. The global growth curve presented in Appendix Figure A2.3 is similar to the previous one except that the "body of the elephant" is now shorter. This can be explained by the fact that Russia, the Middle East, and Brazil are three regions which recorded low growth rates over the period considered. Adding the population of the three regions also slightly shifts the "body of the elephant" to the left, since a large share of the population of the countries incorporated in the analysis is neither very poor nor very rich from a global point of view and thus falls in the middle of the distribution. In this synthetic global region, the top 1% earners captured 26% of total growth over the 1980–2016 period—that is, as much as the bottom 65% of the population. The bottom 50% captured 15% of total growth, more than the top 0.1%, which captured 12% of growth.

The final step consists of including all remaining global regions—namely, Africa (close to 1 billion individuals), the rest of Asia (another billion individuals), and the rest of Latin America (close to half a billion). In order to reconstruct income inequality dynamics in these regions, we take into account between-country inequality, for which information is available, and assume that within countries, growth is distributed in the same way as neighboring countries for which we have specific information (see Box 2.1.1). This allows us to distribute the totality of global income growth over the period considered to the global population.

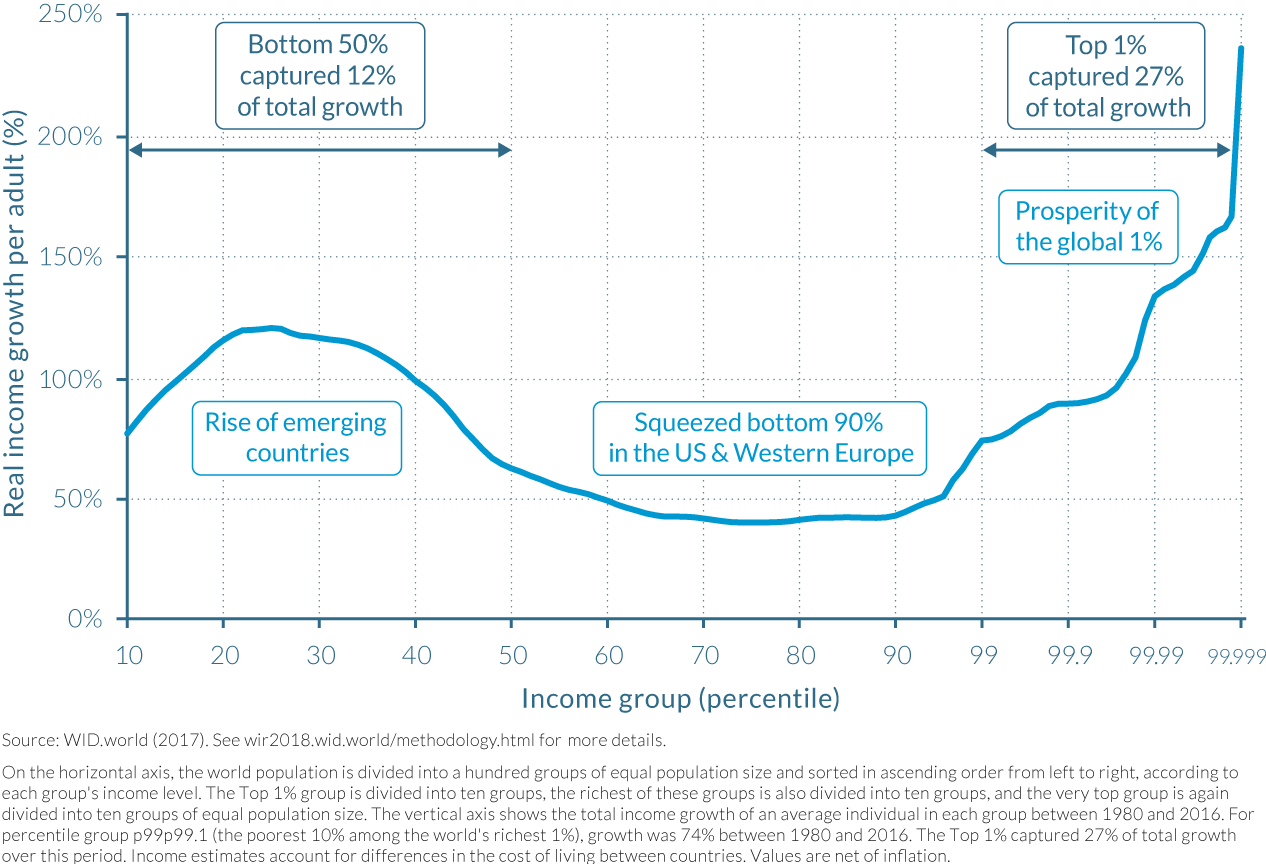

When all countries are taken into account, the shape of the curve is again transformed (Figure 2.1.4). Now, average global income growth rates are further reduced because Africa and Latin America had relatively low growth over the period considered. This contributes to increasing global inequality as compared to the two cases presented above. The findings are the same as those presented in the right-hand column of Table 2.1.2: the top 1% income earners captured 27% of total growth over the 1980–2016 period, as much as the bottom 70% of the population. The top 0.1% captured 13% of total growth, about as much as the bottom 50%.

Figure 2.1.4

Total income growth by percentile across all world regions, 1980–2016

The geography of global income inequality was transformed over the past decades

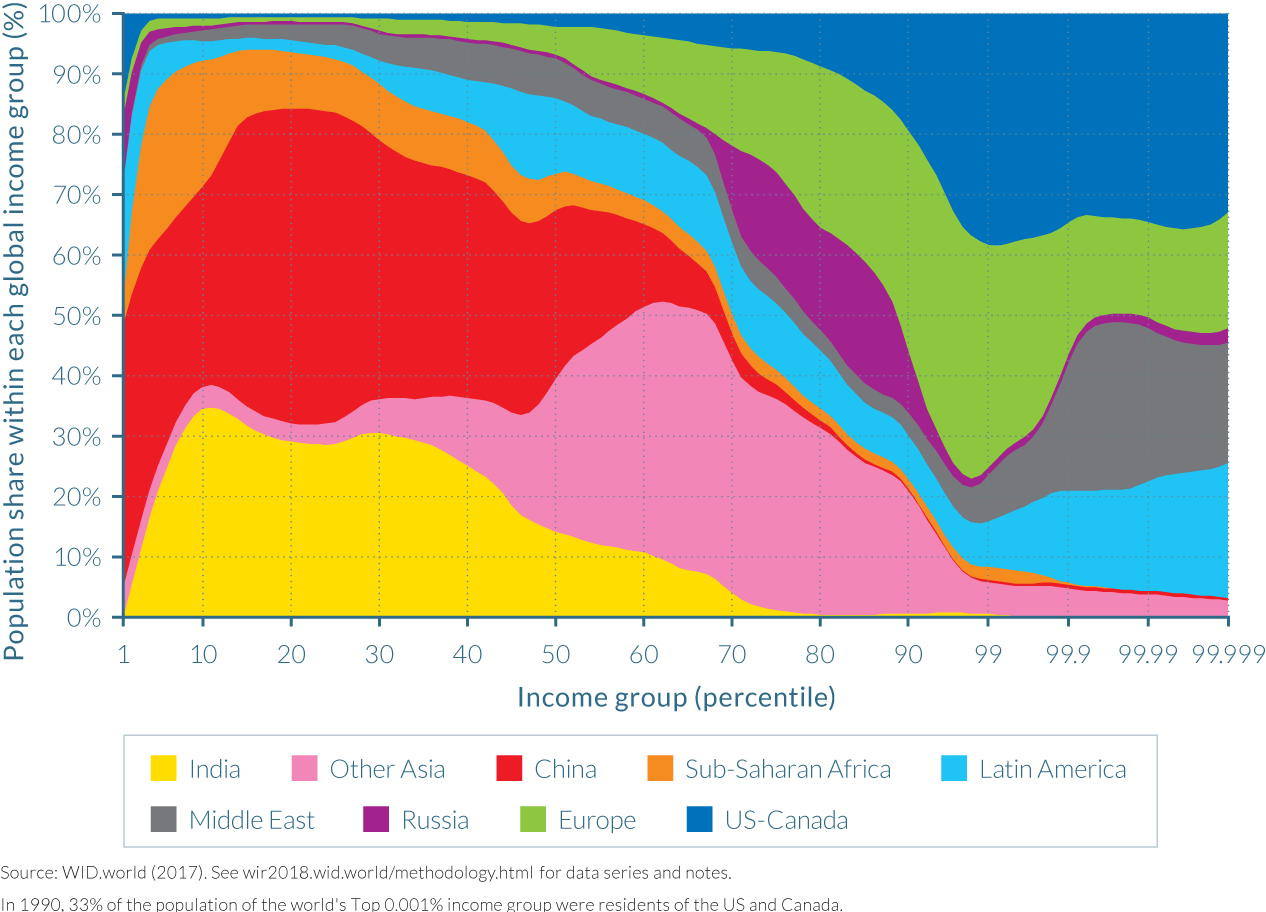

What is the share of African, Asians, Americans, and Europeans in each global income groups and how has this evolved over time? Figures 2.1.5 and 2.1.6 answer these questions by showing the geographical composition of each income group in 1990 and in 2016. Between 1980 and 1990, the geographic repartition of global incomes evolved only slightly, and our data allow for more precise geographic repartition in 1990, so it is preferable to focus on this year. In a similar way to how Figures 2.1.2 through 2.1.4 decomposed the data, Figures 2.1.5 and 2.1.6 decompose the top 1% into 28 groups (see Box 2.1.1). To be clear, all groups above percentile 99 are the decomposition of the richest 1% of the global population.

Figure 2.1.5

Geographic breakdown of global income groups in 1990

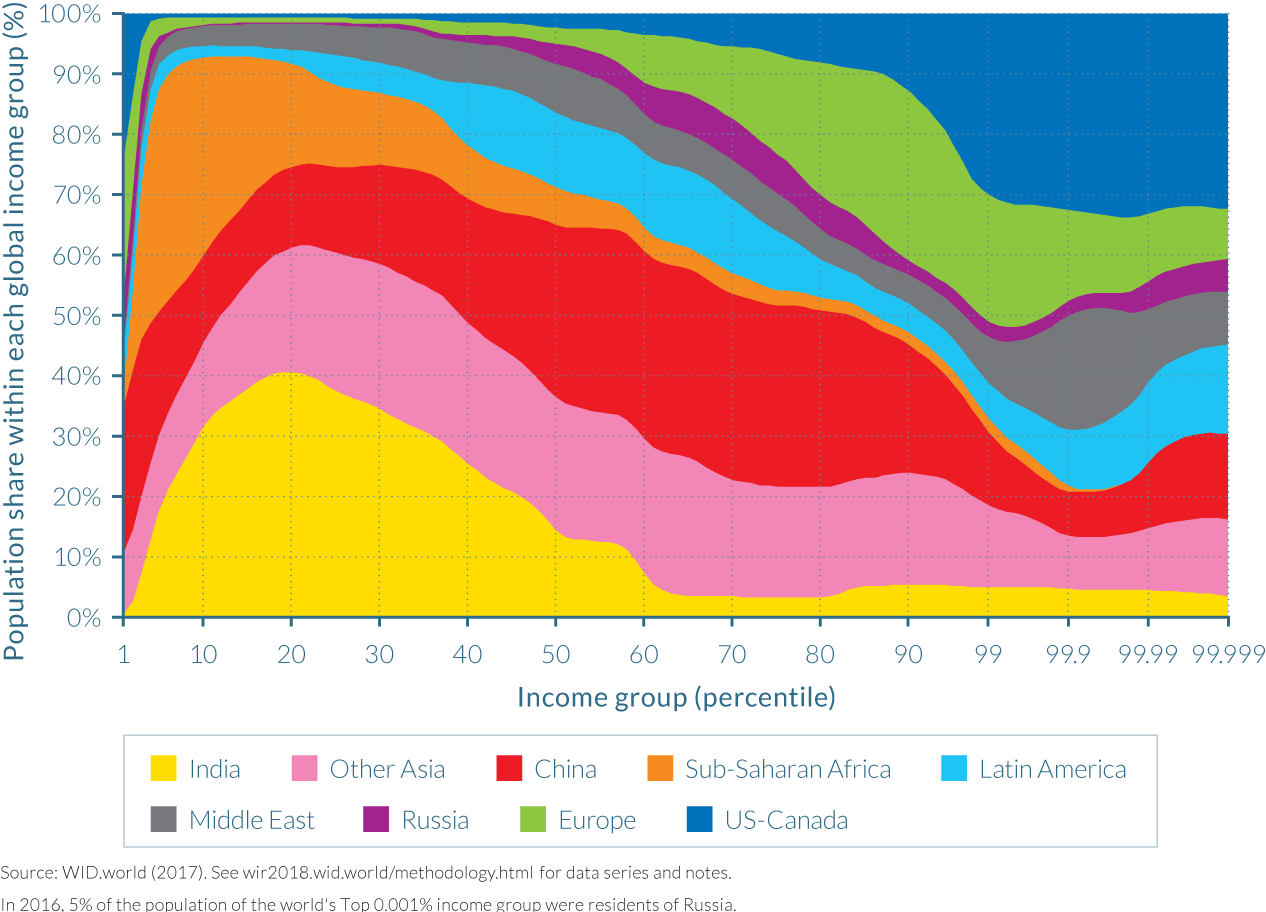

Figure 2.1.6

Geographic breakdown of global income groups in 2016

In 1990, Asians were almost not represented within top global income groups. Indeed, the bulk of the population of India and China are found in the bottom half of the income distribution. At the other end of the global income ladder, US-Canada is the largest contributor to global top-income earners. Europe is largely represented in the upper half of the global distribution, but less so among the very top groups. The Middle East and Latin American elites are disproportionately represented among the very top global groups, as they both make up about 20% each of the population of the top 0.001% earners. It should be noted that this overrepresentation only holds within the top 1% global earners: in the next richest 1% group (percentile group p98p99), their share falls to 9% and 4%, respectively. This indeed reflects the extreme level of inequality of these regions, as discussed in chapters 2.10 and 2.11. Interestingly, Russia is concentrated between percentile 70 and percentile 90, and Russians did not make it into the very top groups. In 1990, the Soviet system compressed income distribution in Russia.

In 2016, the situation is notably different. The most striking evolution is perhaps the spread of Chinese income earners, which are now located throughout the entire global distribution. India remains largely represented at the bottom with only very few Indians among the top global earners.

The position of Russian earners was also stretched throughout from the poorest to the richest income groups. This illustrates the impact of the end of communism on the spread of Russian incomes. Africans, who were present throughout the first half of the distribution, are now even more concentrated in the bottom quarter, due to relatively low growth as compared to Asian countries. At the top of the distribution, while the shares of both North America and Europe decreased (leaving room for their Asian counterparts), the share of Europeans was reduced much more. This is because most large European countries followed a more equitable growth trajectory over the past decades than the United States and other countries, as will be discussed in chapter 2.3.

Since 2000, the picture is more nuanced but within-country inequality is on the rise

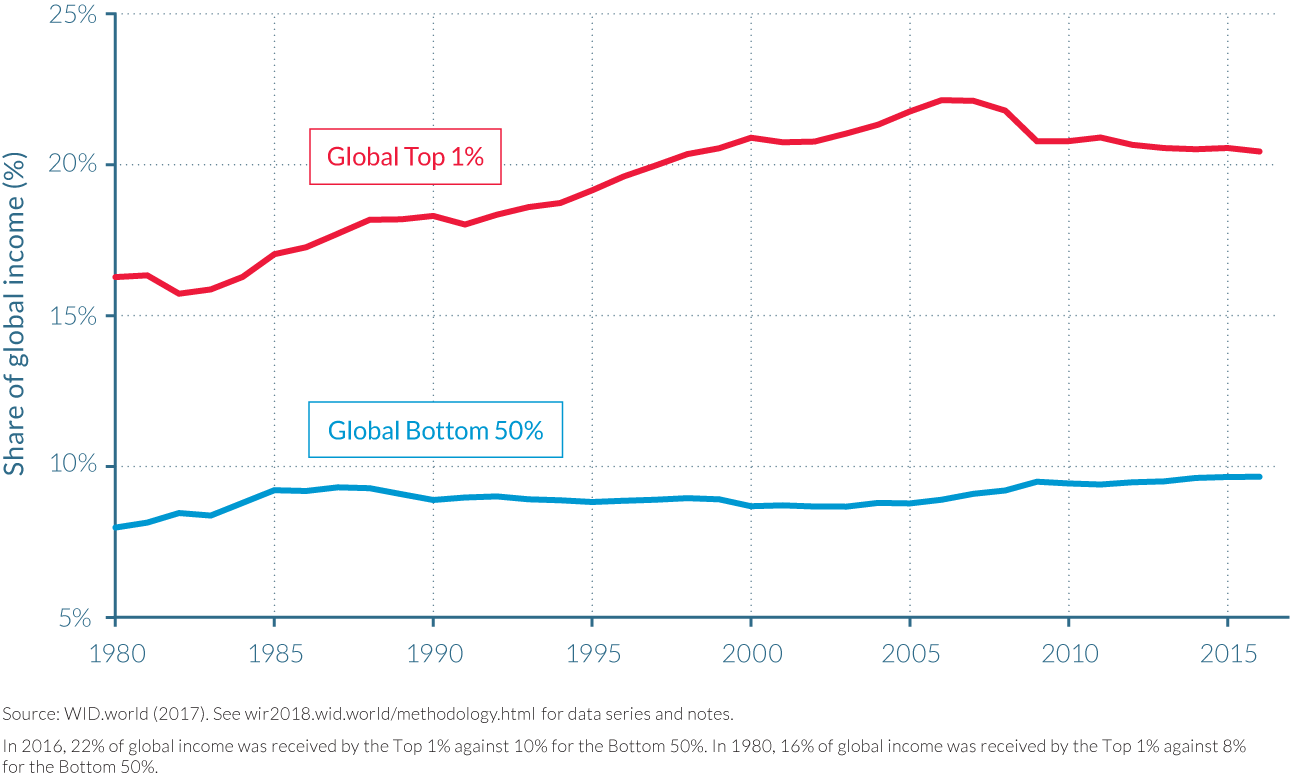

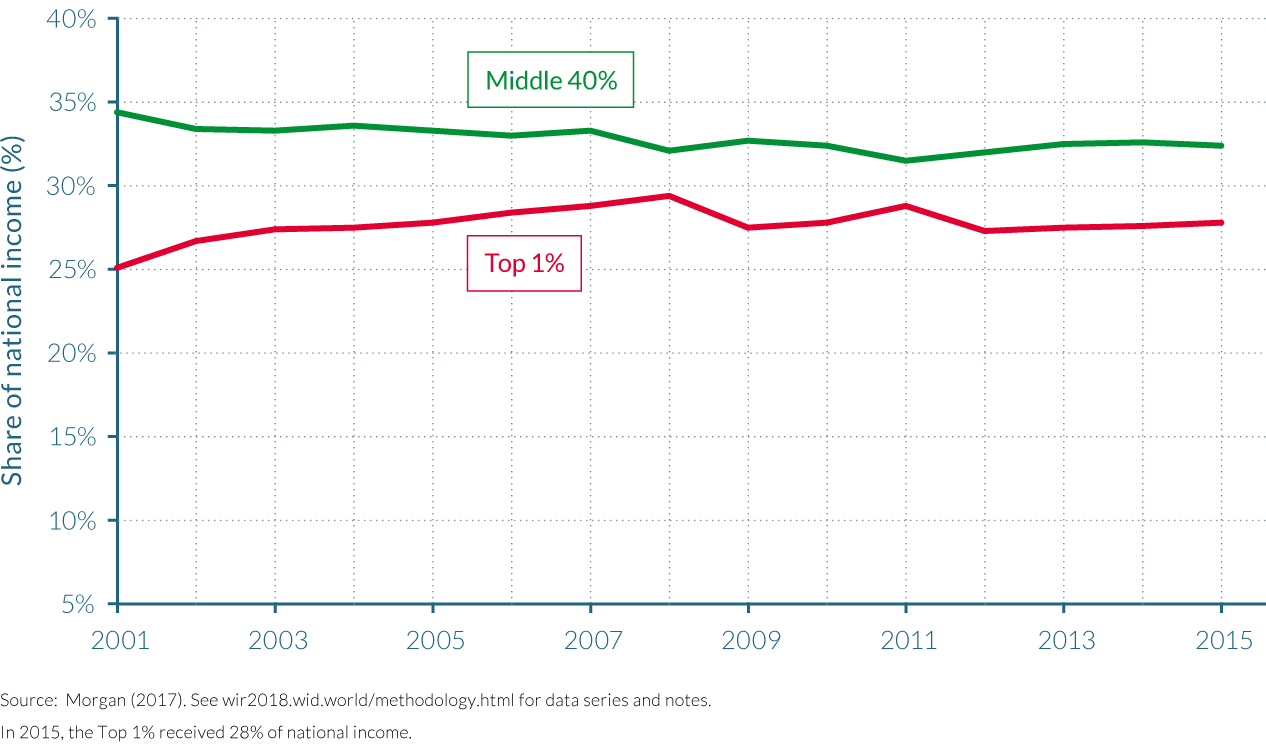

How did global inequality evolve between 1980 and 2016? Figure 2.1.7 answers this question by presenting the share of world income held by the global top 1% and the global bottom 50%, measured at purchasing power parity. The global top 1% income share rose from about 16% of global income in 1980 to more than 22% in 2007 at the eve of the global financial crisis. It was then slightly reduced to 20.4% in 2016, but this slight decrease hardly brought back the level of global inequality to its 1980 level. The income share of bottom half of the world population oscillated around 9% with a very slight increase between 1985 and 2016.

Figure 2.1.7

Global Bottom 50% and Top 1% income shares, 1980–2016

The first insight of this graph is the extreme level of global inequality sustained throughout the entire period with a top 1% income group capturing two times the total income captured by the bottom 50% of the population—implying a factor 100 difference in average per-adult income levels. Second, it is apparent that high growth in emerging countries since 2000, in particular in China, or the global financial crisis of 2008 was not sufficient to stop the rise in global income inequality.

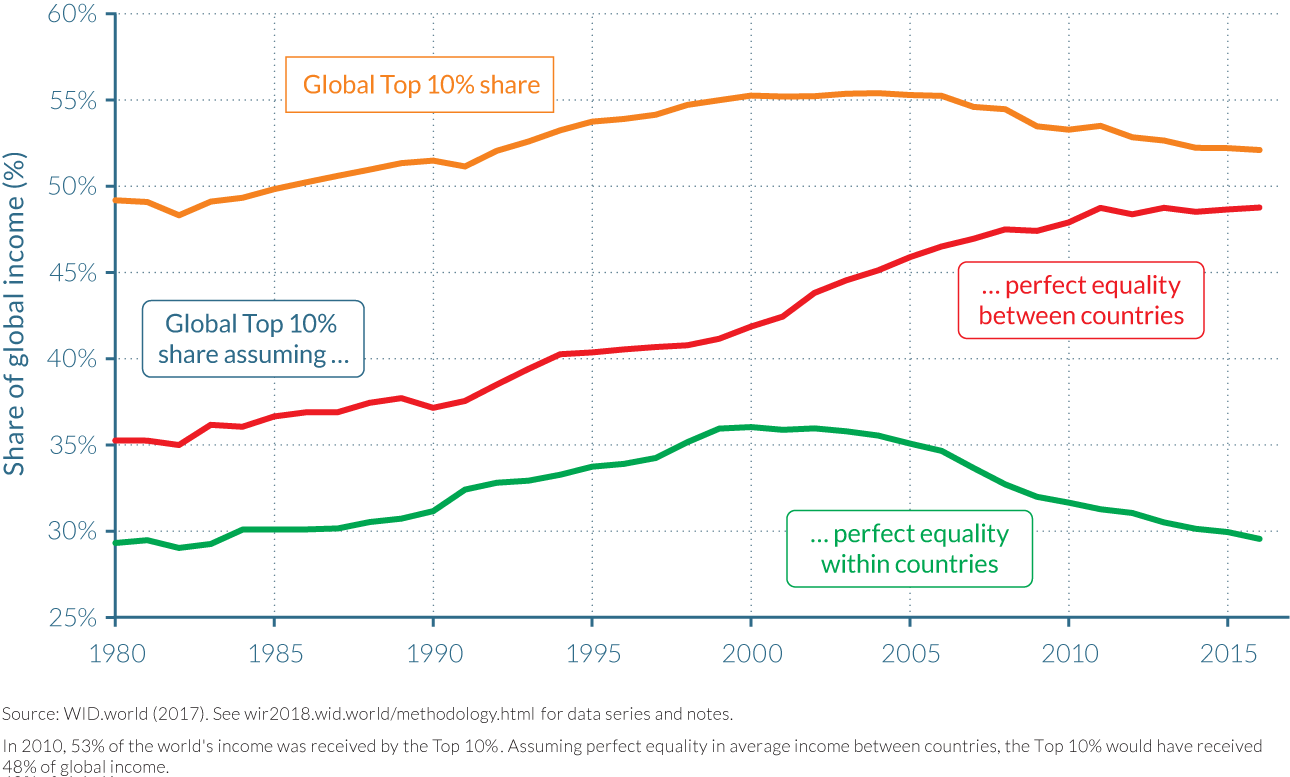

When global inequality is decomposed into a between- and within-country inequality component, it is apparent that within-country inequality continued to rise since 2000 whereas between-country inequality rose up to 2000 and decreased afterwards. Figure 2.1.8 presents the evolution of the global 10% income share, which reached close to 50% of global income in 1980, rose to 55% in 2000–2007, and decreased to slightly more than 52% in 2016. Two alternative scenarios for the evolution of the global top 10% share are presented. The first one assumes that all countries had exactly the same average income (that is, that there was no between-country inequality), but that income was as unequal within these countries as was actually observed. In this case, the top 10% share would have risen from 35% in 1980 to nearly 50% today. In the second scenario, it is assumed that between-country inequality evolved as observed but it is also assumed that everybody within countries had exactly the same income level (no within-country inequality). In this case, the global top 10% income share would have risen from nearly 30% in 1980 to more than 35% in 2000 before decreasing back to 30%.

Figure 2.1.8

Global Top 10% income share, 1980–2016: between versus within country inequality

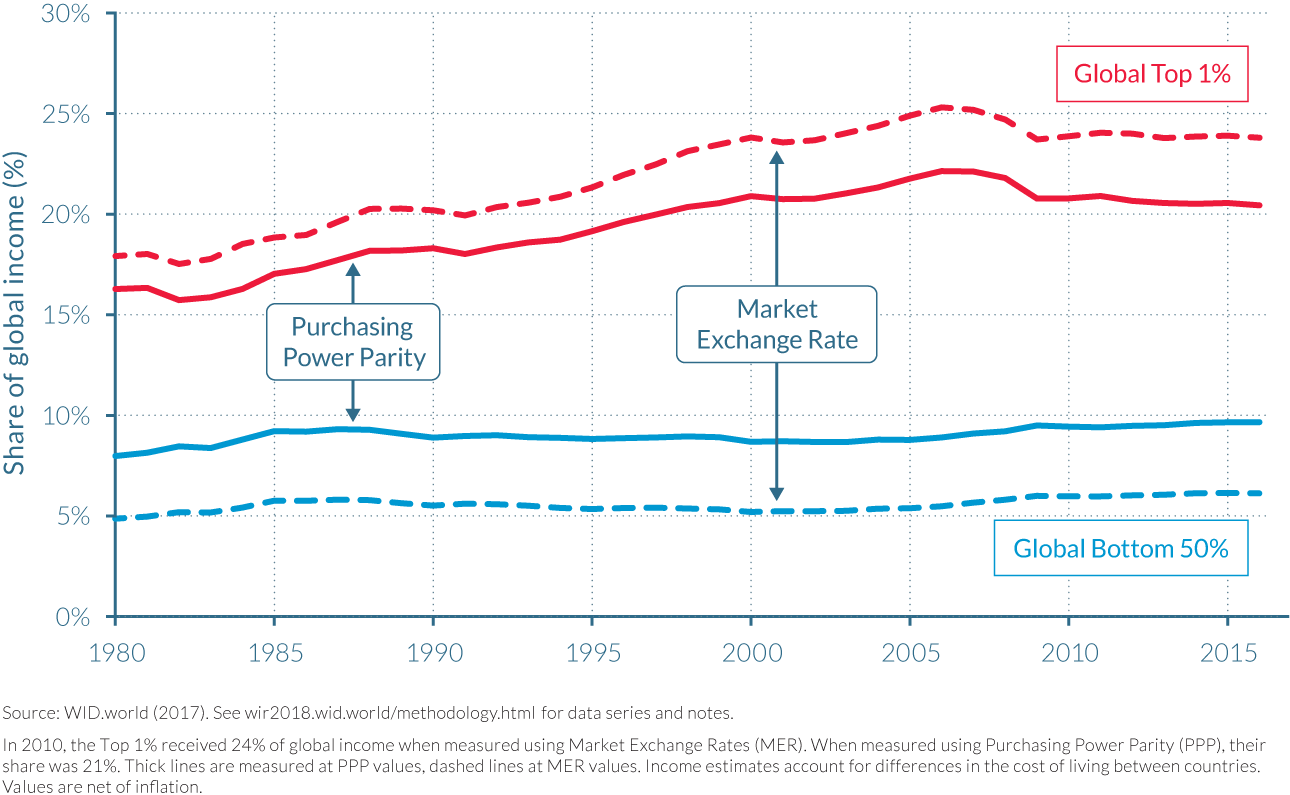

Measured at market exchange rate, global inequality is even higher

Prices can be converted from one currency to another using either market exchange rates or purchasing power parities (as we did above). Market exchanges rates are the prices at which people are willing to buy and sell currencies, so at first glance they should reflect people's relative purchasing power. This makes them a natural conversion factor between currencies. The problem is that market exchange rates reflect only the relative purchasing power of money in terms of tradable goods. But non-tradable goods (typically services) are in fact cheaper relative to tradable ones in emerging economies (given the so-called Balassa-Samuelson effect). Therefore, market exchange rates will underestimate the standard of living in the poorer countries. In addition, market exchange rates can vary for all sorts of other reasons—sometimes purely financial and/or political—in a fairly chaotic manner. Purchasing power parity is an alternative conversion factor that addresses these problems (based on observed prices in the various countries). The level of global income inequality is therefore substantially higher when measured using market exchange rates than it is with purchasing power parity. It increases the global top 1% share in 2016 from 20% to 24% and reduces the bottom 50% share from nearly 10% to 6% (Figure 2.1.9).

Figure 2.1.9

Bottom 50% and Top 1% shares of global income, 1980-2016: PPP versus market exchange rates

Purchasing power parity definitely gives a more accurate picture of global inequality from the point of view of individuals who do not travel across the world and who essentially spend their incomes in their own countries. Market exchange rates are perhaps better to inform about inequality in a world where individuals can easily spend their incomes where they want, which is the case for top global earners and tourists, and increasingly the case for anyone connected to the internet. It is also the case for migrant workers wishing to send remittances back to their home countries. Both purchasing power parity and market exchange rates are valid measures to track global income inequality, depending on the object of study or which countries are compared to one another.

In this report, we generally use purchasing power parity for international comparisons, but at times, market exchange rates are also used to illustrate other meaningful aspects of international inequality.

Carefully looking at countries' diverse growth trajectories and policy changes is necessary to understand drivers of national and global inequality

The past forty years were marked by a steep rise of global inequality, and growth in emerging countries was not high enough to counterbalance it. Whether future growth in emerging countries might invert the trend or not is a key question, which will be addressed in Part V of this report. Before turning to that question, one should understand better the drivers of the trends observed since 1980.

Given that this period was marked by increasing trade integration between countries, it might seem reasonable to seek explanations in economic trade models. The standard economic models of international trade, however, fail to account for dynamics of inequality observed over the past four decades. Take Heckscher-Ohlin, the most well-known of the two-skill-groups economic trade models. According to it, trade liberalization should increase inequality in rich countries, but reduce it in low-income countries.

How does the model reach this conclusion? The underlying mechanism is fairly simple. It is built around the fact that there are more high-skilled workers (such as aeronautical engineers) in the United States than in China, and more low-skilled workers (such as textile workers) in China than in the United States. Before trade liberalization started between these two countries, aeronautical engineers were relatively scarce in China and thus enjoyed relatively high pay compared to textile workers which were abundant. Conversely, in the United States, low-skilled earners were relatively scarce at the time, and the income differential between engineers and textile workers was limited.

When the United States and China started to trade, each country specialized in the domain for which they had the most workers, in relative terms. China thus specialized in textiles, so that textile workers were in higher demand and saw their wages increase, while aeronautical engineers came to be in lower demand and saw their wages decrease. Conversely, the United States specialized in aircraft building, so the aeronautical engineers saw their wages increase, while the textile workers saw their wages decrease. By virtue of the factor price equalization theorem, the wages of low-skilled workers in China and the United States started to converge, along with the wages of high-skilled workers.

While inequality did rise in the United States, as this model predicts, it also sharply rose in China, as well as in India and Russia, as seen in Figure 2.1.1a—contrary to the model's predictions. Regardless of whether the Heckscher-Ohlin is otherwise valid or not, it cannot account for the evolution of global inequality. How can we account for these empirical findings? As Table 2.1.1 suggests, countries followed very different growth and inequality trajectories over the past decades. It seems necessary to carefully look at these trajectories as well as the institutional and policy shifts which may have occurred in various regions of the world over the past forty years.

Understanding the drivers of global income inequality requires a thorough analysis of the distribution of national income growth within countries. These dynamics are explored in the following chapters.

2.2 Trends in income inequality between countries

Information in this chapter is based on "National Accounts Series Methodology," by Thomas Blanchet and Lucas Chancel, 2016. WID.world Working Paper Series (No. 2016/1), and on subsequent WID.world updates.

- When focusing on income inequalities between countries, it is more meaningful to compare national incomes than gross domestic product (GDP). National income takes into account depreciation of obsolete machines and other capital assets as well as flows of foreign income.

- At the global level, average per-adult national income is €1 340 per month. North Americans enjoy an income three times higher, while Europeans have an income two times higher. Average per-adult income in China is slightly lower than the global average. As a country, however, China represents a higher share of global income than North America or Europe (19%, 17%, and 17%, respectively).

- This situation sharply contrasts with that of 1980, when China represented only 3% of total global income. Over this period, strong converging forces were in play which reduced global income inequality between countries. While growth slowed in Western Europe, it skyrocketed in Asia and China in particular, following the modernization of its economy and its opening to global markets.

- However, diverging forces were also in play in other parts of the world. From 1980 to now, average incomes in sub-Saharan Africa and South America fell behind the world average.

National income is more meaningful than GDP to compare income inequalities between countries

Public debates generally focus on the growth of gross domestic product (GDP) to compare countries' economic performance. However, this measure is of only limited use in measuring national welfare. GDP measures the value of all goods and services sold in an economy, after having subtracted the costs of materials or services incurred in production processes. As such, it does not properly account for capital depreciation, or for public "bads" such as environmental degradation, rising crime, or illnesses (because these lead to expenditures that contribute to GDP). These limitations have led many statistical agencies, and a growing number of governments, to develop and use complementary indicators of economic performance and well-being.3

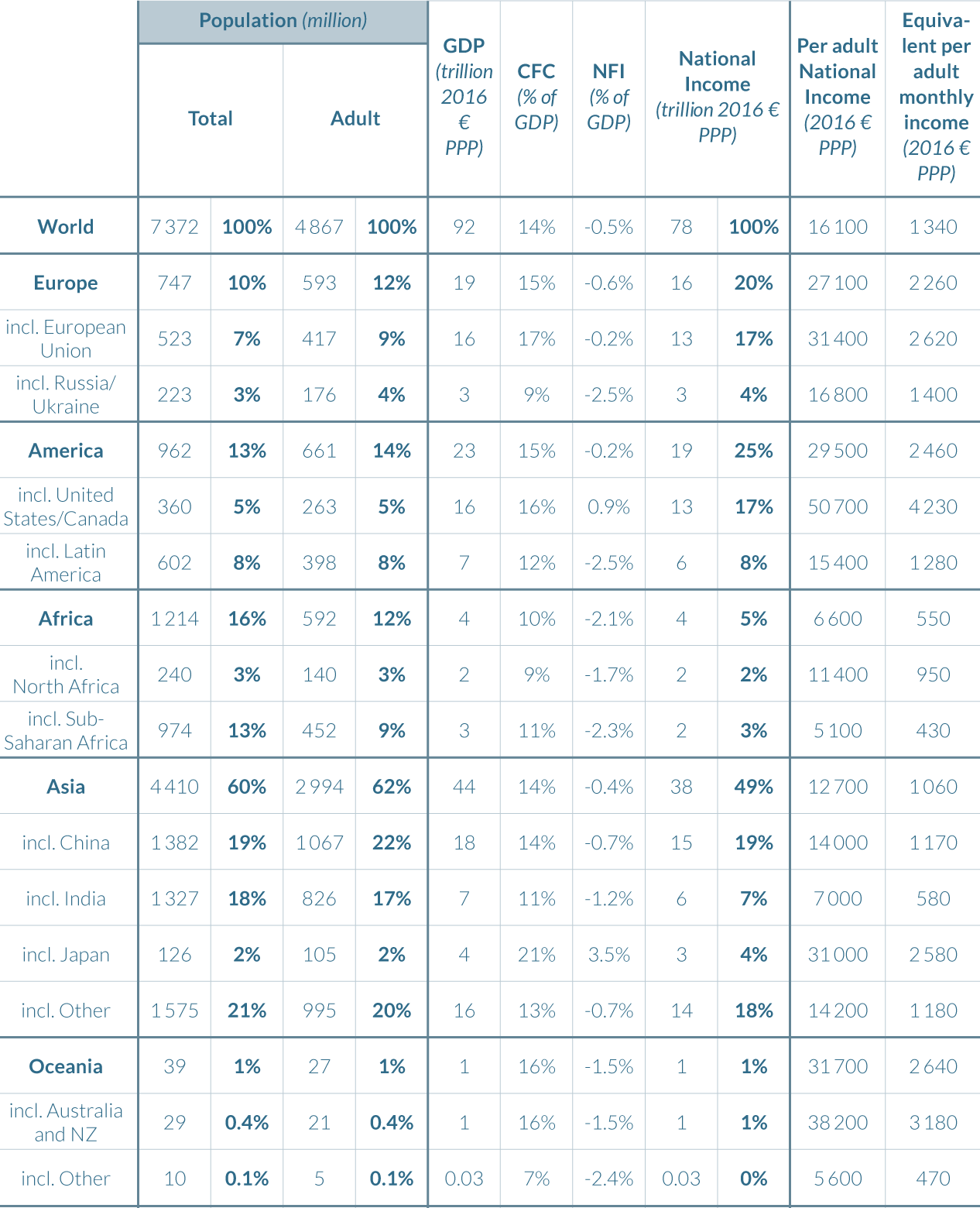

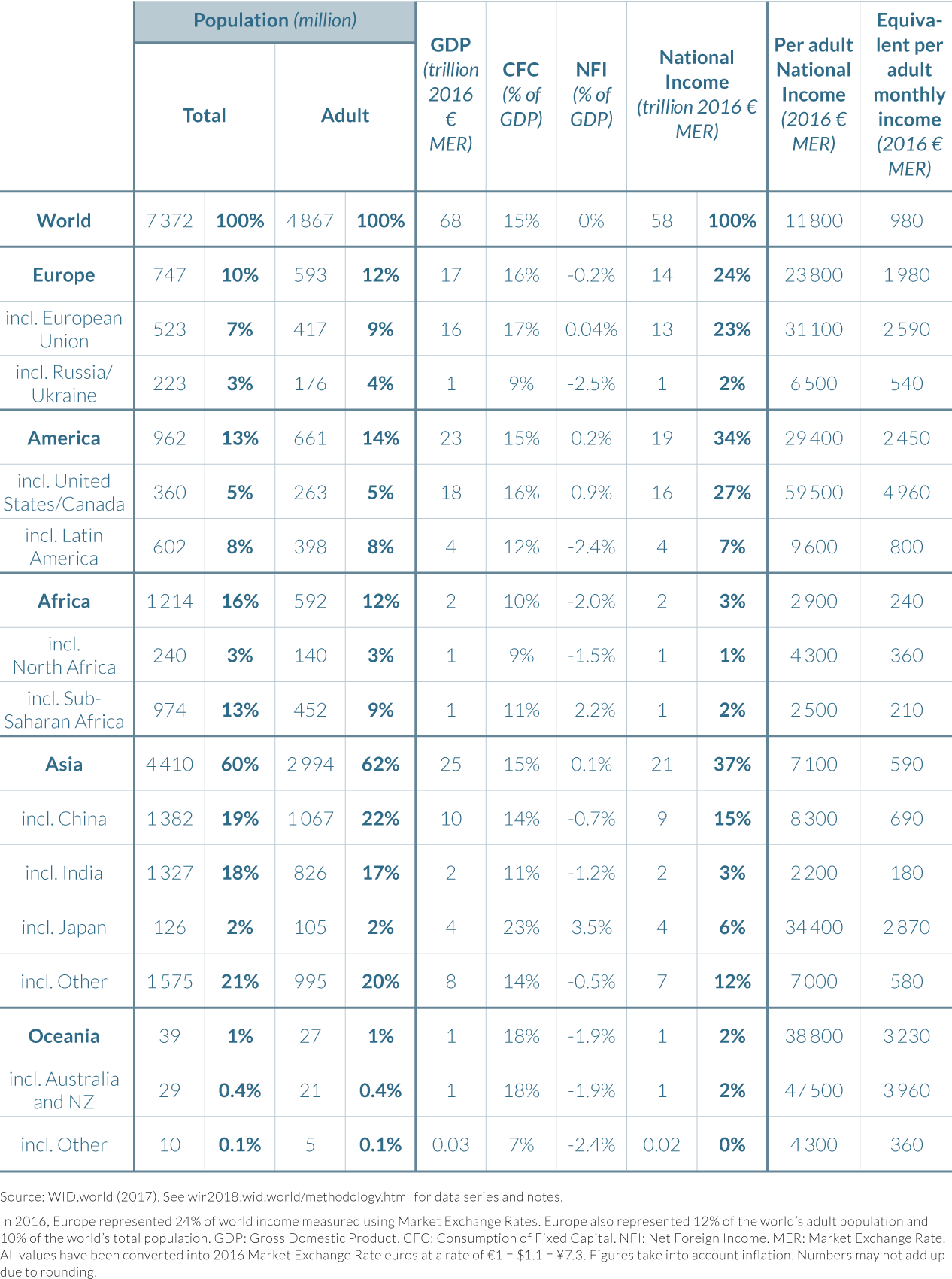

Beyond the fact that the GDP framework is not meant for the analysis of inequality within countries, it has two other important limitations when the focus is on income inequality between countries. The first one is that gross domestic product, as its name indicates, is a gross measure: it does not take into account expenses required to replace capital that has been deteriorated or that has become obsolete during the course of production of goods and services in an economy. Machines, computers, roads, and electric systems have to be repaired or replaced every year. This has been termed capital depreciation or consumption of fixed capital (CFC). Subtracting it from GDP yields the net domestic product, which is a more accurate measure of true economic output than GDP. Consumption of fixed capital actually varies over time and countries (Table 2.2.1). Countries that have an important stock of machines in their overall stock of capital tend to replace higher shares of overall capital. This is generally true for advanced and automatized economies—in particular, for Japan, where consumption of fixed capital is equal to 21% of its GDP (which reduces GDP by close to €8 000 per year and per adult). Consumption of fixed capital is also high in the European Union and the United States (16–17%). On the contrary, economies that possess relatively fewer machines and a higher share of agricultural land in their capital stock tend to have lower CFC values. CFC is equal to 11% of GDP in India, and 12% in Latin America. CFC variations thus modify the levels of global inequality between countries. Such variations tend to reduce global inequality, since the income dedicated to replacing obsolete machines tends to be higher in rich countries than in low-income countries. In the future, we plan to better account for the depreciation of natural capital in these estimates.

GDP figures have another important limitation when the need is to compare income inequality between countries and over time. At the global level, net domestic product is equal to net domestic income: by definition, the market value of global production is equal to global income. At the national level, however, incomes generated by the sale of goods and services in a given country do not necessarily remain in that country. This is the case when factories are owned by foreign individuals, for instance. Taking foreign incomes into account tends to increase global inequality between countries rather than reduce it. Rich countries generally own more assets in other parts of the world than poor countries do. Table 2.2.1 shows that net foreign income in North America amounts to 0.9% of its GDP (which corresponds to an extra €610 ($670) received by the average North American adult from the rest of the world.4 Meanwhile, Japan's net foreign income is equal to 3.5% of its GDP (corresponding to €1 460 per year and per adult). Net foreign income within the European Union is slightly negative when measured at PPP values (Table 2.2.1) and very slightly positive when measured at market exchange rate values (Table 2.2.2). This figure in fact hides strong disparities within the European Union. France and Germany have strongly positive net foreign income (2 to 3% of their GDP), while Ireland and the United Kingdom have negative net foreign incomes (this is largely due to the financial services and foreign companies established there). On the other hand, Latin America annually pays 2.4% of its GDP to the rest of the world. Interestingly, China has a negative net foreign income. It pays close to 0.7% of its GDP to foreign countries, reflecting the fact that the return it receives on its foreign portfolio is lower than the return received by foreign investments in China.

By definition, at the global level, net foreign income should equal zero: what is paid by some countries must be received by others. However, up to now, international statistical institutions have been unable to report flows of net foreign incomes consistently. At the global level, the sum of reported net foreign incomes has not been zero. This has been termed the "missing income" problem: a share of total income vanishes from global economic statistics, implying non-zero net foreign income at the global level.

The World Inequality Report 2018 relies on a novel methodology which takes income flows from tax havens into account. Our methodology relies on estimations of offshore wealth measured by Gabriel Zucman.5 It should be noted that, when measured at market exchange rates, net foreign income flows should sum to zero (Table 2.2.2), but there is no reason for this to happen when incomes are measured at purchasing power parity (Table 2.2.1). Taking into account missing net foreign incomes does not radically change global inequality figures but can make a large difference for particular countries. This constitutes a more realistic representation of income inequality between countries than figures generally discussed.

Table 2.2.1

The distribution of world national income and gross domestic product, 2016:

Purchasing Power Parity

Asian growth contributed to reduce inequality between countries over the past decades

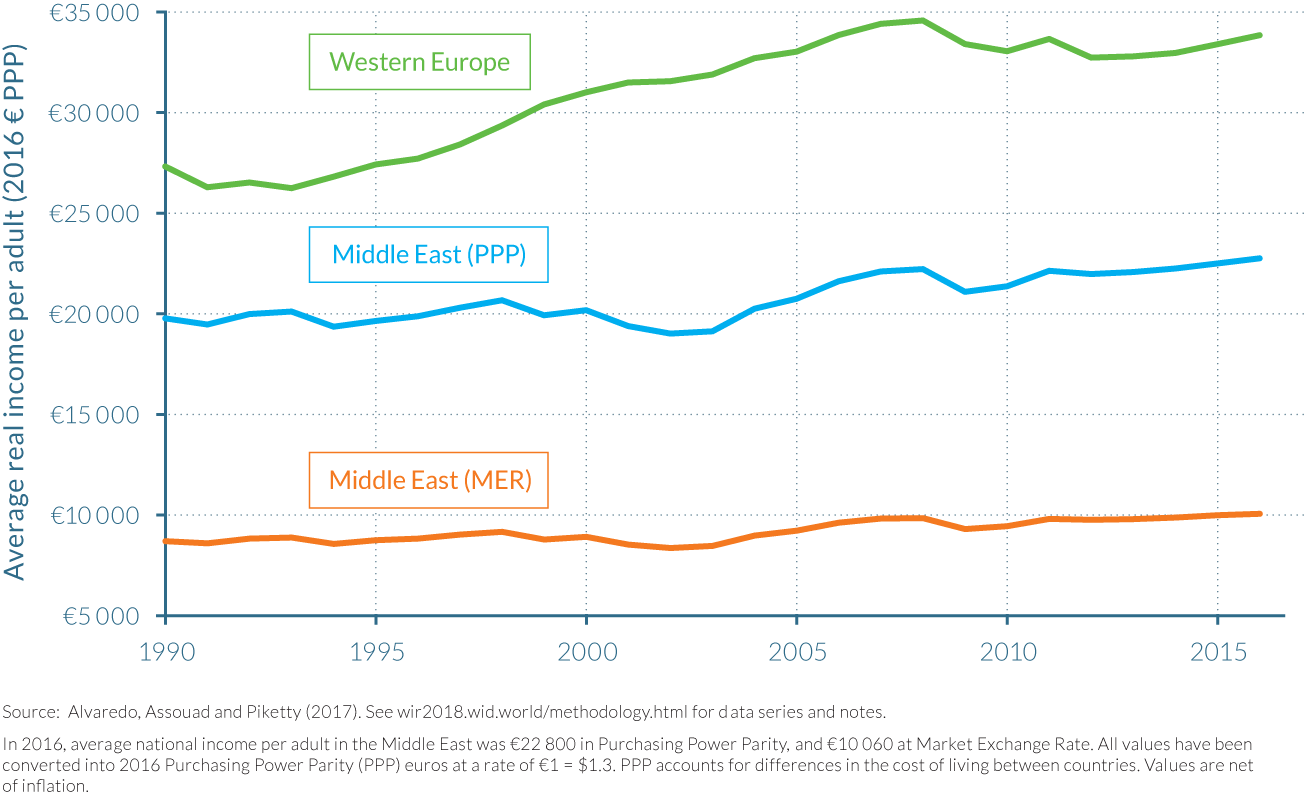

At the global level, per-adult monthly income in 2016 is €1 340 ($1 740) at purchasing power parity (PPP) and €990 ($1 090) at market exchange rate (MER). As discussed, PPP and MER are different ways to measure incomes and inequality across countries. Whereas MER reflects market prices, PPP aims to take price differences between countries into account.

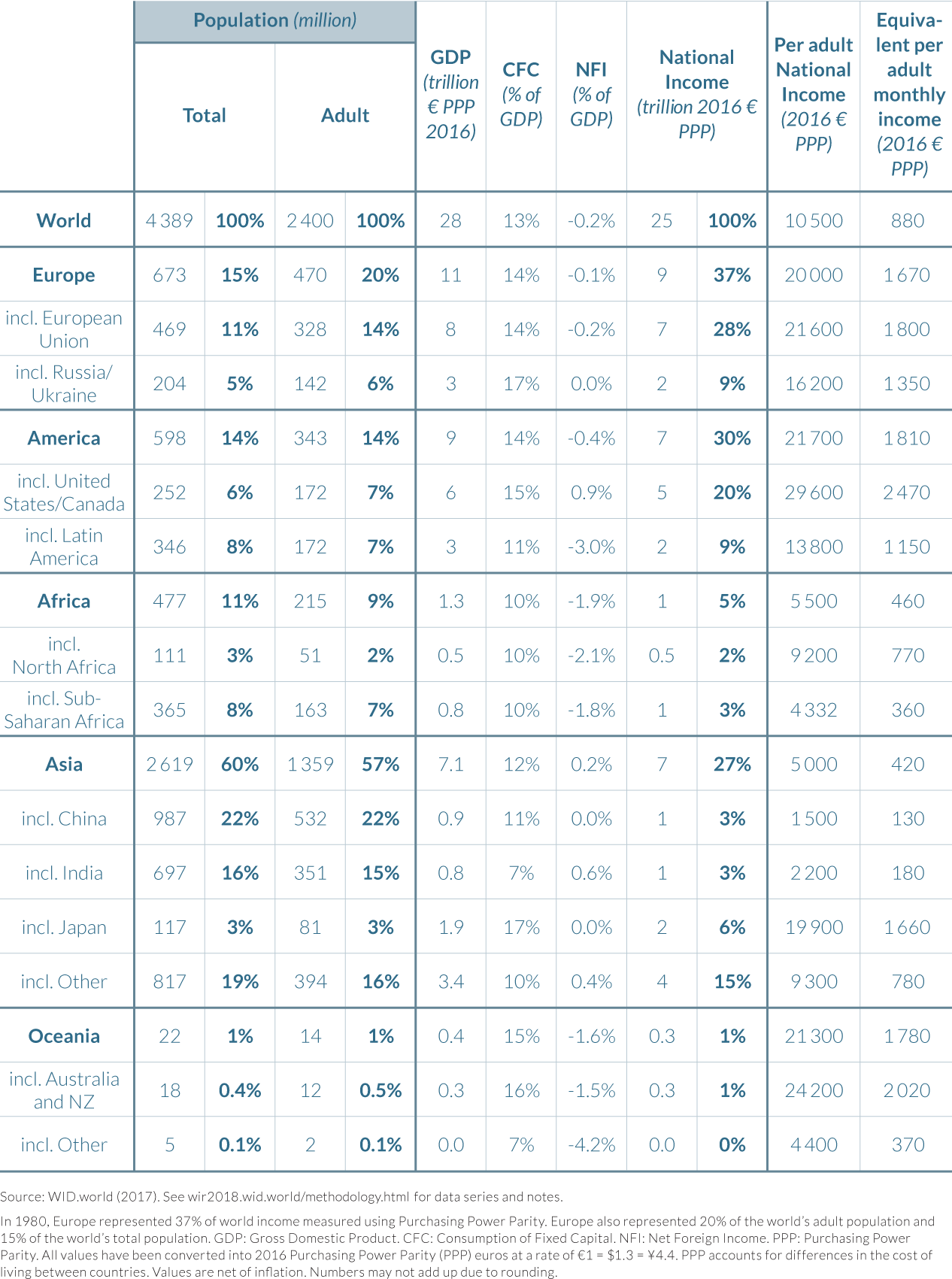

National income is about three times higher in North America at PPP (€4 220 or $5 490 per adult per month) than the global average and it is two times higher in the European Union at PPP than the global average (€2 630 or $3 420 per adult per month). Using MER values, gaps between rich countries and the global average are reinforced: United States and Canada are five times richer than the world average whereas the EU is close to three times richer.6 In China, per-adult income is €1 170 or $1 520 at PPP—that is, slightly lower than world average (€1 340 or $1 740). China as a whole represents 19% of today's global income. This figure is higher than North America (17%) and the European Union (17%). Measured at MER, the Chinese average is, however, equal to €700 or $770, notably lower than the world average (€990 or $1 090). The Chinese share of global income is reduced to 15% versus 27% for US-Canada and 23% for the EU.

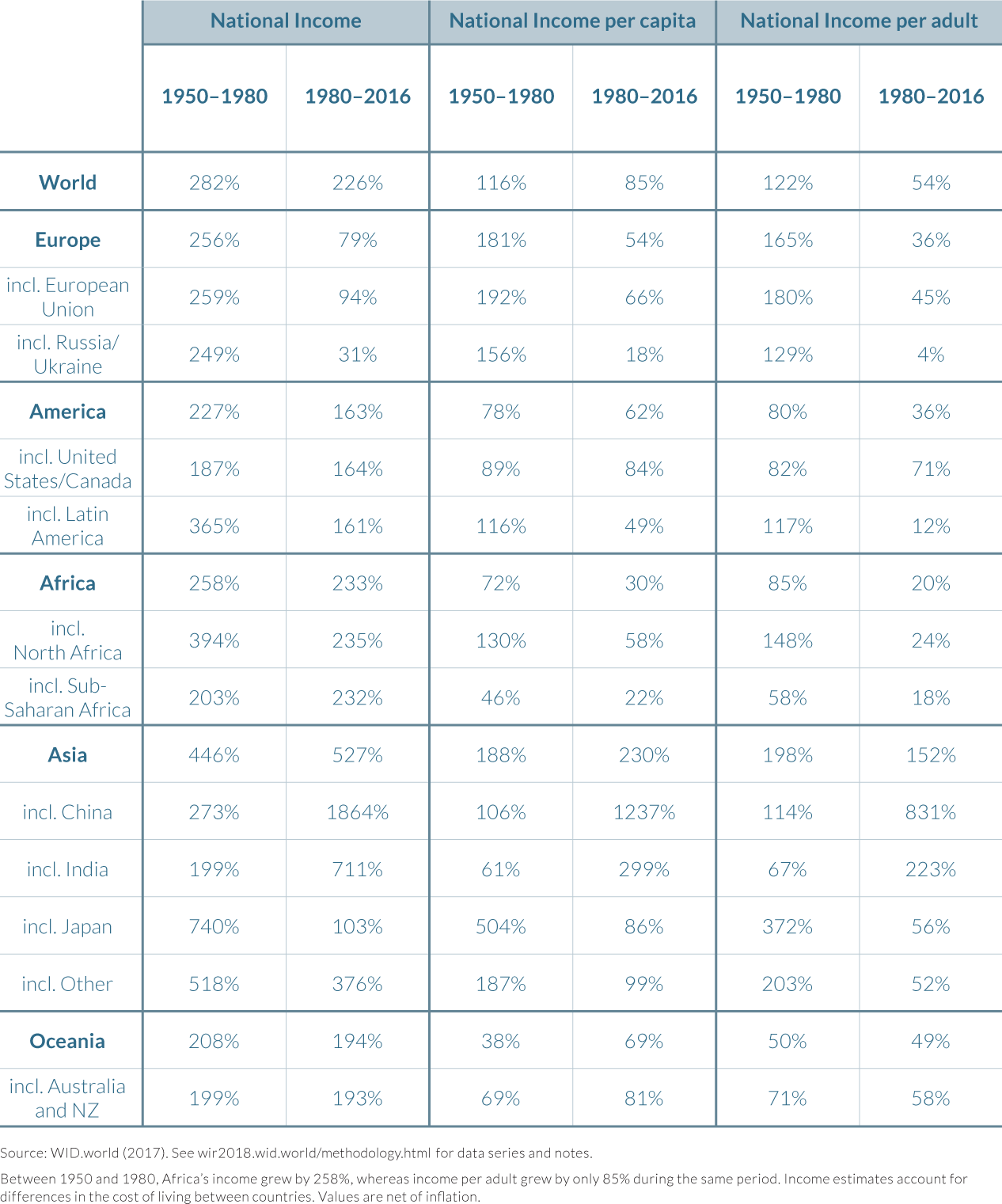

This marks a sharp contrast with the situation in 1980. Thirty-eight years ago, China represented only 3% of global income versus 20% for US-Canada and 28% for the European Union (at purchasing power parity estimates: see Table 2.2.3). Indeed, China's impressive real per-adult national income growth rate over the period (831% from 1980 to 2016, versus 106% from 1950 to 1980: see Table 2.2.4) highly contributed to reducing between-country inequalities over the world. Another converging force lies in the reduction of income growth rates in Western Europe, as compared to the previous decades (180% per-adult growth between 1950 and 1980 versus 45% afterwards). This deceleration in growth rates was due to the end of the "golden age" of growth in Western Europe but also due to the Great Recession, which led to a decade of lost growth in Europe. Indeed, per-adult income in Western Europe was in 2016 the same as ten years before, before the onset of the financial crisis.

Despite a reduction of inequality between countries, average national income inequalities remain strong among countries. Developing and emerging countries did not all grow at the same rate as China. India's average monthly per-adult income (€580 or $750) is still only 0.4 times the world average measured at PPP, while sub-Saharan Africa is only 0.3 times the world average (€430 or $560) today. Average North Americans earn close to ten times more than average sub-Saharan Africans.

Table 2.2.2

The distribution of world national income and gross domestic product, 2016:

Market Exchange Rates

Table 2.2.3

The distribution of world national income and gross domestic product, 1980:

Purchasing Power Parity

Table 2.2.4

Total national income growth rates by world region, 1950–2016

Diverging forces were also at play in certain parts of the world, such as sub-Saharan Africa and Latin America.

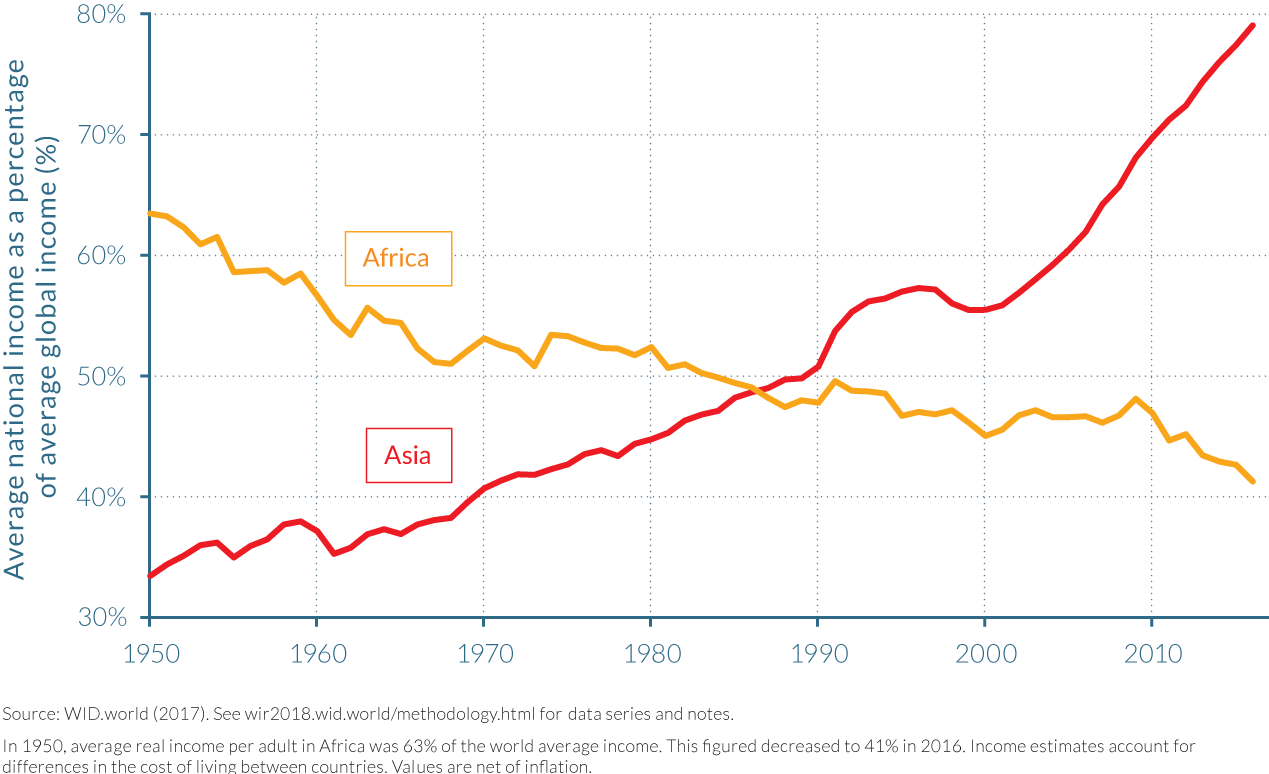

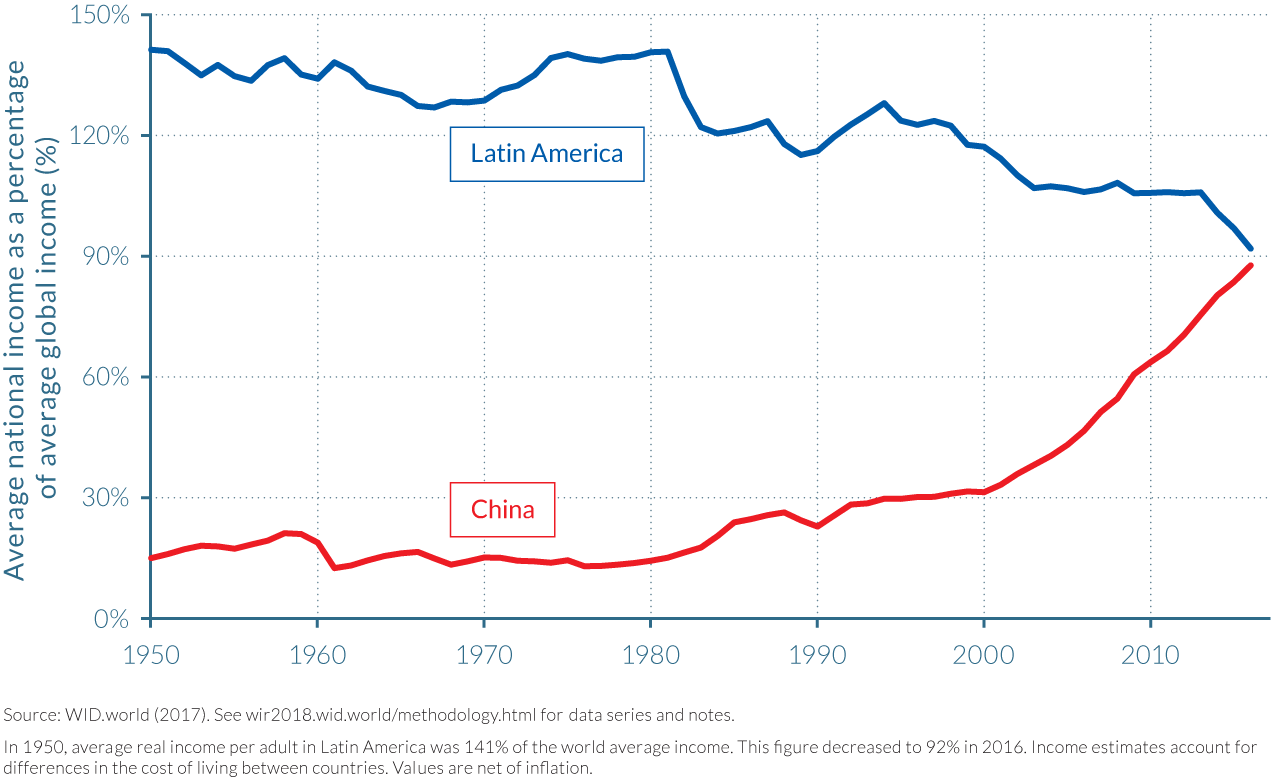

Huge inequalities persist among countries but, in some cases, they actually worsened. Certain low- to middle-income regions are relatively worse off today than four decades ago. Between 1980 and 2016, per-adult incomes in Africa grew more slowly (18%) than the world's average per-adult incomes (54%). This growth trend, marked by a combination of political and economic crises and wars, is not limited to the poorest region of the world. In South America, as well, incomes have grown by only 12% since 1980. As a result, these regions' average incomes fell relative to the world average, from 65% to only 40% of the world average in 1950, versus 140% to less than 100% in Latin America (Figures 2.2.1 and 2.2.2).

Figure 2.2.1

Average income in Africa and Asia relative to the global average, 1950–2016

Figure 2.2.2

Average income in China and Latin America relative to the global average, 1950–2016

2.3 Trends in income inequality within countries

- After a historical decline in most parts of the world from the 1920s to the 1970s, income inequality is on the rise in nearly all countries. The past four decades, however, display a variety of national pathways, highlighting the importance of political and institutional factors in shaping income dynamics.

- In the industrialized world, Anglo-Saxon countries have experienced a sharp rise in inequality since the 1980s. In the United States, the bottom 50% income share collapsed while the top share boomed. Continental European countries were more successful at containing rising inequality, thanks to a policy and institutional context more favorable to lower- and middle-income groups.

- In China, India, and Russia, three formerly communist or highly regulated economies, inequality surged with opening and liberalization policies. The steepest rise occurred in Russia, where the transition to a market economy was particularly abrupt.

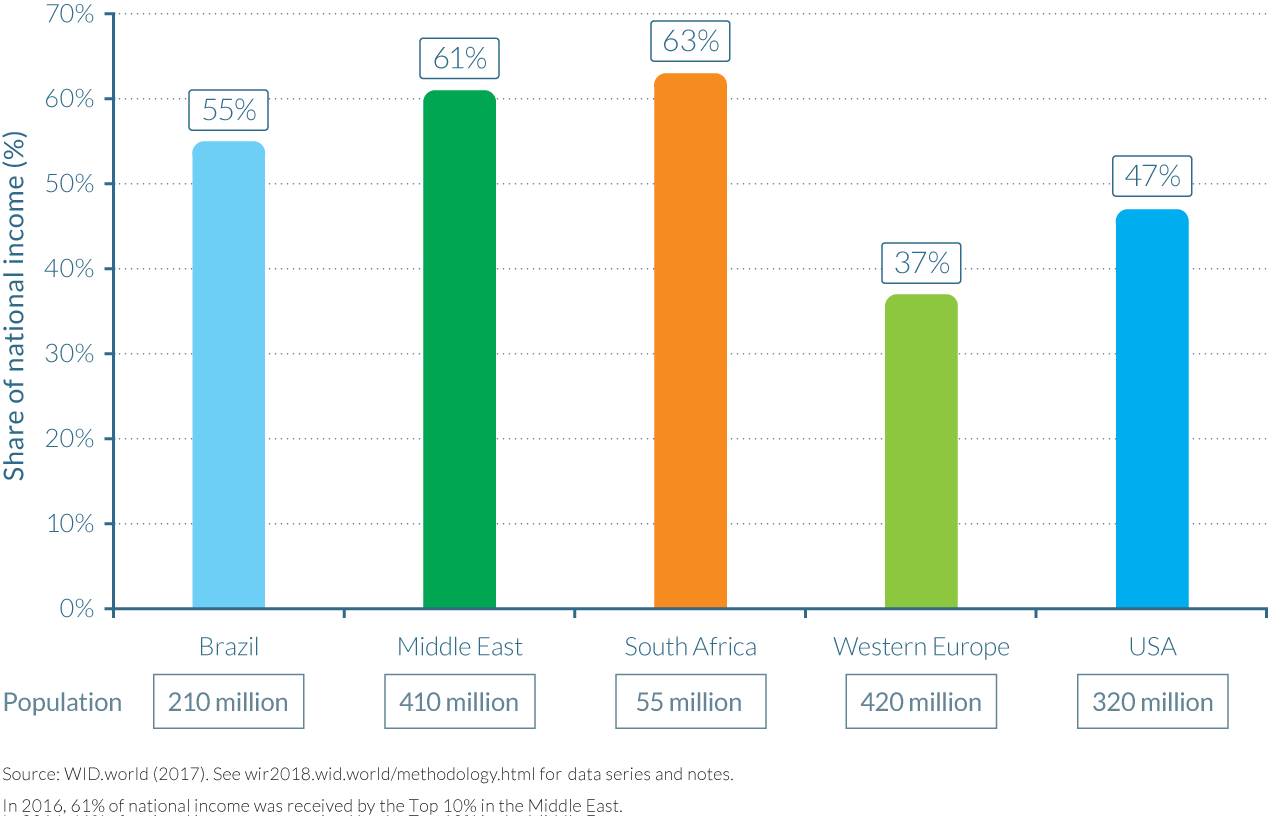

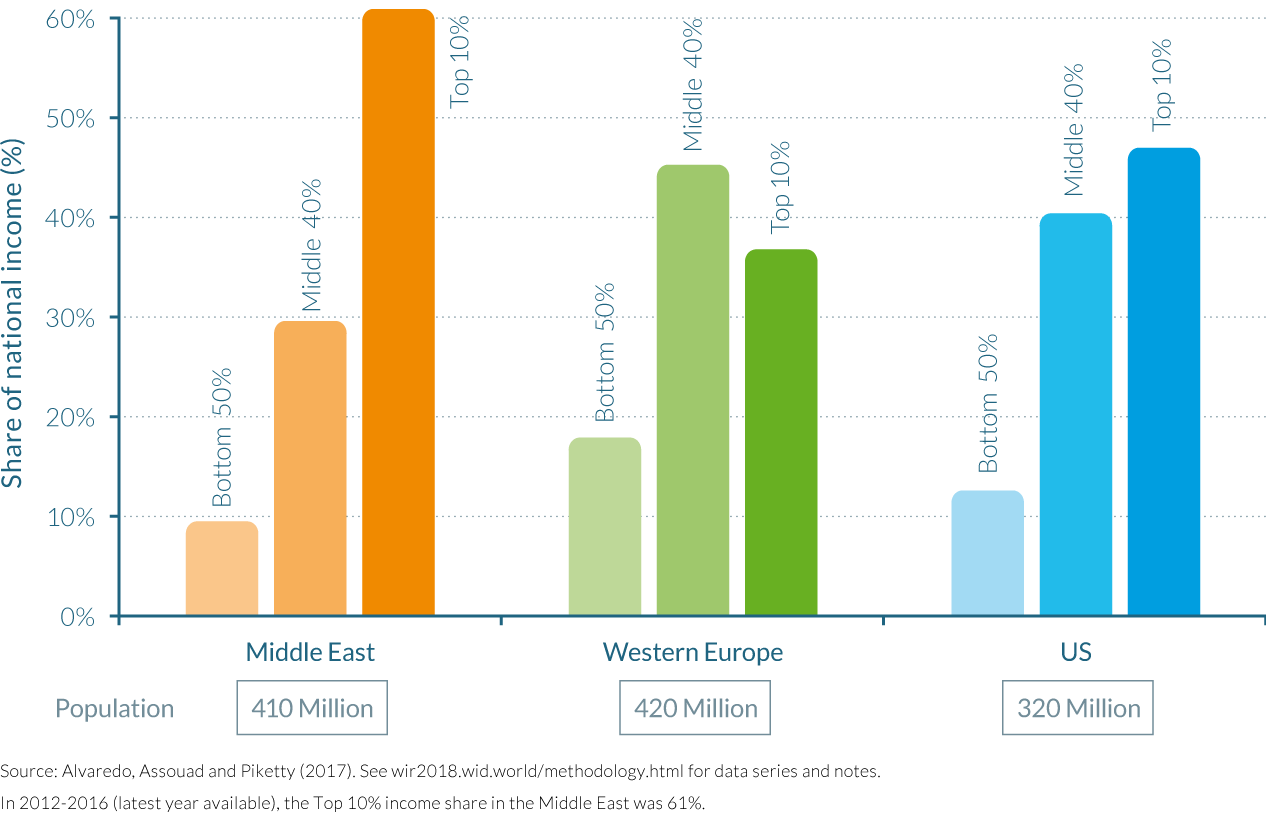

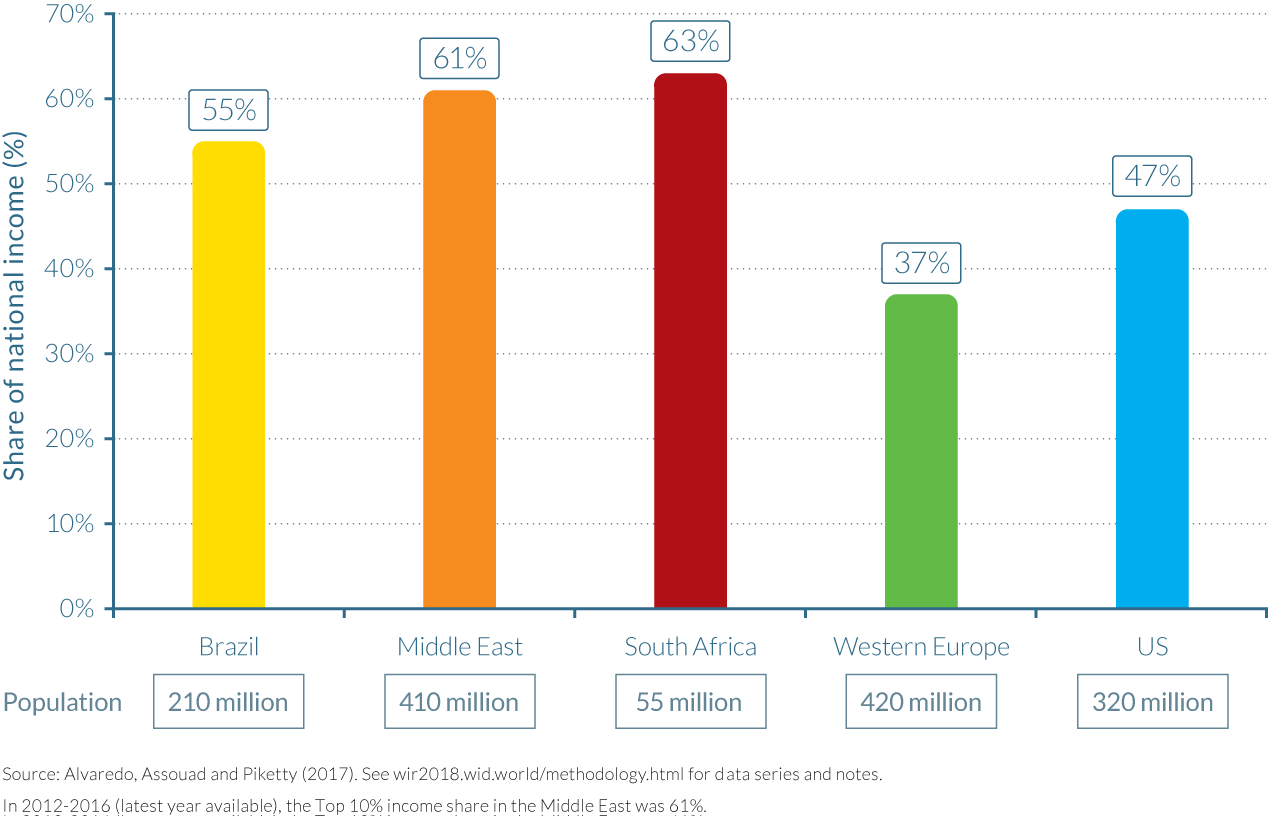

- Inequality is extreme in Brazil, the Middle East, and South Africa, the world's most unequal regions. In these three large emerging markets, inequality currently reaches extreme levels: the top 10% earners capture 55% to 65% of national income.

- Little is known of the long-run dynamics of income inequality in many low-income countries. More information is essential for peaceful democratic debates in these countries, especially given that official estimates are very likely to understate existing levels of inequality.

After a historical decline from the 1920s to the 1970s, income inequality is on the rise in most regions of the world

Income inequality was sharply reduced in the first half of the twentieth century—more precisely, between the 1920s and the 1970s—in most countries of the world, but it has been on the rise almost everywhere since the late 1970s. In Europe and North America, the long-run decline in income inequality was due to the combination of political, social, and economic shocks already discussed. These included the destruction of human and physical capital led by the World Wars, the Great Depression, nationalization policies, and government control over the economy. After the Second World War, a new policy regime was put in place, including the development of social security systems, public education, social and labor policies, and progressive taxation. This combination of factors severely affected very high fortunes, and enabled the rise of a patrimonial middle class and a general decline in inequality in Europe—and to a lesser extent, in North America.7

In emerging economies, political and social shocks led to an even more radical reduction of income inequality. The abolition of private property in Russia, land redistribution, massive investments in public education, and strict government control over the economy via five-year plans effectively spread the benefits of growth from the early 1920s to the 1970s. In India, which did not undergo a communist revolution but implemented socialist policies after gaining its independence, income inequality was also severely reduced over the same period. For most of the global population, the first three-quarters of the twentieth century corresponded to a very strong compression in the distribution of national incomes. The economic elite captured a much smaller share of economic growth in the late 1970s than it did at the beginning of the century.

The trend was then reversed in most countries—even though there are notable exceptions deserving attention. Countries did not all follow the same path. Large emerging countries, as they underwent profound deregulations of their economies, saw inequalities surge as they opened up and liberalized but followed different transition strategies. In rich countries, inequality levels also varied largely according to changes in institutional and policy contexts, with sharp income inequality rises in the Anglo-Saxon world and more moderate increases in continental Europe and Japan. Certain Western European and Northern European countries almost contained the rise in income inequality.

Given the multitude of trends presented in this chapter, it would be imprudent to seek a single story line behind the rise of inequality across countries. Our findings show that national cultural, political, and policy contexts are key to understanding the dynamics of income inequality. In this chapter, we largely focus on the evolution of top-income shares, as they are now available for a very large set of countries. In the country-by-country chapters that come next, the focus will be more detailed and we will shift the attention to bottom-income groups.

Bottom-income groups were shut off from economic growth in the United States, while top incomes surged in the Anglo-Saxon world

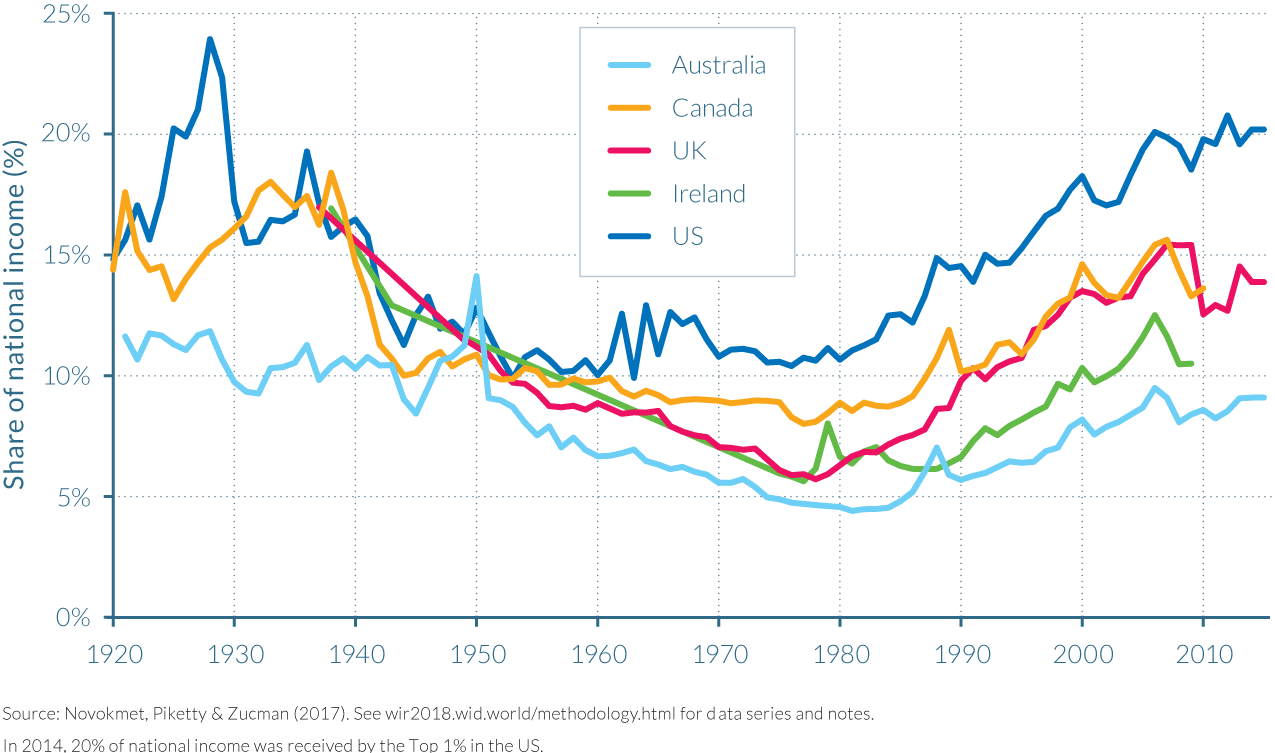

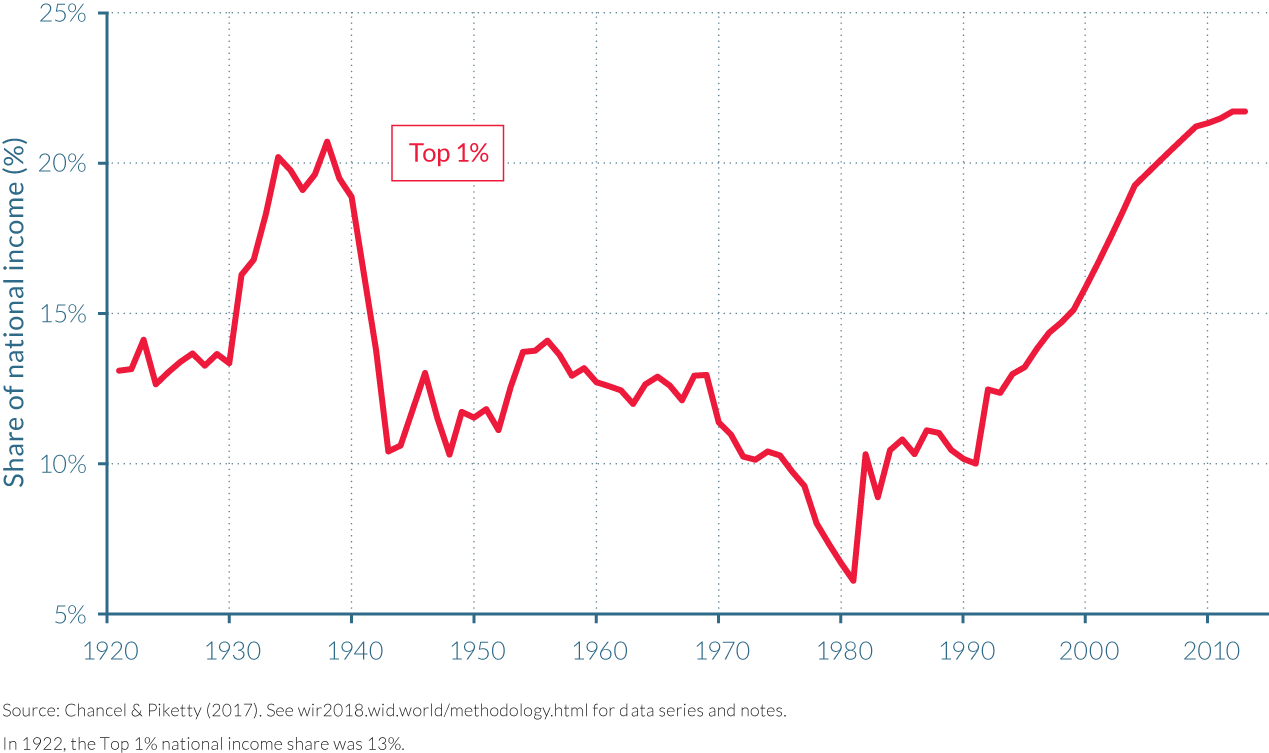

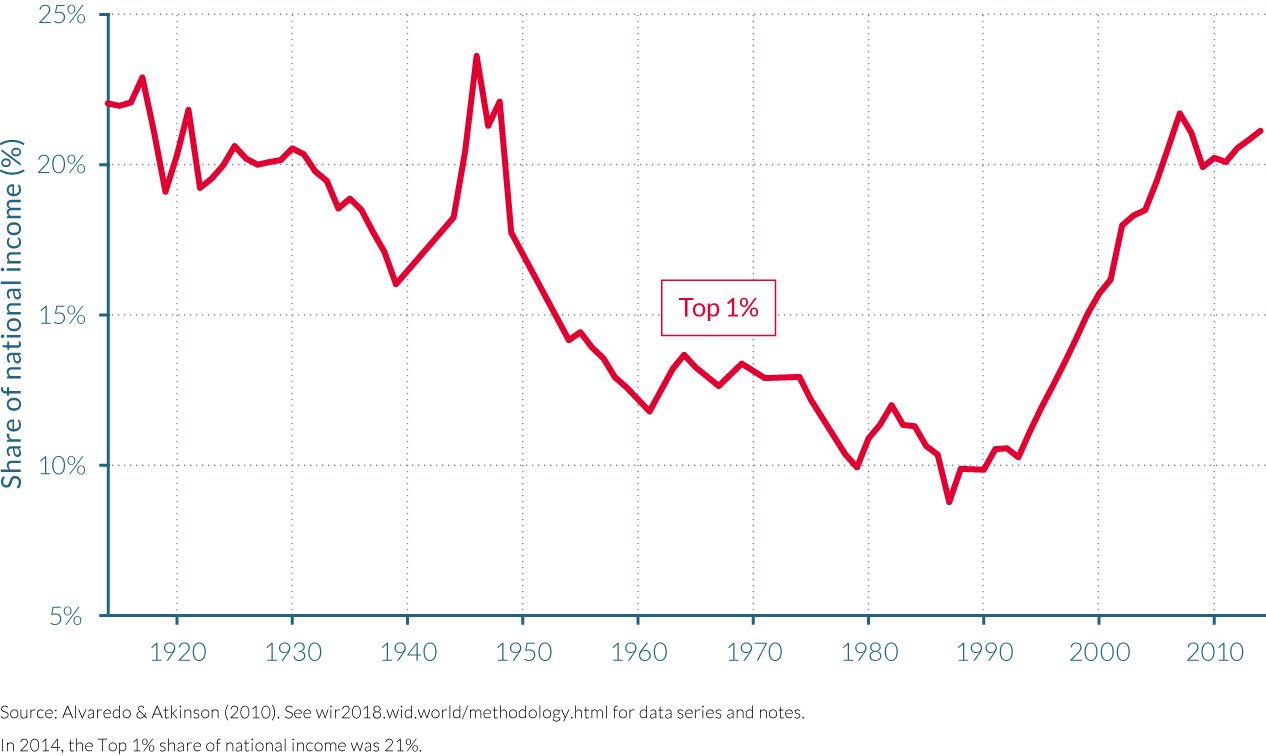

Top 1% income shares have been steadily increasing in Anglo-Saxon countries since the early 1980s, after a historical decline throughout the first part of the twentieth century (see Figure 2.3.1). Inequality exploded in the United States: the top percentile income share there was less than 11% in 1980, and it was slightly above 20% in 2014. Britain's top percentile share rose from less than 6% in the late 1970s to nearly 14% in the mid-2010s. Britain had the same level of top 1% income share as Ireland in the late 1970s, but is now nearly on a level with Canada, where the top share increased from less than 9% in 1980 to almost 14%. Australia and New Zealand, with levels of inequality much lower throughout the entire period (around 5% in the early 1980 and rising to less than 10%) also show a broadly similar pattern.8 The impact of the financial crisis is visible on top-income shares, which exhibit a marked declined after 2007. Novel data suggest that top incomes have either recovered their shares or are progressively recovering them.

Figure 2.3.1

Top 1% national income share in Anglophone countries, 1920–2015

The rise in labor income inequality played an important role in the rise of inequality in Anglo-Saxon countries, and particularly in the United States before the turn of the century, as discussed in chapter 2.4. This phenomenon is owing to the "rise of super managers"—that is, the rise in super wages received by CEOs of large financial and nonfinancial firms. This evolution was also accompanied by an increased polarization of income between low-wage and high-wage firms. This contrasted with European countries, where the dynamics at the top of the distribution have been more moderate. New estimates also show that the upsurge in top incomes has mostly been a capital income phenomenon after 2000 in the United States, shedding new light on the process of unequal growth generation.

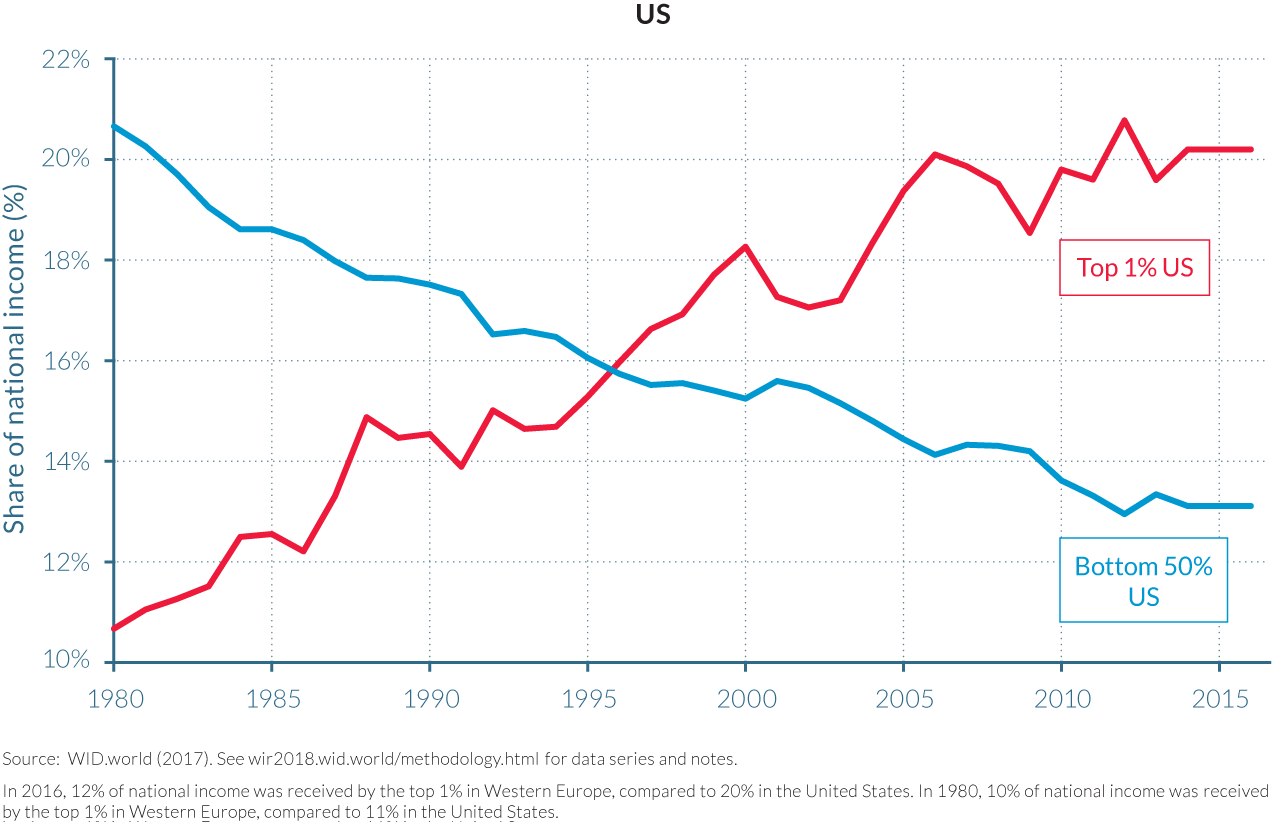

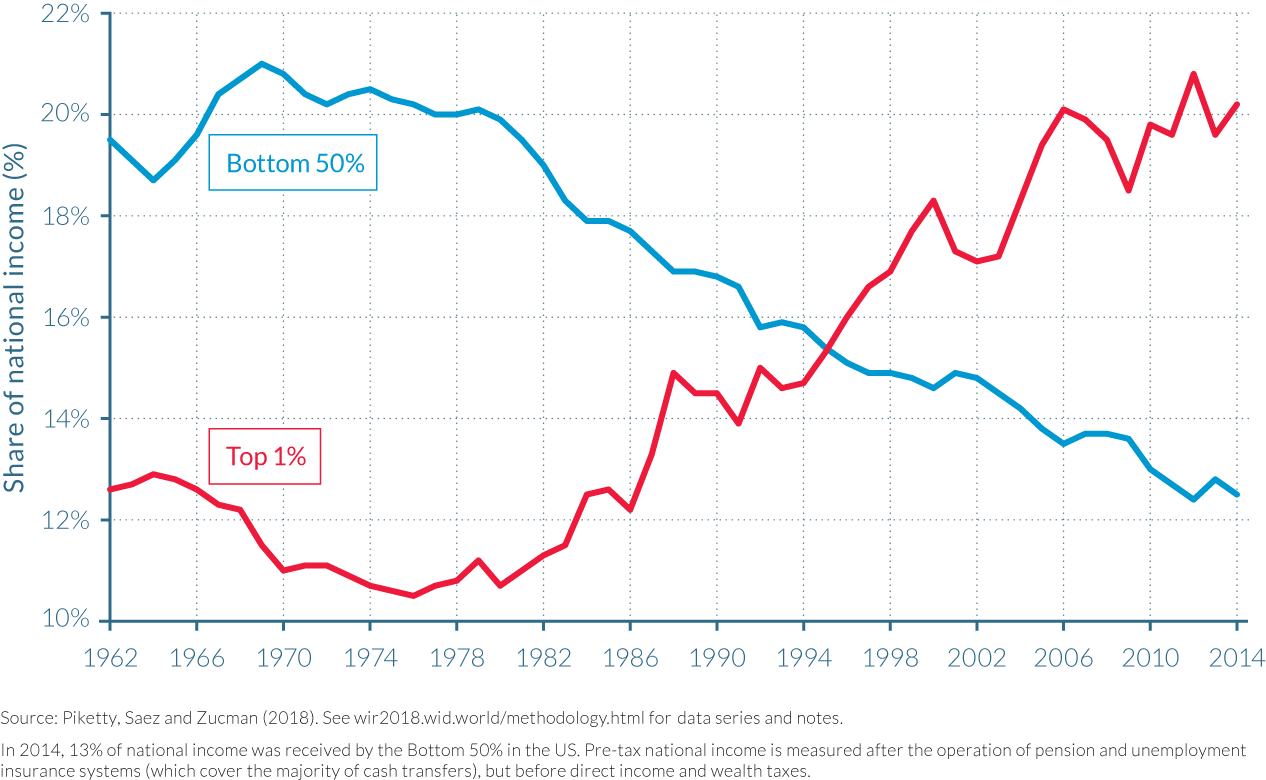

Our novel estimates also allow a better understanding of the dynamics at the bottom of the distribution—at least for certain countries. In the United States, the bottom 90% of the population benefited from a large share of growth in the three decades following the Second World War. Total per-adult pre-tax income growth for the bottom 50% and for the middle 40% was higher than 100%, while total growth for the top 10% earners was less than 80%. But since the 1980s, the bottom 50% was shut off from national income growth. While average per-adult pre-tax incomes increased by 60%, growth was close to zero for the bottom 50% of the population. The bottom 50% did benefit from a very modest post-tax income growth, thanks to redistribution, but this has been eaten up by rising health spending. Government provided little support to help low-income individuals cope with the situation.

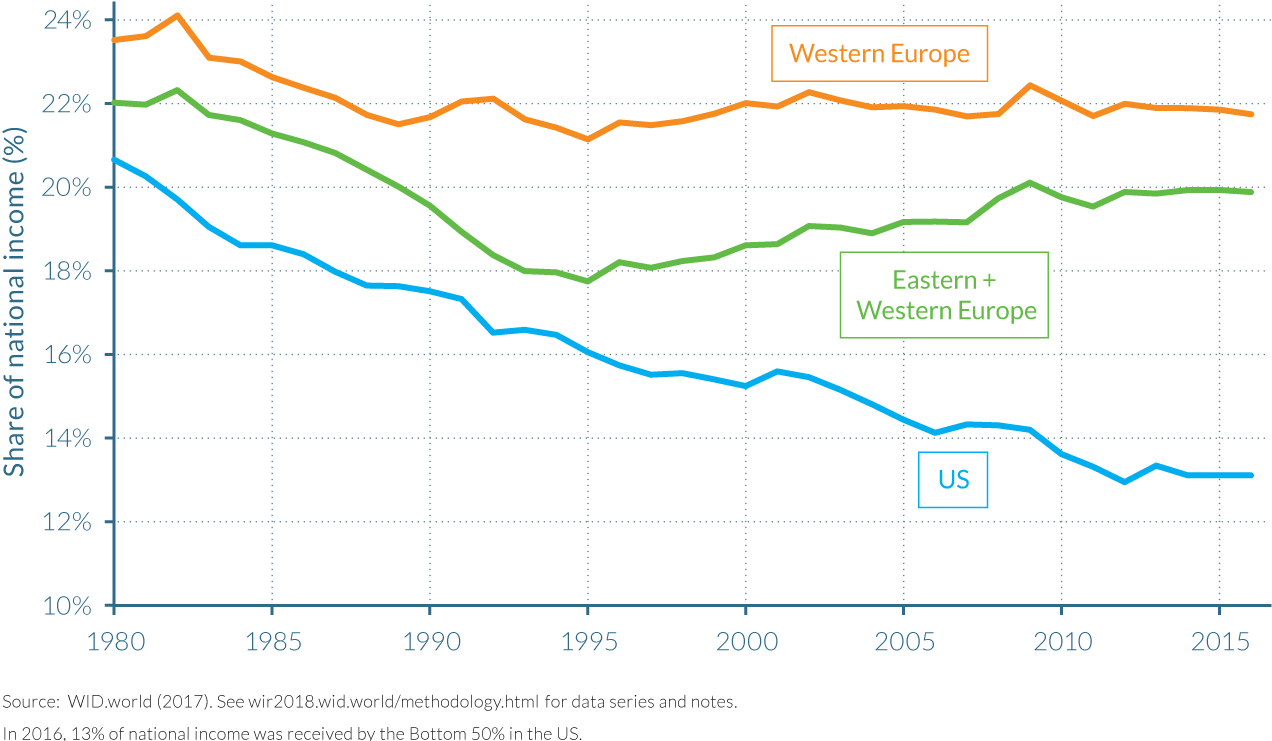

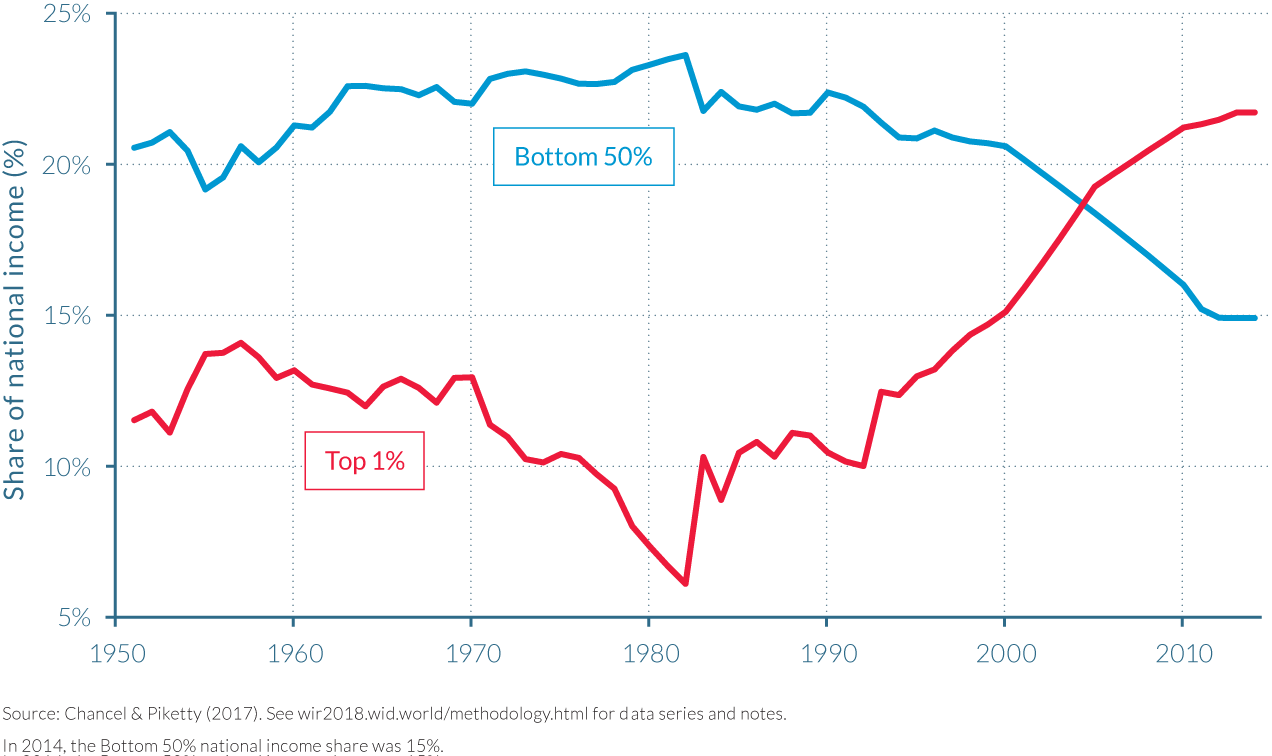

The comparison of inequality trajectories between the United States and Western Europe is particularly striking. The two regions had similar levels of inequality in 1980 (top 1% share at 10–11% and bottom 50% share at 21–23%). However, today, the situations are radically different as the relative positions of the bottom 50% and top 1% group in the United States have been inverted (see Figure 2.3.2a).

Figure 2.3.2a

Top 1% vs. Bottom 50% national income shares in the US and Western Europe, 1980–2016

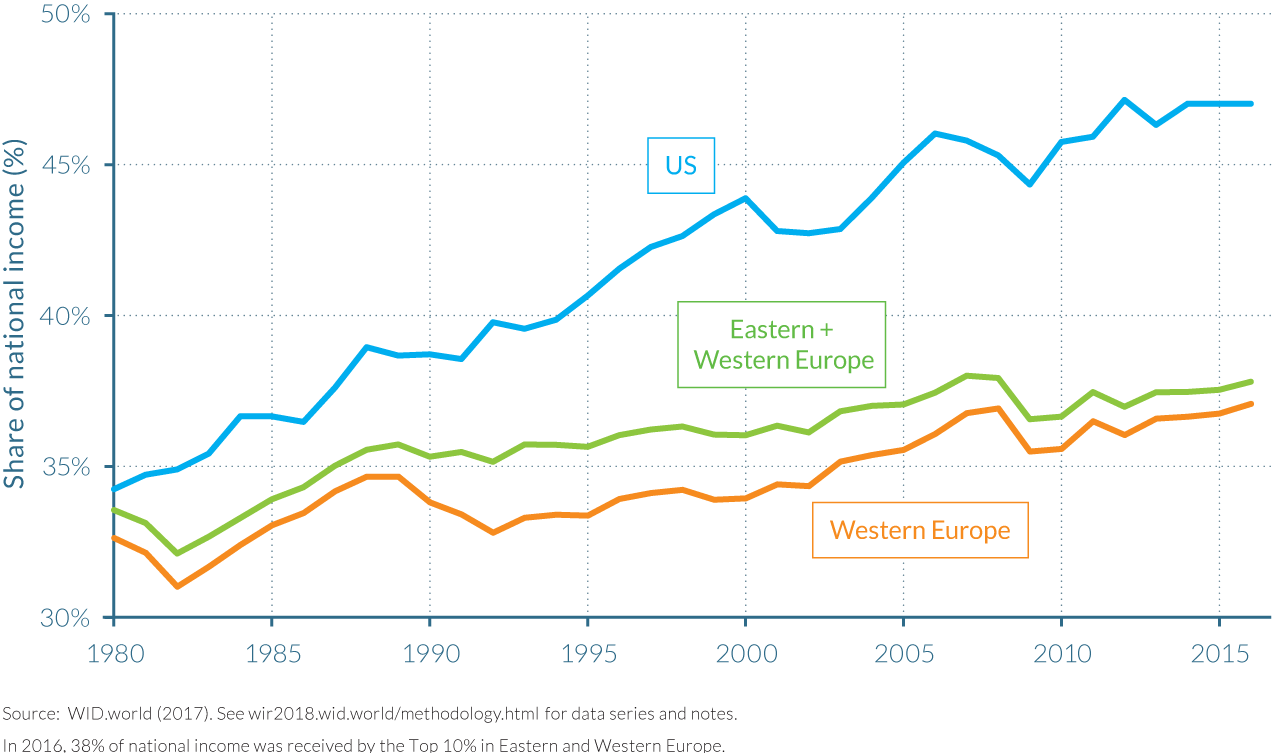

Inequality in enlarged Europe (with a population of 520 million) is now substantially smaller than in the United States (320 million)

We also compare in Figures 2.3.2b through 2.3.2c the evolution of income inequality between the United States, Western Europe, and enlarged Europe (that is, including Eastern Europe). Enlarged Europe includes ex-communist East European countries with lower average incomes than West European averages, leading to higher inequality levels. However, it is striking to see that inequality levels in enlarged Europe remain much smaller than in United States. In particular, in spite of Europe's bigger size and potential heterogeneity (520 million for enlarged Europe, 320 million for the United States), the bottom 50% income share is substantially larger in Europe: 20–22% of total income at the end of the period versus 12% in the United States.

This conclusion would likely be exacerbated if we were to compare enlarged Europe to enlarged North America (including not only Canada but also Mexico), which we plan to do in the near future as new data become available for Mexico. Another important issue for future research is to better understand which part of Europe's lower inequality level can be attributed to redistributive policies at the regional level (including EU regional development funds), as opposed to national factors (such as the relatively egalitarian legacy of Eastern European countries and the fact that the transition from communism was not as abrupt as in Russia).

Figure 2.3.2b

Top 10% national income share in Europe and the US, 1980–2016

Figure 2.3.2c

Bottom 50% national income share in Europe and the US, 1980–2016

Continental European countries were more successful in preventing the rise of incomes at the top and the stagnation of incomes at the bottom

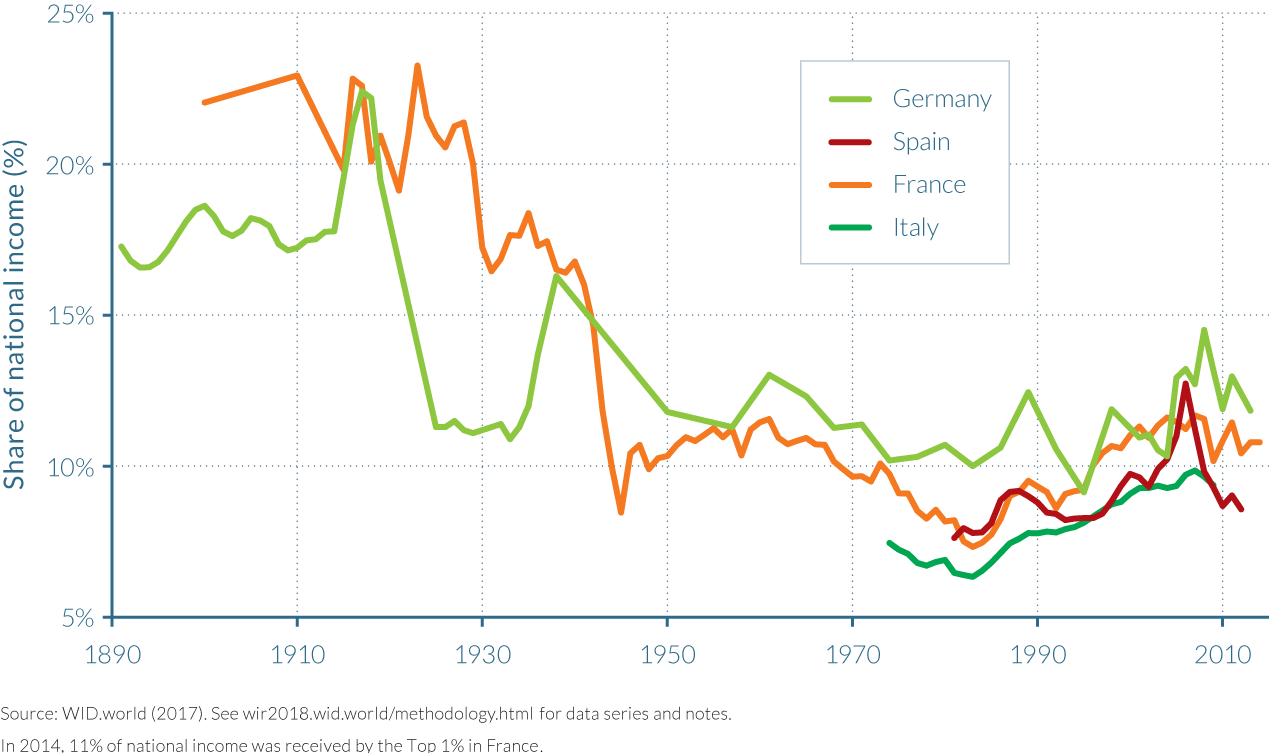

In western continental Europe, inequality has also been on the rise since the late 1970s, though both the levels of inequality and the rise in inequality were less striking than in the United States. The German top 1% income share rose from slightly less than 11% in the early 1980s to 13% today, as described in chapter 2.6. In France, the top 1% pre-tax income share increased from approximately 7% in 1983 to nearly 11% in 2014, as discussed in more detail in chapter 2.5. Spain displays a different picture. The impact of the financial crisis and the bursting of the real estate bubble in 2007–2008, which represented a substantial share of national income, severely hampered incomes at the bottom of the distribution, but also at the top: the top 1% income share decreased from close to 13% in 2006 to less than 9% in 2012, and still shows no sign of recovery. (Figure 2.3.3)

Figure 2.3.3

Top 1% national income share in European countries, 1890–2014

For France, new estimates also allow us to track the dynamics of growth at the bottom of the distribution. While growth was higher than average at the bottom 50% and middle 40% during the postwar period and up to the early 1980s, the situation was reversed afterwards. The "thirty glorious years"—as the high-growth 1950–1980 period is commonly referred to in France—continued after the 1980s, but only for the top income earners. This increase in inequality is characterized by rises in both labor and capital income. However, the bottom half of the population was not shut off from growth after the 1980s. This part of the population enjoyed close to average income growth rates—a strikingly different picture than in the United States.

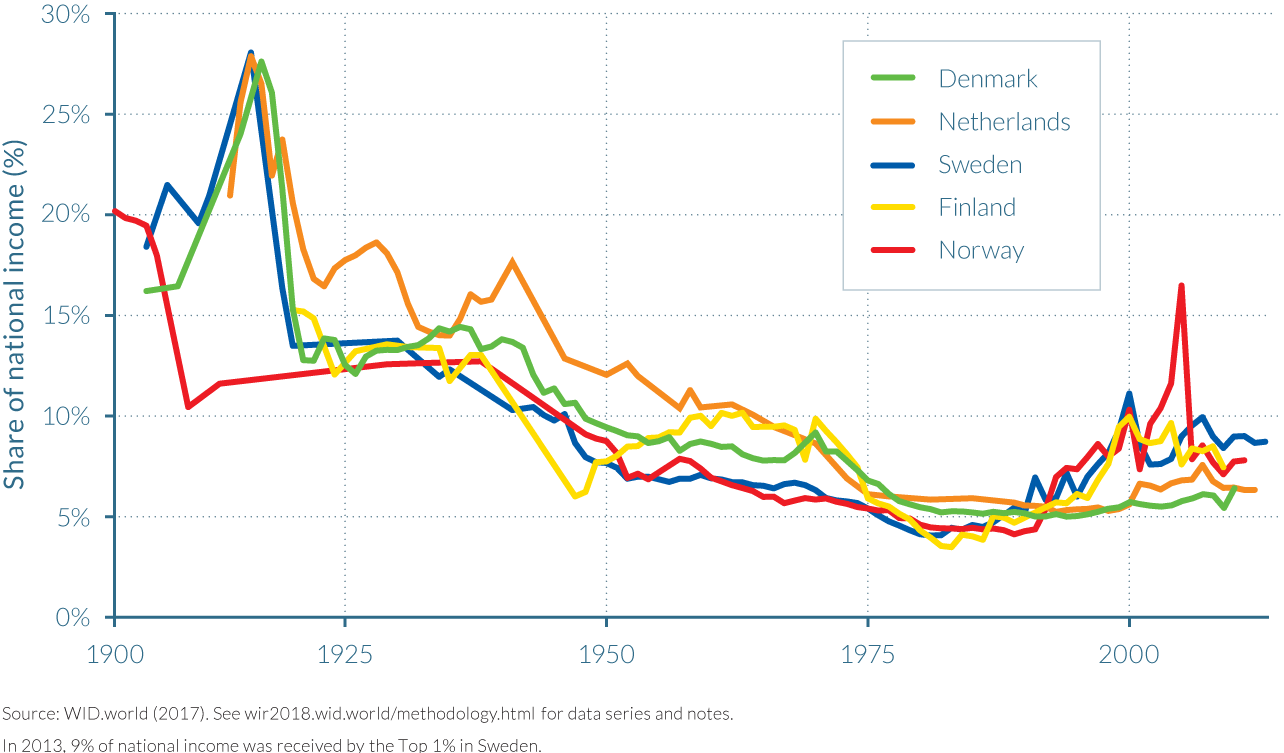

Northern European countries had among the lowest levels of income inequality in the world in the early 1980s. Growth has been more unequal in these countries after 1980 than before, yet income concentration at the top of the distribution remains limited. Top 1% income earners capture less than 10% of total income in Denmark, Finland, Norway, and Sweden. In Denmark and in the Netherlands, the rise in top percentile share has been small, from about 5% to 6% since the 1980s. As we can see, many European countries have been able to generate relatively high average income growth rates and maintain the rise in income inequality (Figure 2.3.4).

Figure 2.3.4

Top 1% national income share in Northern European countries, 1900–2013

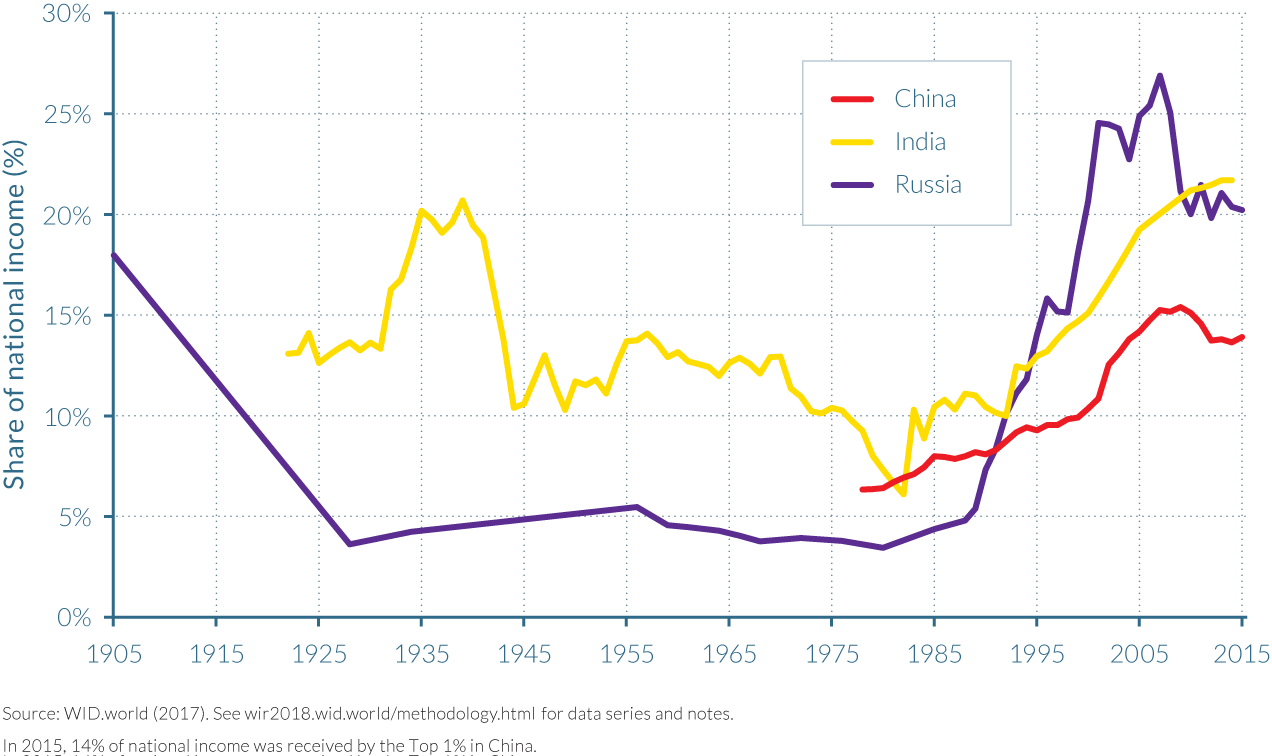

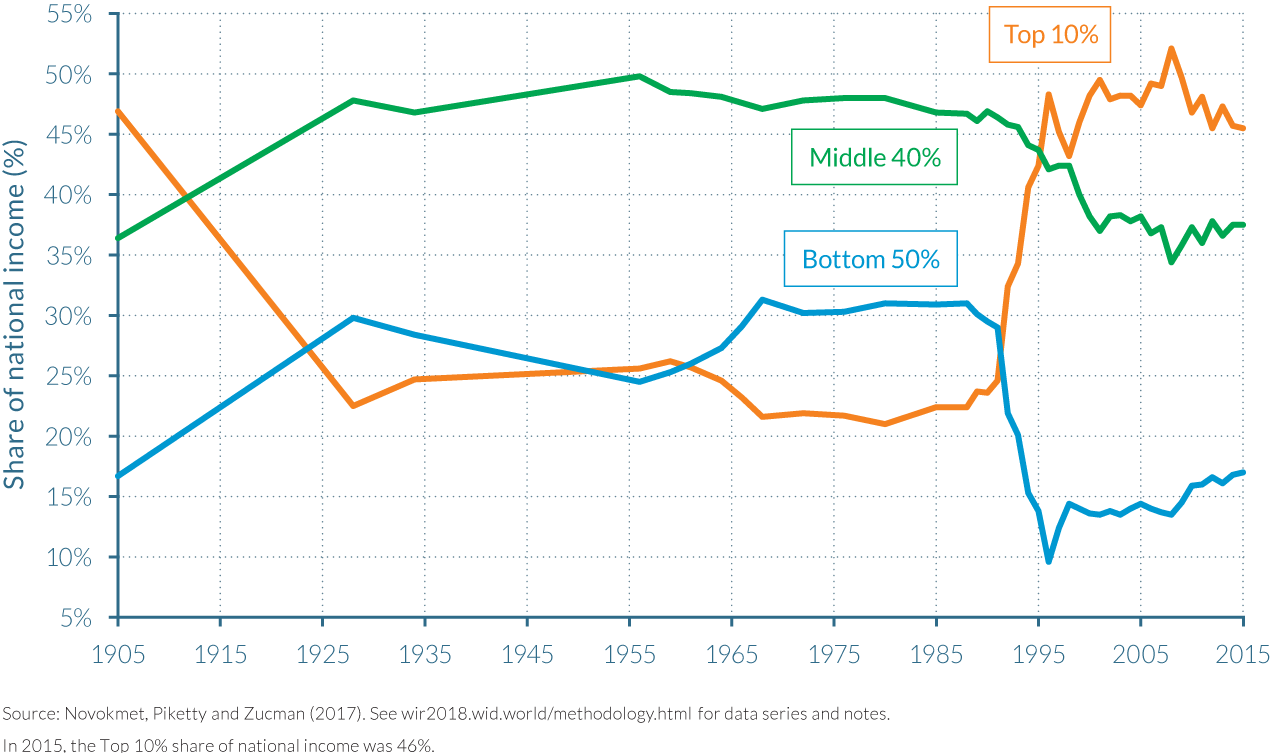

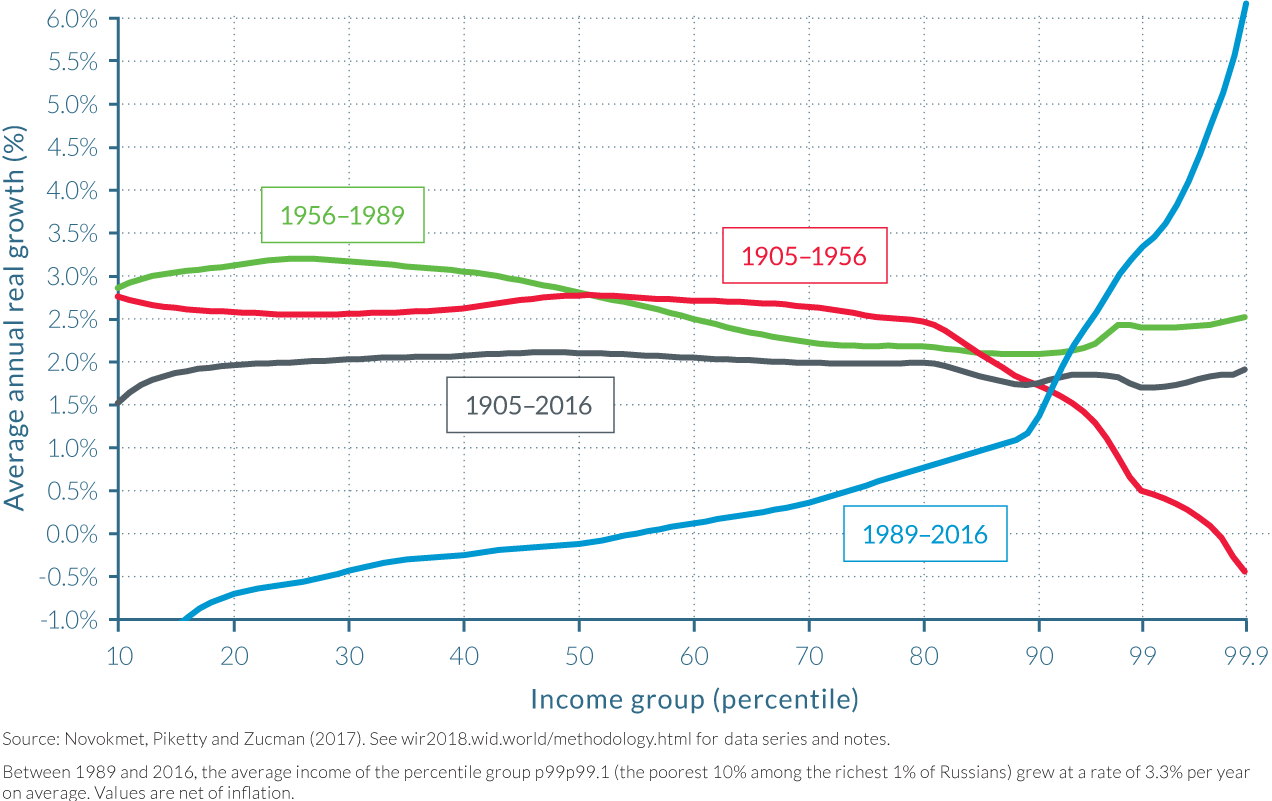

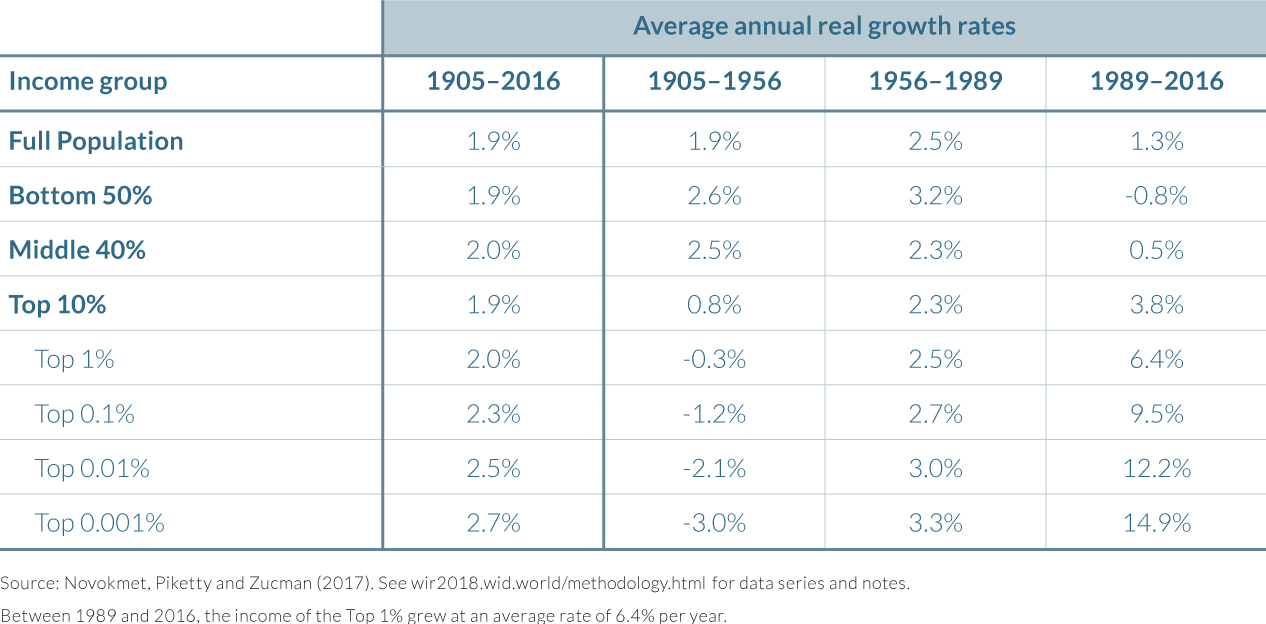

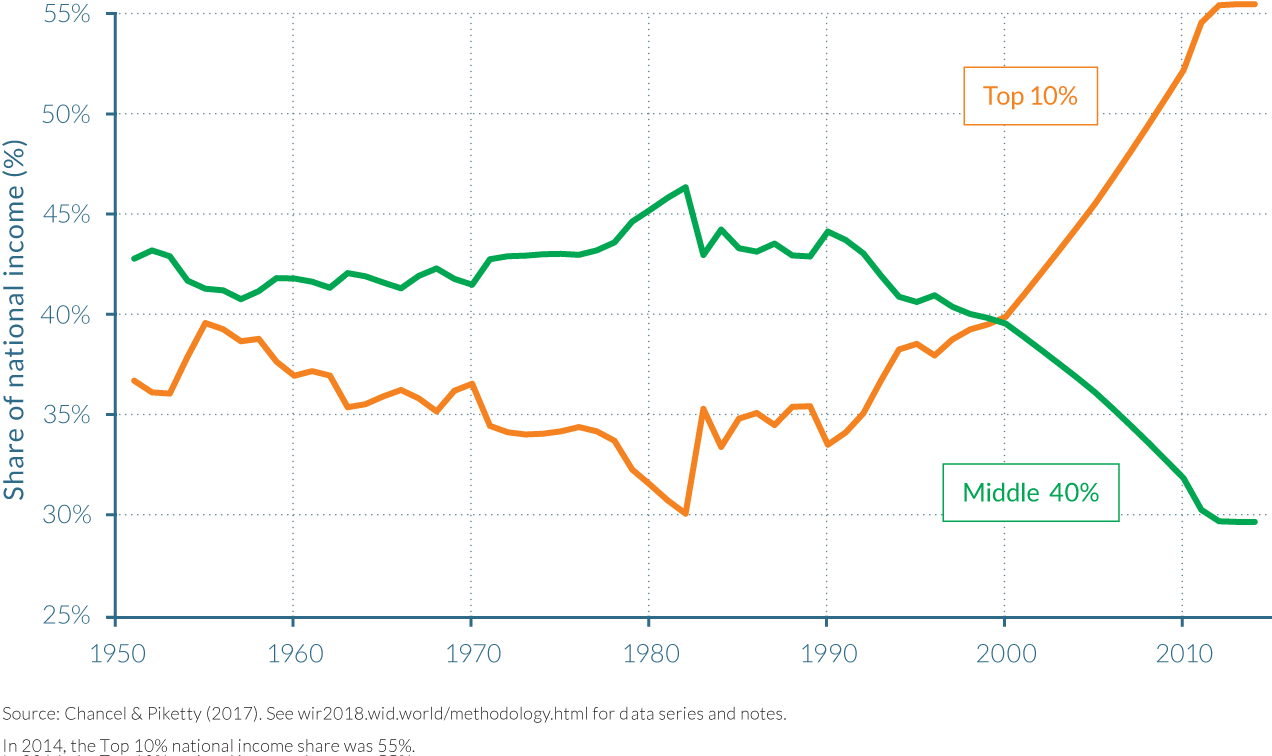

In Russia, China, and India, income inequality surged after the 1980s

Income concentration and wealth concentration were particularly high in tsarist Russia before the Soviet revolution of 1917 (see chapter 2.8 on Russia), and in colonial India (see chapter 2.9 on India). In Russia, the communist revolution led to an extreme compression of money incomes. During the entire communist period, the top 1% income share represented around 5% of national income, down to less than 4% in the seventies (see Figure 2.3.5). It is worth stressing, however, that this extremely low level of monetary inequality is partly artificial. Soviet inequality took other, non-monetary forms, such as privileged access to particular shops and vacation centers for the political elite, and brutal political repression for large segments of the population.

In India, the top percentile income share decreased from around 20% at the end of the colonial period to 6% in the early 1980s, after four decades of socialist-inspired policies aiming at reducing the economic power of the elite, including nationalizations, government control over prices, and extreme tax rates on top incomes. The implosion of the Soviet block and "shock policies" in Russia, and deregulation and opening policies in India from the 1980s onwards, contributed to strong increases in top percentile income shares. The top 1% share increased to 26% in 1996 in Russia and is now at 20%. In India, the top percentile is now around 22%.

Figure 2.3.5

Top 1% national income share in emerging countries 1900–2015

The Chinese opening-up policies established from 1978 (discussed in chapter 2.7 on China), which included important privatization plans, had a lesser effect on inequality than reforms had in Russia or India. China shows a substantial rise in inequality (the top share rose from 6.5% to 14% in twenty years). However, as compared to Russia, China's transition to a liberalized, open economy was less abrupt and more gradual. Since 2006, inequality at the top has stagnated. In China and to a lesser extent in India, the rise in inequality occurred in the context of high average income growth, enabling important growth at the bottom of the distribution.

Brazil, South Africa, and the Middle East can be characterized as "extreme inequality" regimes: they have the highest inequality levels observed

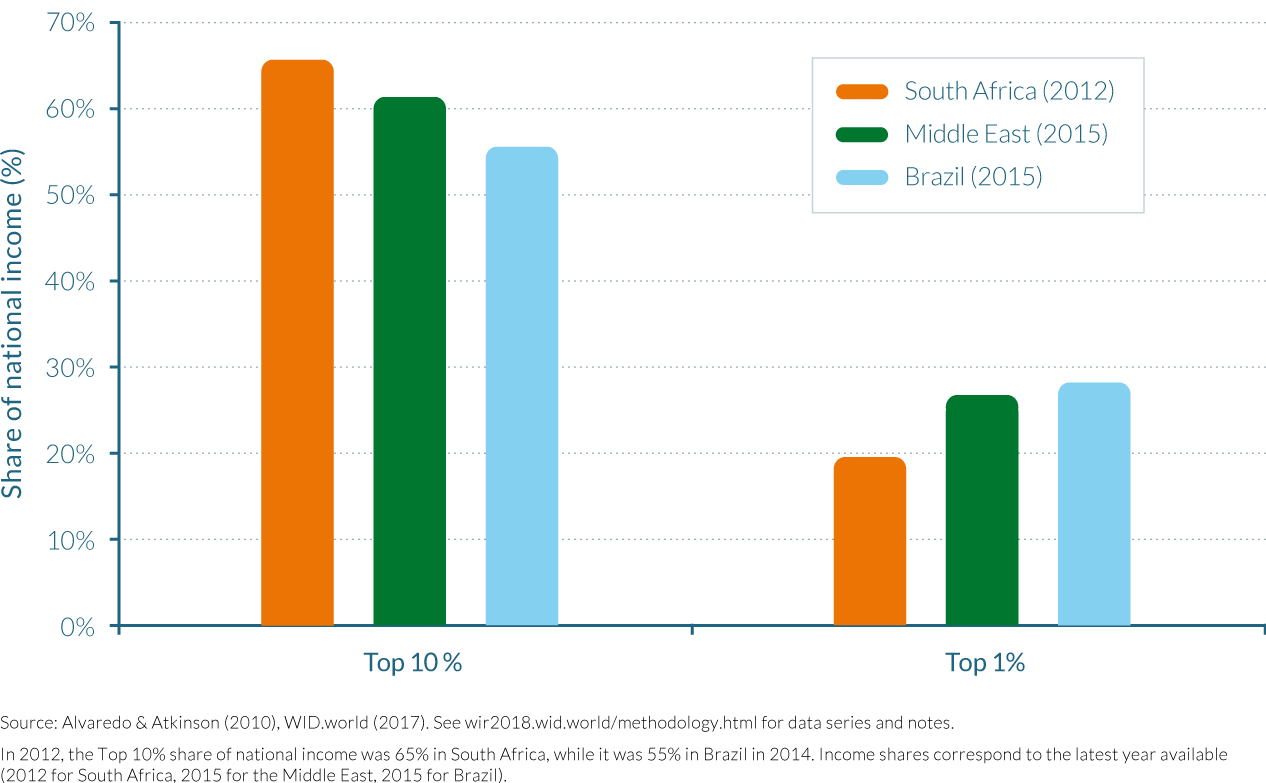

In Brazil, South Africa, and the Middle East, income has been historically highly concentrated (see Figure 2.3.6). In Brazil, wage inequality has decreased over the past twenty years (in particular due to rising minimum wage) and there have been important and often lauded cash-transfer systems to the poor. However, due to a large concentration of business profits and capital incomes, the top 10% national income share reaches 55% in Brazil today and this value has not changed significantly for the past twenty years as is shown in chapter 2.11. Together with huge regional inequalities, the legacy of racial inequality still plays an important role; Brazil was the last major country to abolish slavery, back in 1887, at a time when slavery made up a very large fraction of the population, up to about 30% of the population in certain regions.

Figure 2.3.6

Top 10% national income share in Brazil, the Middle East, South Africa and other countries, 2012–2016

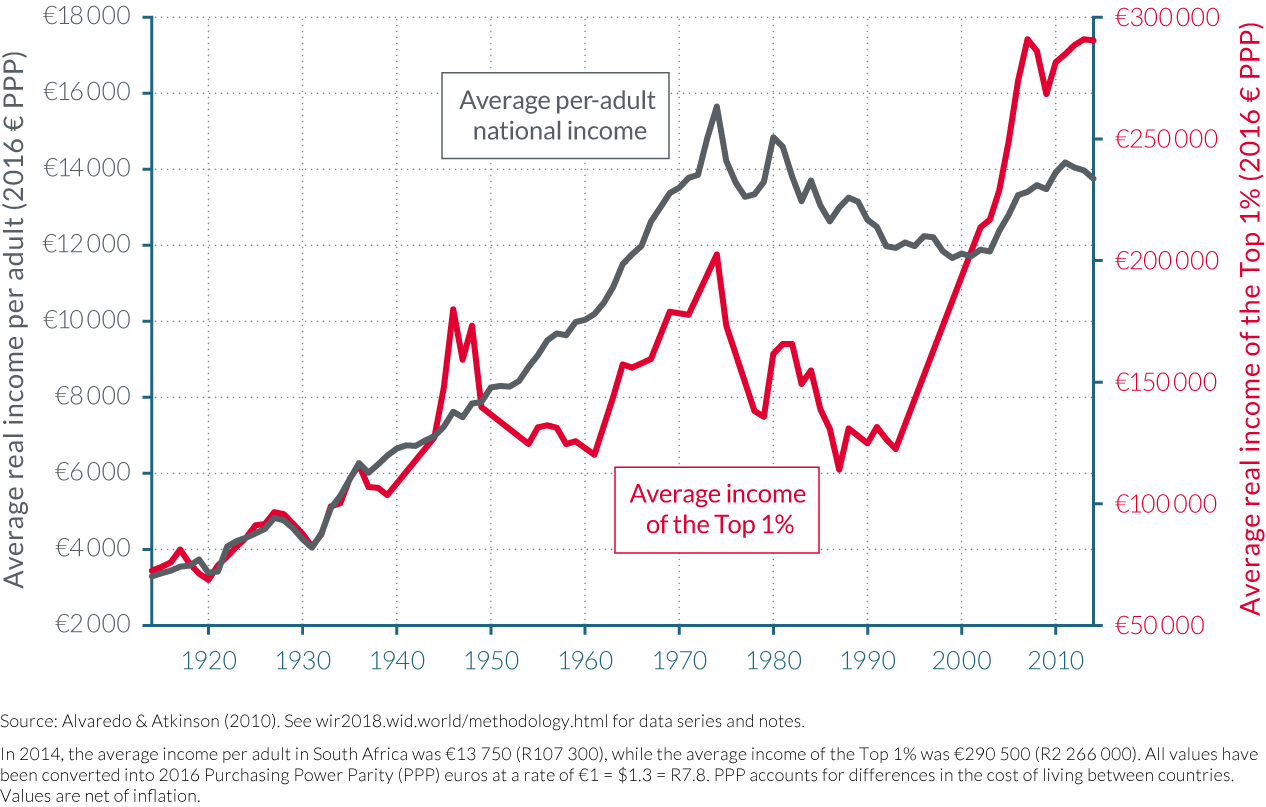

The extreme inequality evident in South Africa can obviously be linked to the historical legacy of the apartheid regime (only fully abolished in 1994), seen today in the country's dualistic economy and society. As discussed in chapter 2.12, the top 10% is largely made up of whites. This group earns more than 60% of national income and enjoys income levels similar to those of Europeans, while the bottom 90% live with incomes comparable to those of low-income African countries. But in contrast to Brazil and the Middle East, inequality increased significantly over the past decades in South Africa. The trade and financial liberalization that occurred after the end of apartheid, coupled with the failure to redistribute land equally, can help to explain these dynamics - yet more research will be required to better track and understand recent South African income inequality dynamics.

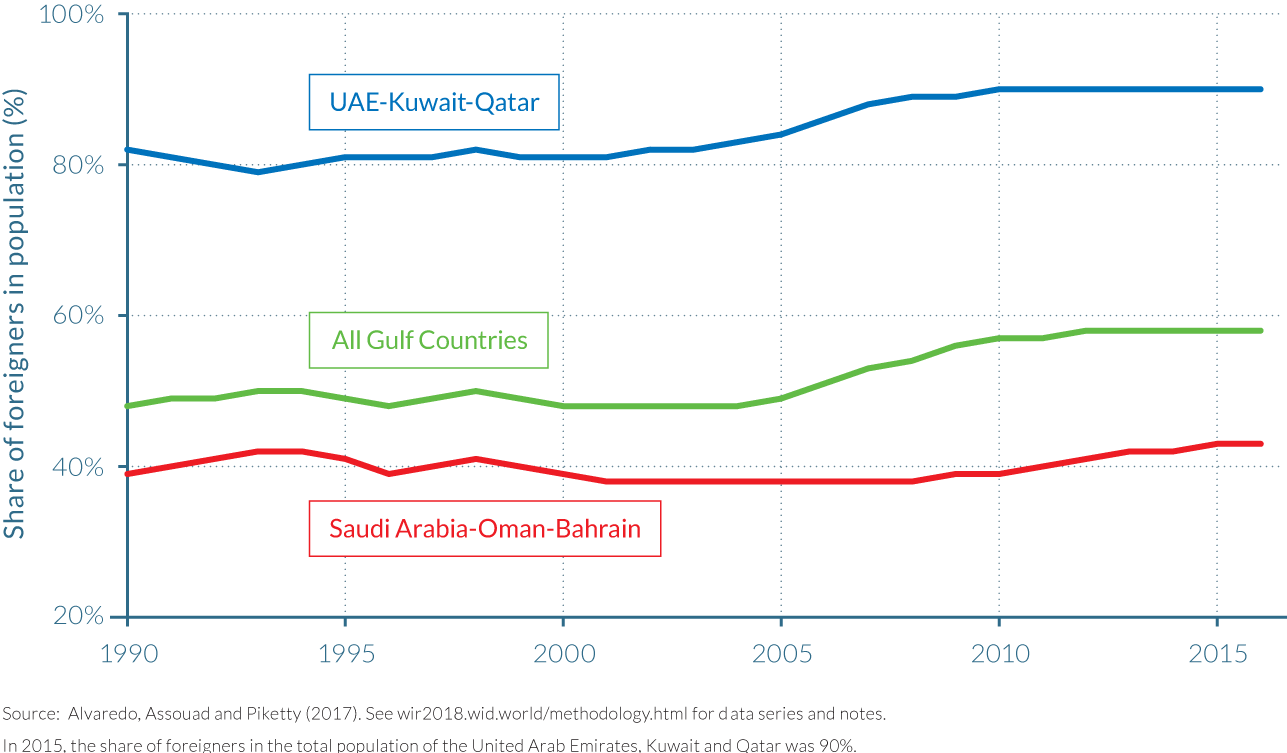

Despite its much larger racial and ethno-cultural homogeneity, levels of inequality in the Middle East are similar to (or possibly even higher than) those in Brazil and South Africa, with a top 10% share above 60%. As discussed in chapter 2.10, regional income and wealth is largely concentrated in in the hands of a small group that is located in the Gulf countries and Saudi Arabia. This is yet another inequality-generating mechanism: the geography of oil property and the frontier system have led to extreme inequality in this region.

In low-income countries, inequality is likely to be higher than previously thought, but data is scarce

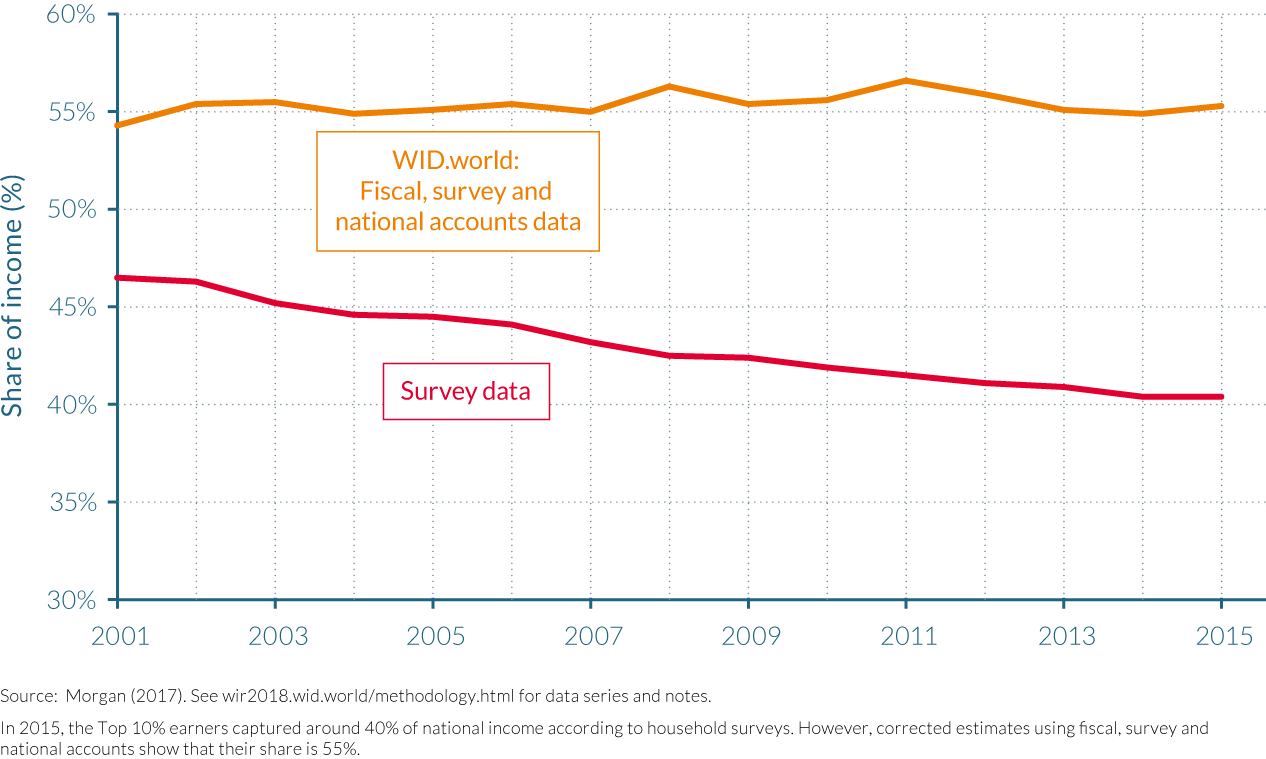

We still know very little about the evolution of income inequality in the rest of the developing and emerging world. The first explanation for this situation is that there is a lack of proper income-tax data, either because governments have not shared it, or because the data simply do not exist anymore, or because the data are still decentralized and not digitized.

In the absence of administrative data, most of what we know is based on survey estimates. As discussed in Part I, survey-based estimates of inequality can have a number of limitations. Surveys are often more sporadic in time, lack consistency with national accounts estimates, and miss top incomes. As demonstrated in this report, for numerous emerging countries, these weaknesses can lead to significant underestimation of inequality levels. (See chapters 2.7 and 2.12.) In Côte d'Ivoire, novel estimates show that the income share of the top 1% is approximately 17% of the country's total income, contrary to the 12% previously estimated by surveys. WID.world work also shows that the share of income earned by the top 1% in China was at least twice as great as official estimates previously suggested. We are currently devoting great energies to accessing income tax data in other African countries, following the lead of Côte d'Ivoire, and hope to be able to report more findings in the near future. At this stage, however, we have only limited access to adequate data.

Collectively, these factors mean that we can assess the evolution of income inequality for only a few developing countries in the years before the 1980s, and over a short or interrupted time period. Given that most individuals earned below the first income-tax threshold, our analysis is also restricted to a tiny fraction of the population. Out of the nine sub-Saharan African countries for which we have historical income tax data, the income share earned by the top 1% can only be properly computed in two small countries—Mauritius and the Seychelles—and for only a few years in Zambia and Zimbabwe. For the remaining countries (Ghana, Kenya, Tanzania, Nigeria, and Uganda), the income-tax data encompass less than 1% of the estimated adult population. While this may appear surprising, it is worth remembering that in the early days of the US personal income tax (1913–1915), the proportion of taxpayers was 0.9%.

Nevertheless, some lessons can be drawn from this data. In Africa, from the mid-1940s until the early 1980s, the income share of the top 0.1% decreased in Zimbabwe, Zambia, Malawi, Kenya, Tanzania, and South Africa, following a trend similar to that of most rich countries. But compared to European levels over the same period, income inequality was much higher in these African countries, and even reached the most extreme levels. In 1950, the richest 0.1% of Zambia commanded a bit more than 10% of total national income. Income inequality was, however, seemingly lower in West African countries such as Nigeria and Ghana, where the top 0.1% averaged to 2.5% of total income between 1940 and 1960. Interestingly, this pattern of geographical differences in inequality is still evident in survey data that has been collected in recent decades.

Where it is possible to break down tax data by race or nationality, historical data in African countries demonstrate that most taxpayers were non-African—mainly Europeans, followed by Arabs, then Asians. This dominance is likely to have been mitigated in recent decades, but it is still important in former settlement colonies such as South Africa. Recent research on Côte d'Ivoire for the period 1985–2014 further illustrates how the aforementioned discrepancy between survey data and administrative data can be partly due to the undersampling of non-African individuals.9

Available data for Latin American countries show that income inequality in the region is generally higher than the levels seen in European and Asian countries. For example, recent data collected in Latin America indicate that the total income share of the top 1% in Argentina, Colombia, and Brazil is greater than 16%. Interestingly, when only survey data have been used to estimate inequality in the region, the results suggest that income inequality has decreased significantly, while WID.world estimates for Brazil and Colombia show that they have in fact remained stubbornly high.

In conclusion, the scarcity of available data makes it challenging to develop a conclusive picture of inequality levels in lower-income countries. From the data that are available, however, inequality estimations suggest that in most cases the distribution of income is more concentrated than previously thought in low-income countries. While important efforts have been made in the past years to produce and analyze consistent inequality estimates in emerging countries (which are presented for the first time together in this report) the study of the analysis of income inequality based on sound and consistent data in low-income countries is still only in its infancy.

2.4 Income inequality in the United States

Information in this chapter is based on the article "Distributional National Accounts: Methods and Estimates for the United States," by Thomas Piketty, Emmanuel Saez, and Gabriel Zucman, forthcoming in the Quarterly Journal of Economics (2018).

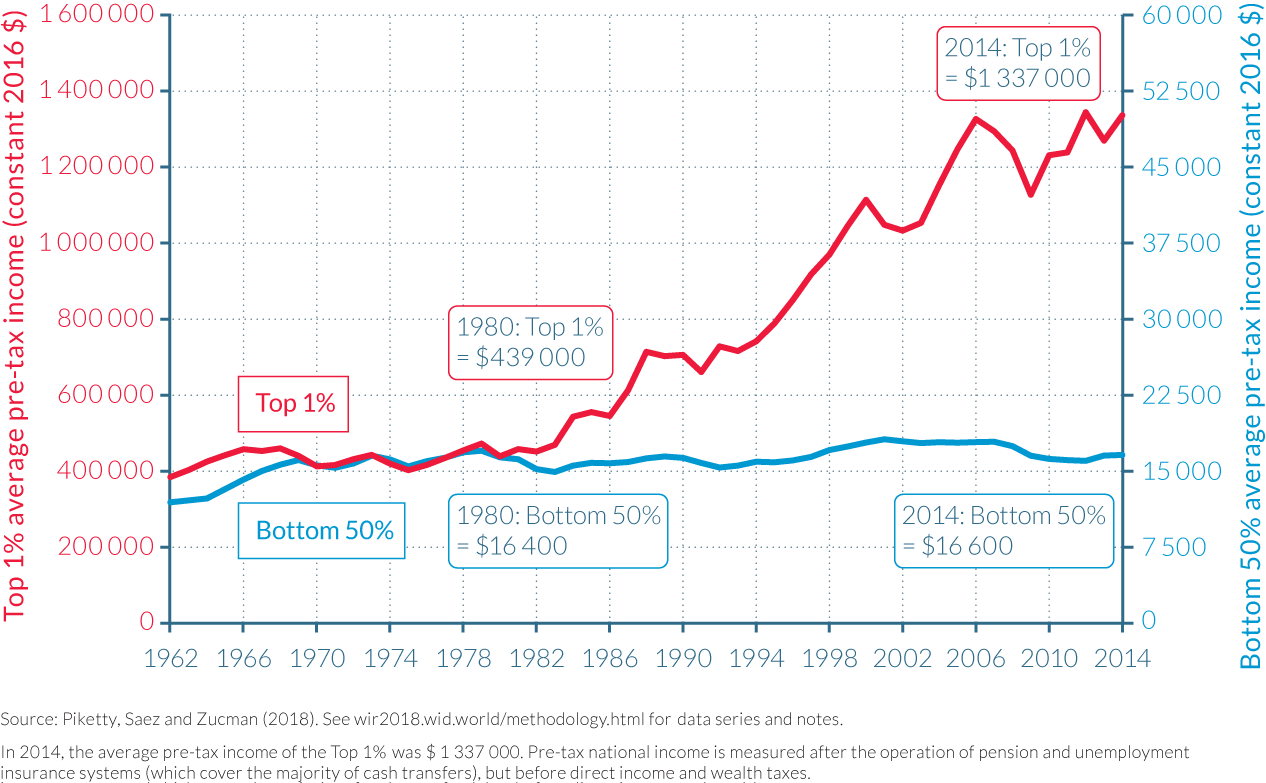

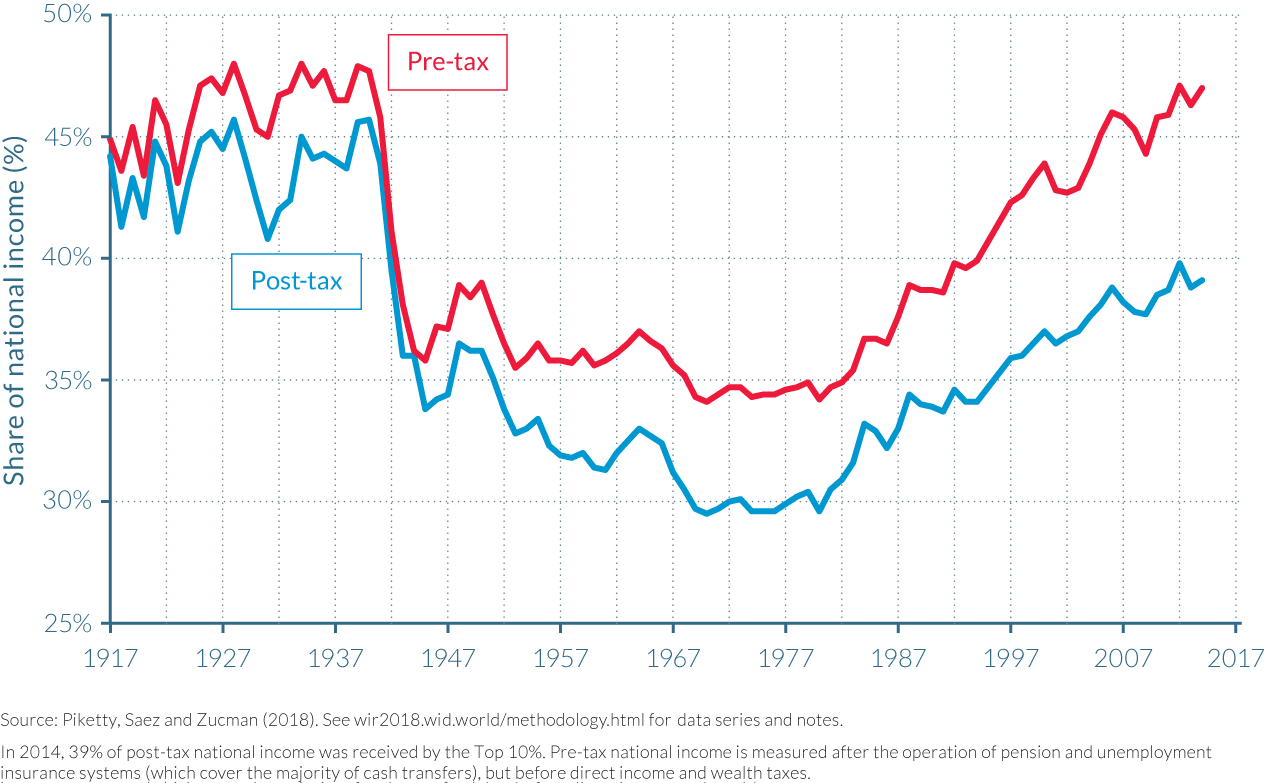

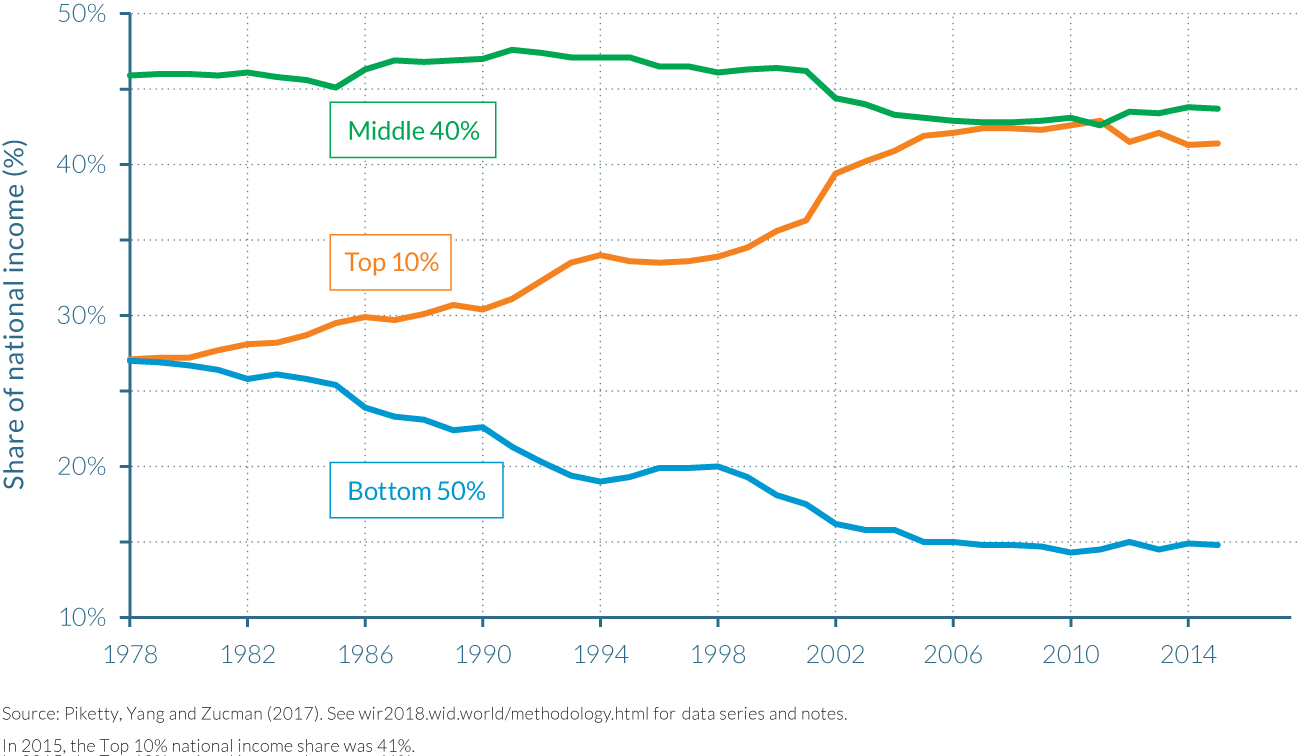

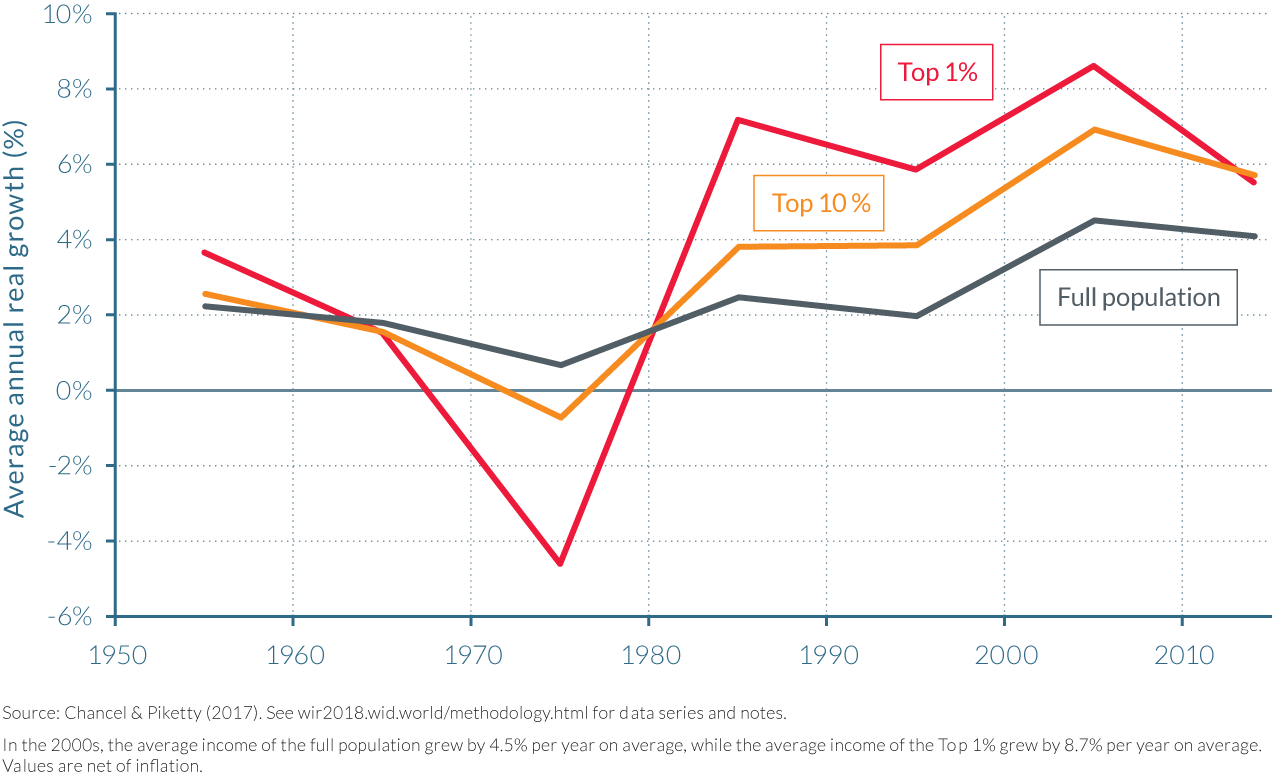

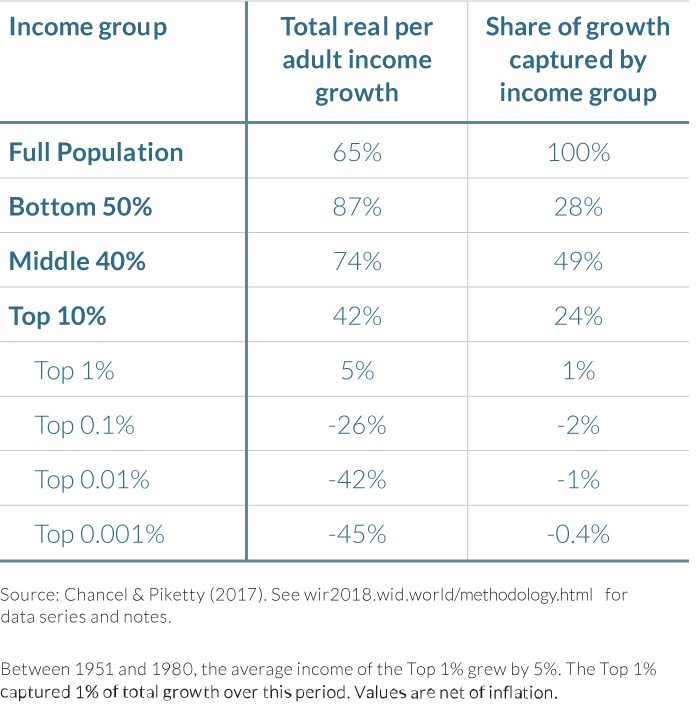

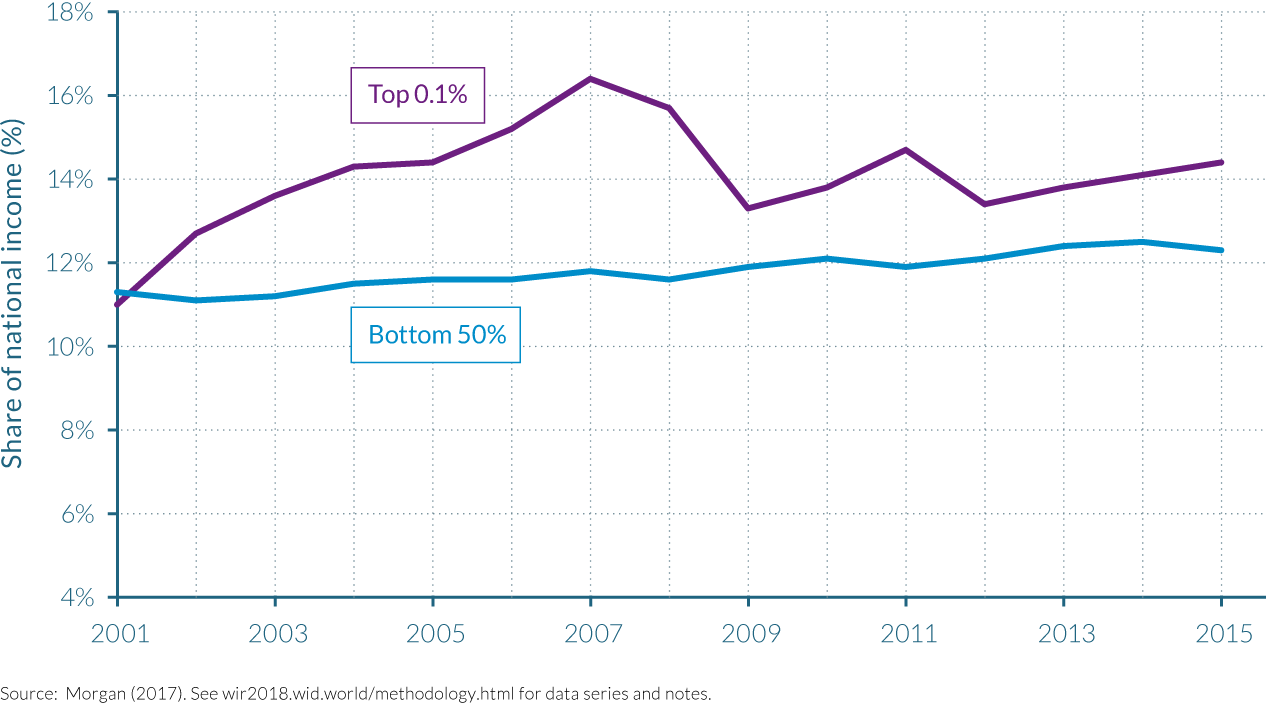

- Income inequality in the United States is among the highest of all rich countries. The share of national income earned by the top 1% of adults in 2014 (20.2%) is much larger than the share earned by the bottom 50% of the adult population (12.5%).

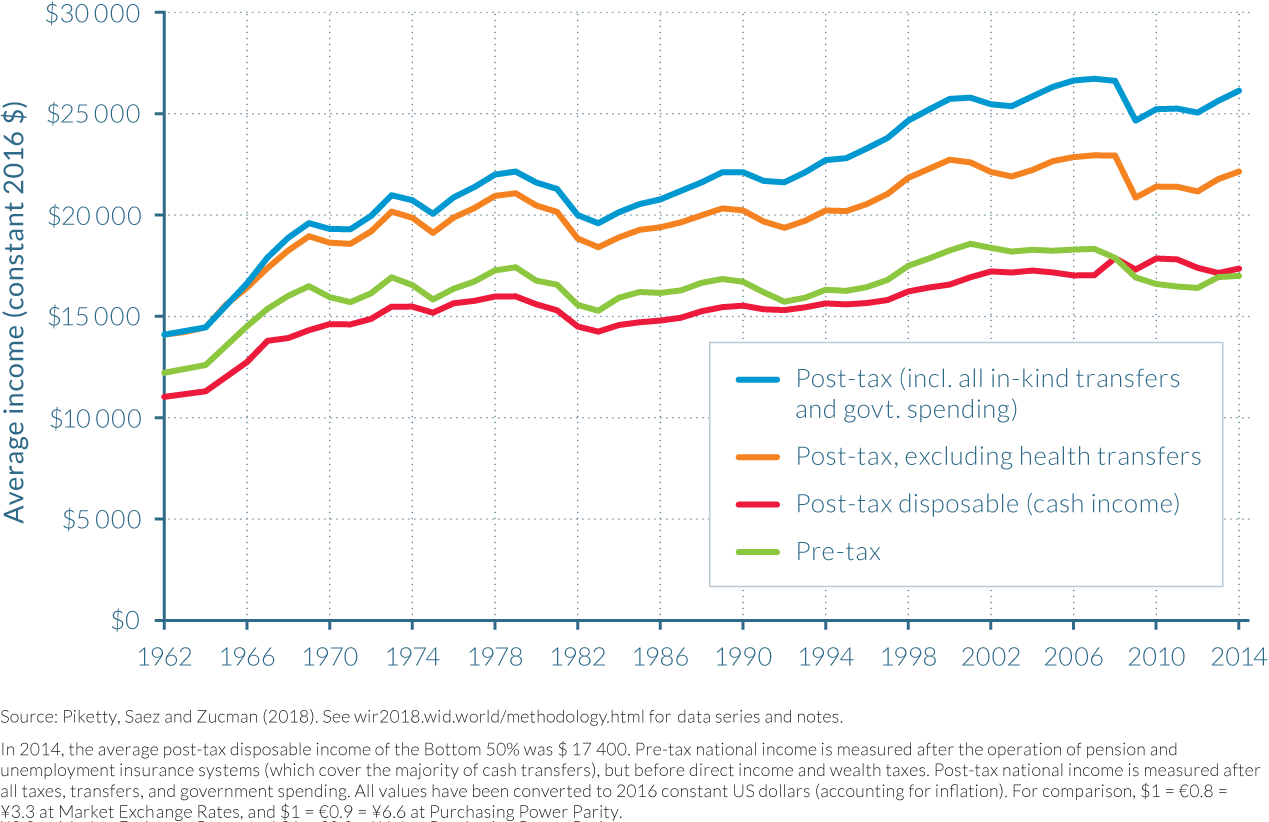

- Average pre-tax real national income per adult has increased 60% since 1980, but it has stagnated for the bottom 50% at around $16 500. While post-tax cash incomes of the bottom 50% have also stagnated, a large part of the modest post-tax income growth of this group has been eaten up by increased health spending.

- Income has boomed at the top. While the upsurge of top incomes was first a labor-income phenomenon in 1980s and 1990s, it has mostly been a capital-income phenomenon since 2000.

- The combination of an increasingly less progressive tax regime and a transfer system that favors the middle class implies that, even after taxes and all transfers, bottom 50% income growth has lagged behind average income growth since 1980.

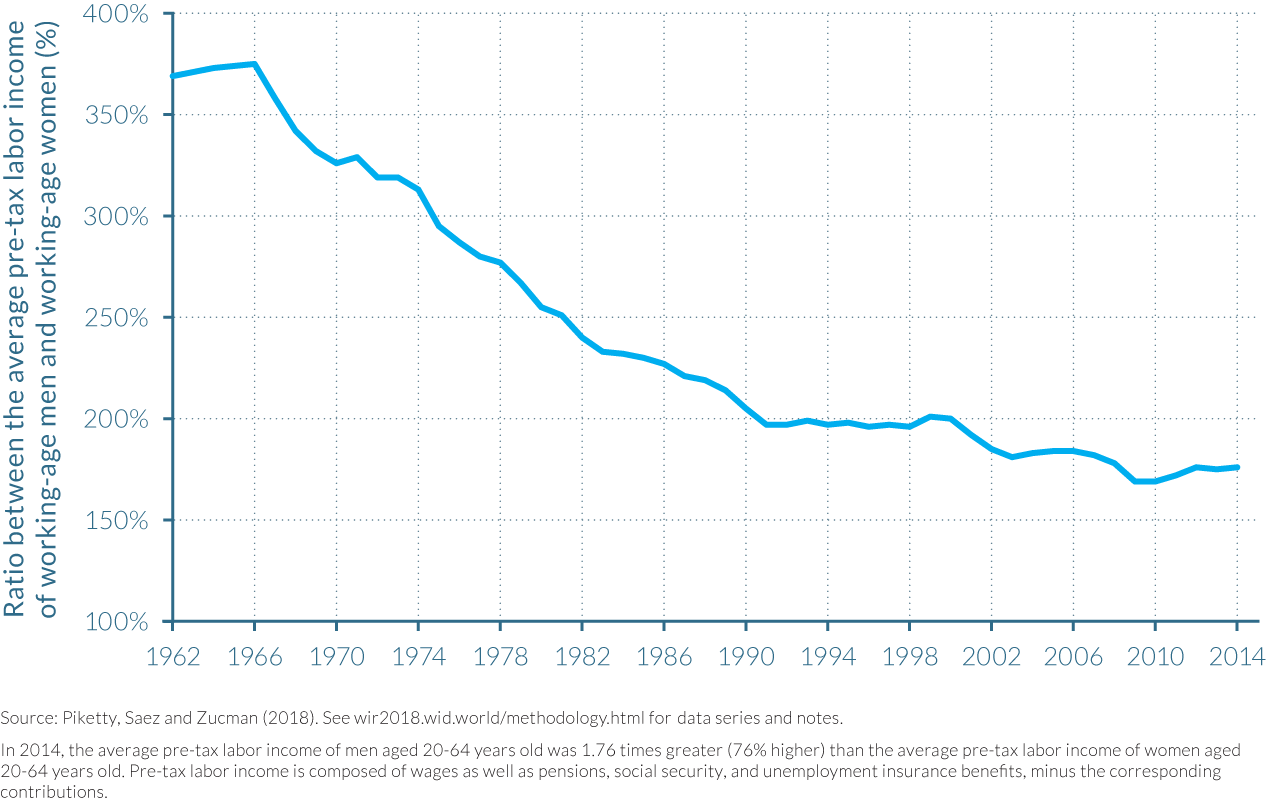

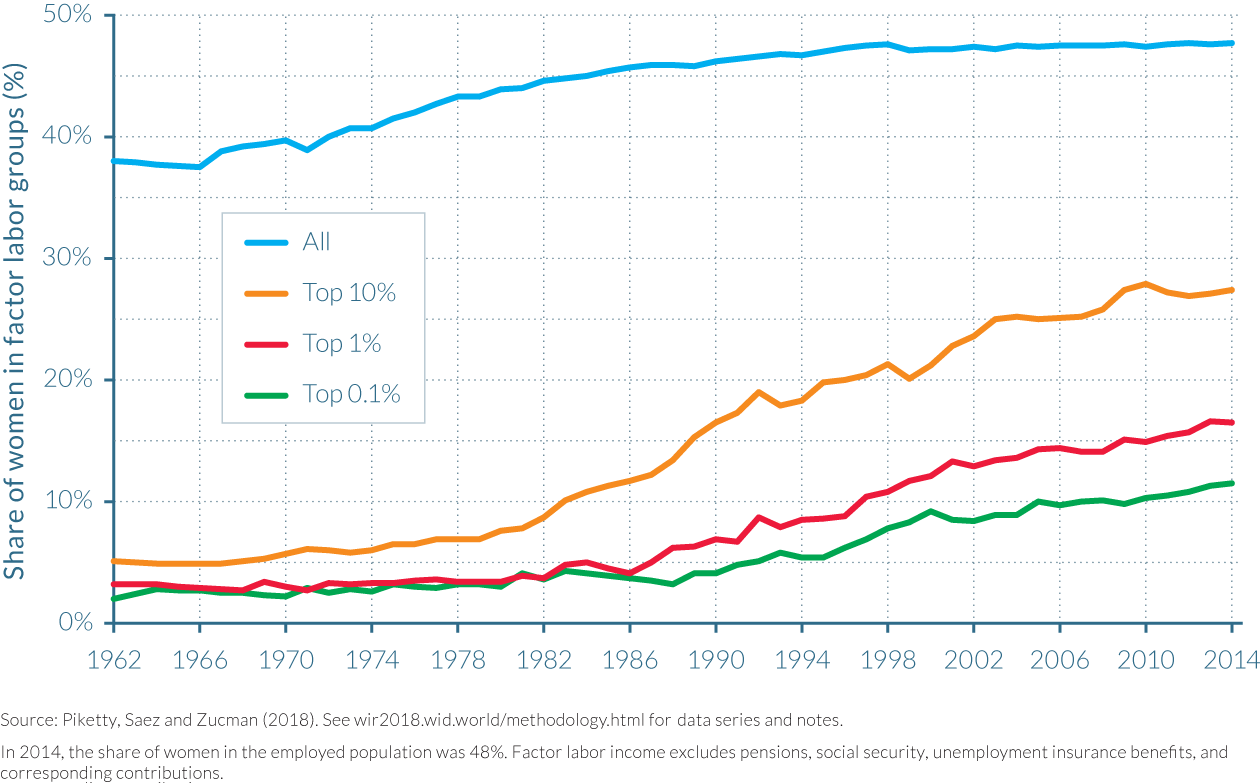

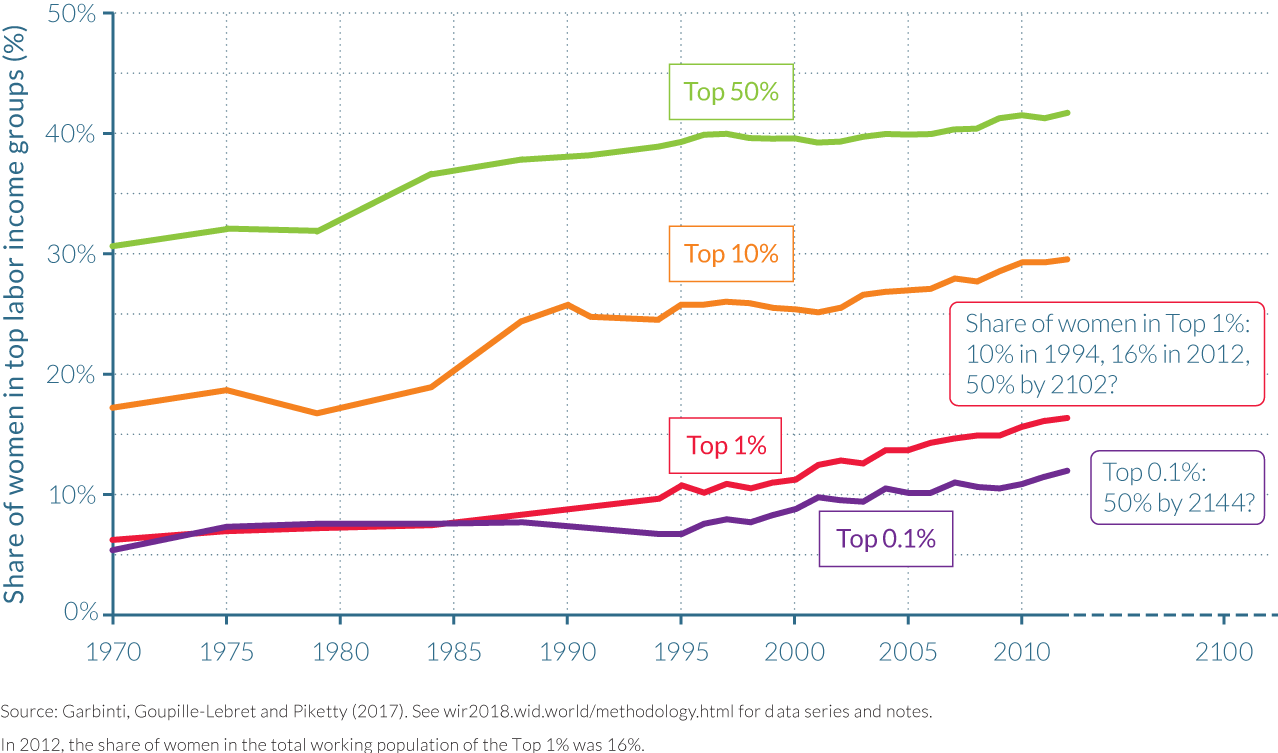

- Increased female participation in the labor market has been a counterforce to rising inequality, but the glass ceiling remains firmly in place. Men make up 85% of the top 1% of the labor income distribution.

Income inequality in the United States is among the highest of rich countries

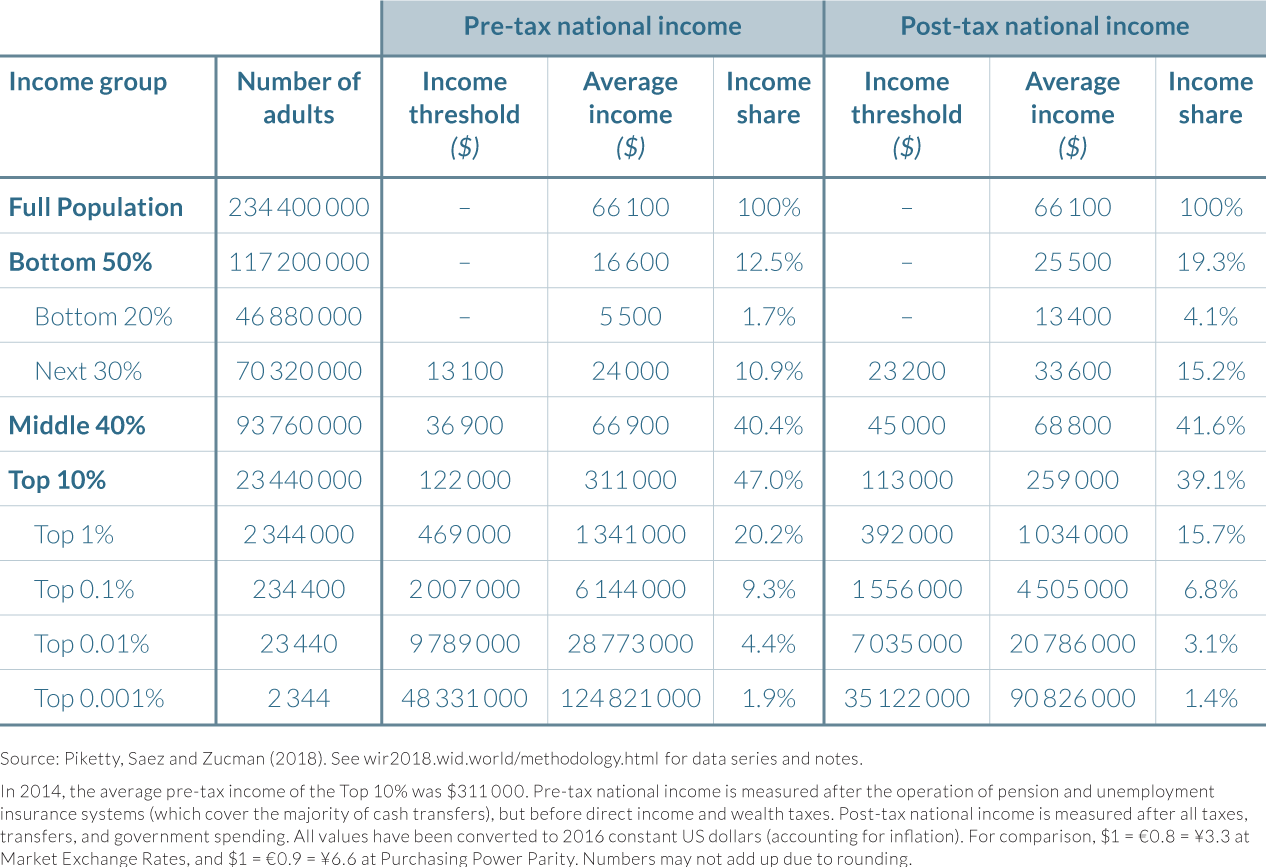

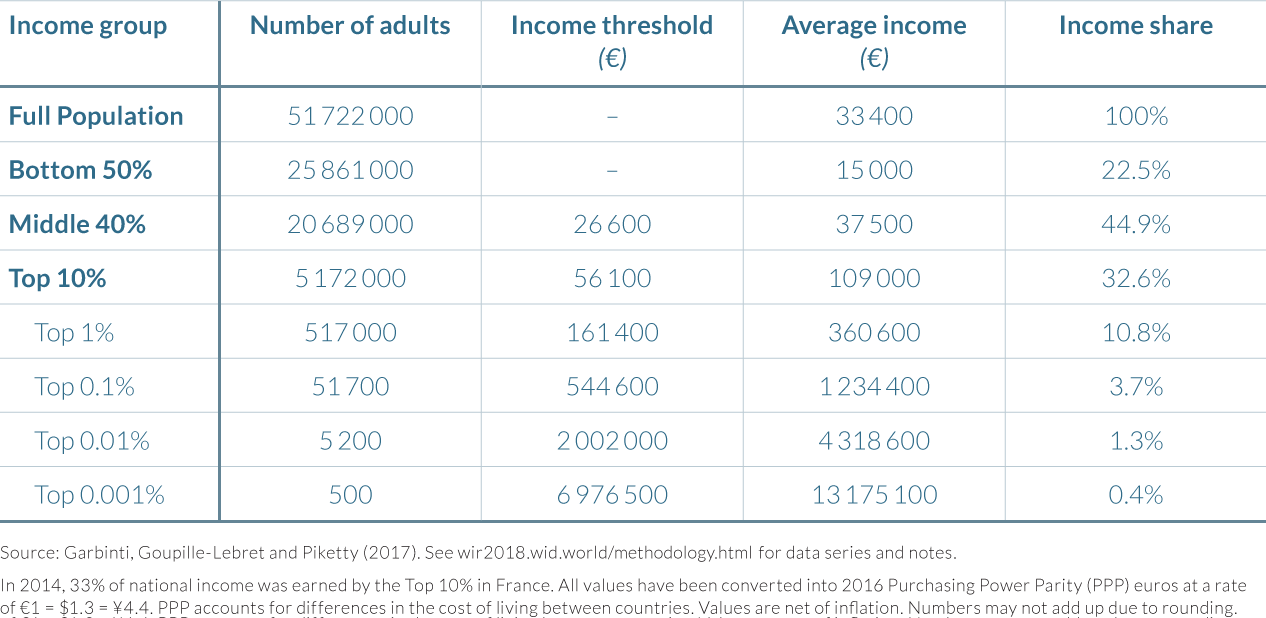

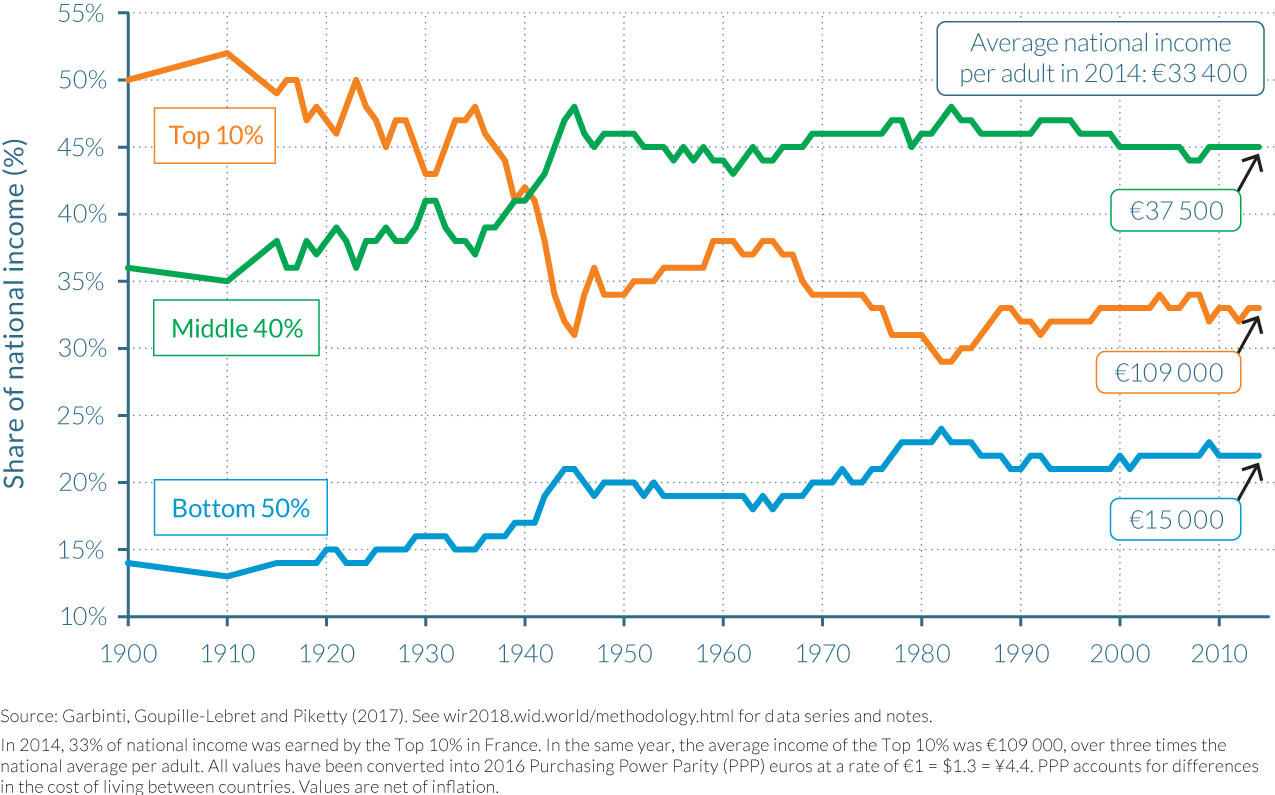

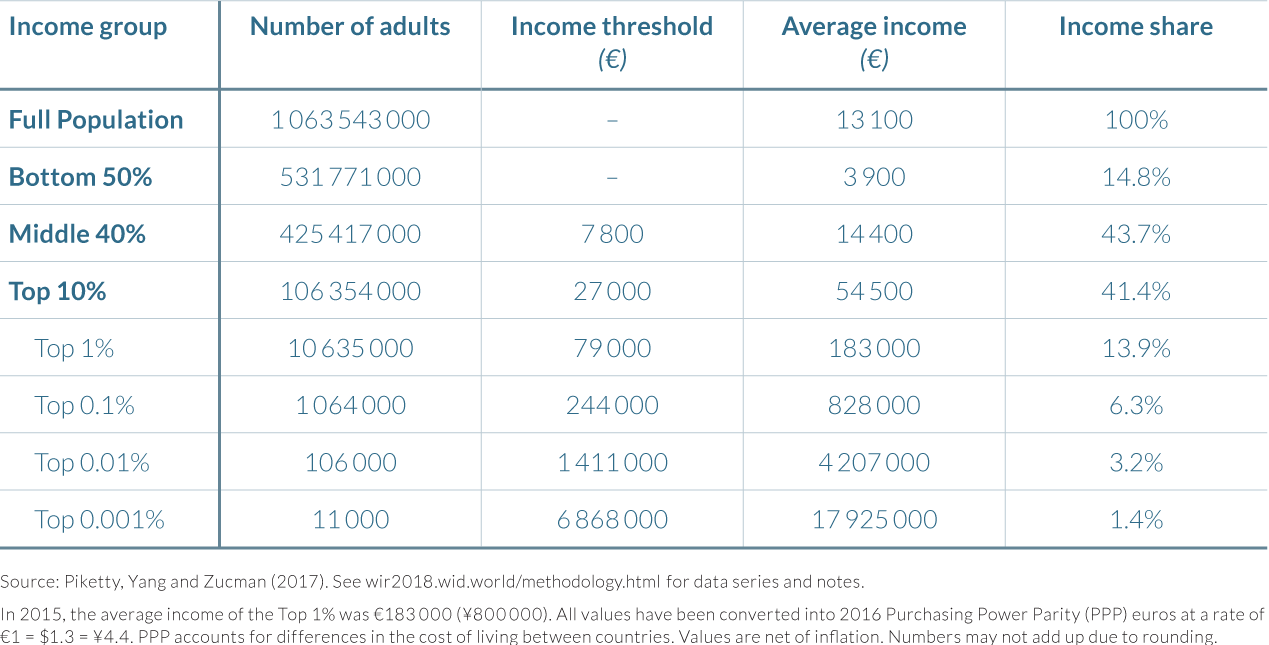

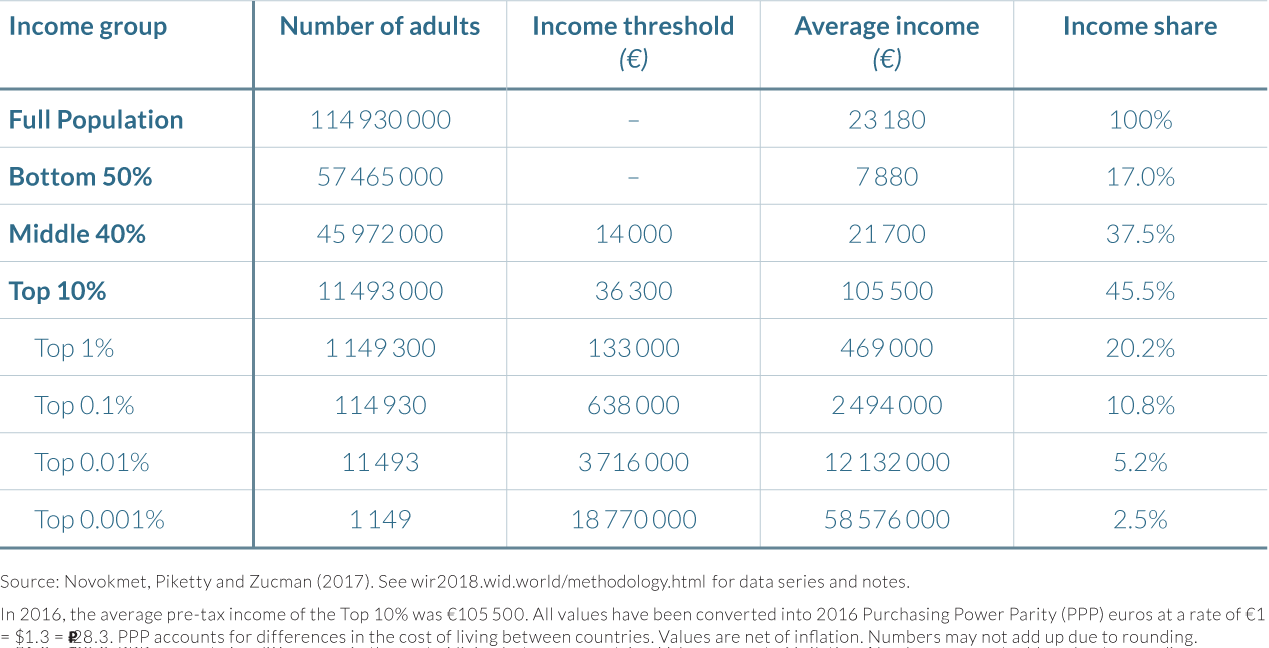

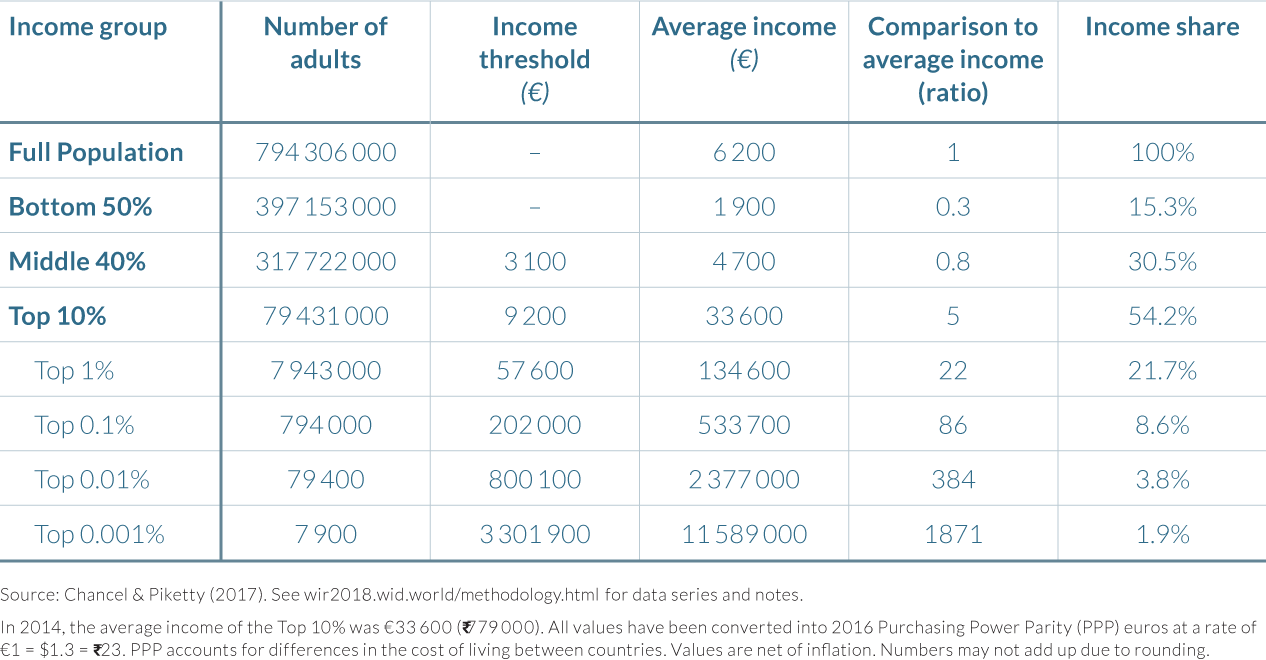

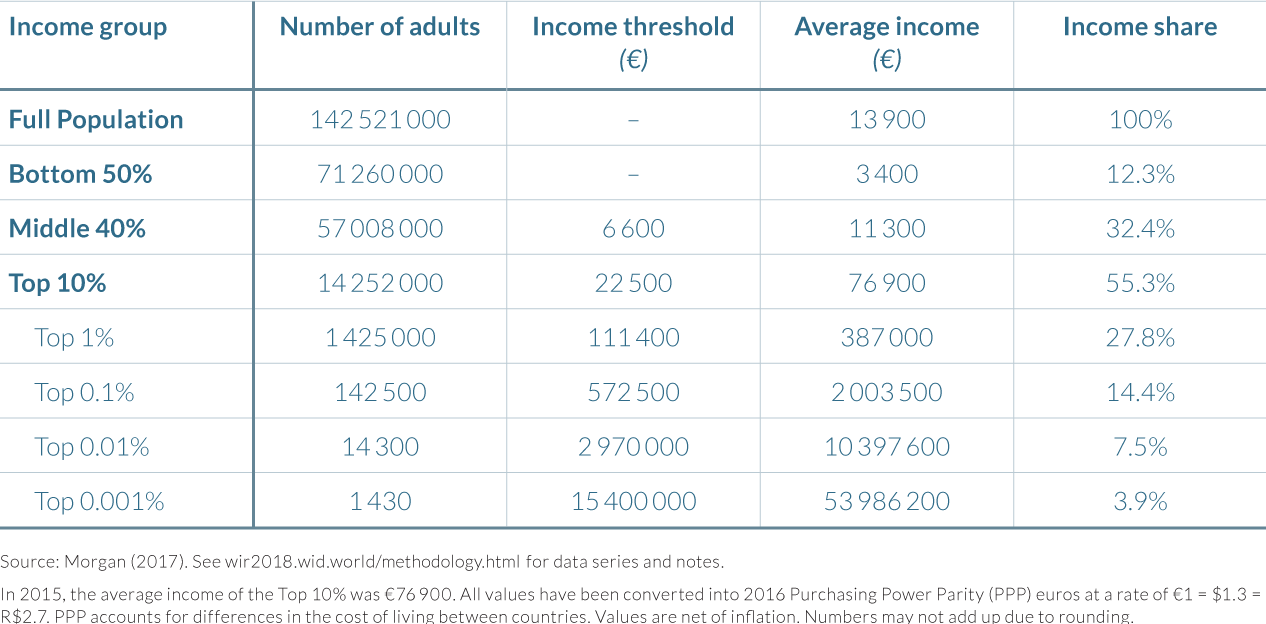

In 2014, the distribution of US national income exhibited extremely high inequalities. The average income of an adult in the United States before accounting for taxes and transfers was $66 100, but this figure masks huge differences in the distribution of incomes. The approximately 117 million adults that make up the bottom 50% in the United States earned $16 600 on average per year, representing just one-fourth of the average US income. As illustrated by table 2.4.1, their collective incomes amounted to a 13% share of pre-tax national income. The average pre-tax income of the middle 40%—the group of adults with incomes above the median and below the richest 10%, which can be loosely described as the "middle class"—was roughly similar to the national average, at $66 900, so that their income share (41%) broadly reflected their relative size in the population. The remaining income share for the top 10% was therefore 47%, with average pre-tax earnings of $311 000. This average annual income of the top 10% is almost five times the national average, and nineteen times larger than the average for the bottom 50%. Furthermore, the 1:19 ratio between the incomes of the bottom 50% and the top 10% indicates that pre-tax income inequality between the "lower class" and the "upper class" is more than twice the (1:8 ratio) difference between the average national incomes in the United States and China, using market exchange rates.

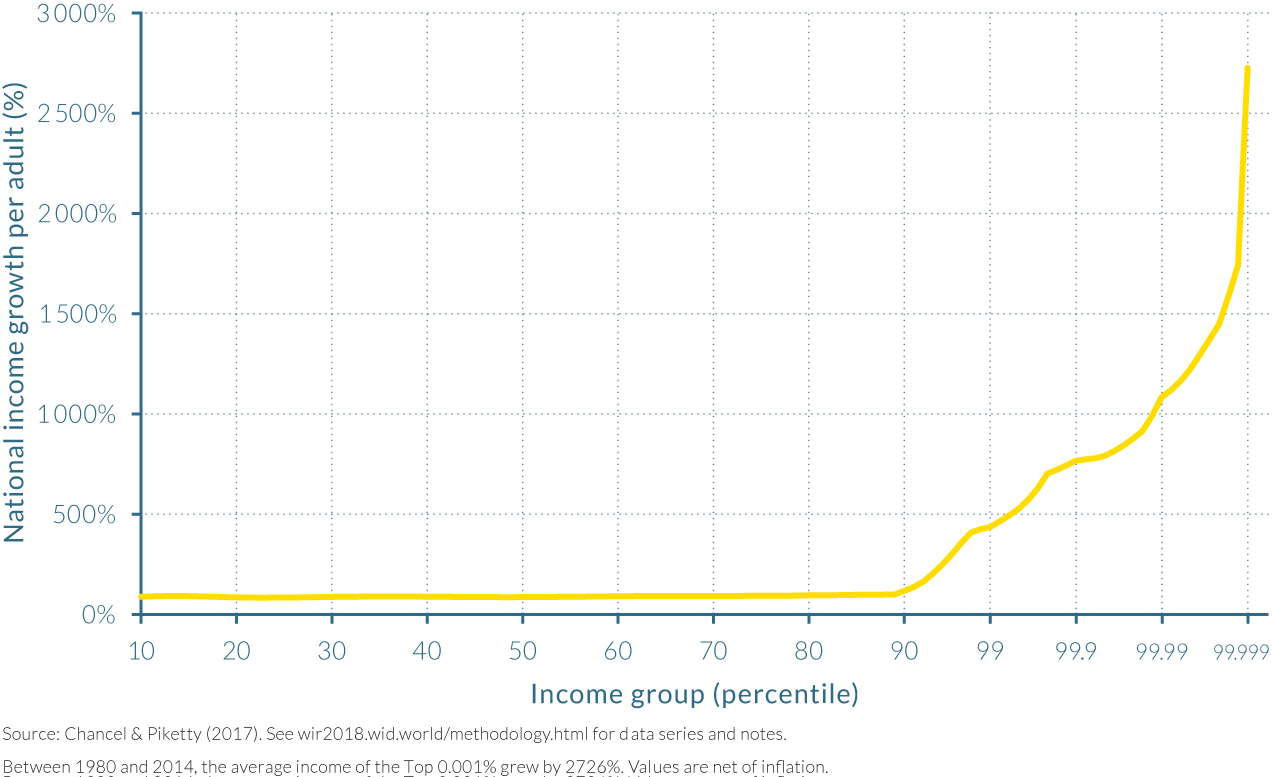

Income is very concentrated, even among the top 10%. For example, the share of national income going to the top 1%, a group of approximately 2.3 million adults who earn $1.3 million on average per annum, is over 20%—that is, 1.6 times larger than the share of the entire bottom 50%, a group fifty times more populous. The incomes of those in the top 0.1%, top 0.01%, and top 0.001% average $6 million, $29 million, and $125 million per year, respectively, before personal taxes and transfers.

As shown by Table 2.4.1, the distribution of national income in the United States in 2014 was generally made slightly more equitable by the country's taxes and transfer system. Taxes and transfers reduce the share of national income for the top 10% from 47% to 39%, which is split between a one percentage point rise in the post-tax income share of the middle 40% (from 40.5% to 41.6%) and a seven percentage point increase in the post-tax income share of the bottom 50% (from 12.5% to 19.4%). The trend is also of relatively large proportionate losses in income shares as one looks further up the income distribution, indicating that government taxes are slightly progressive for the United States' richest adults.

Table 2.4.1

The distribution of national income in the US, 2014

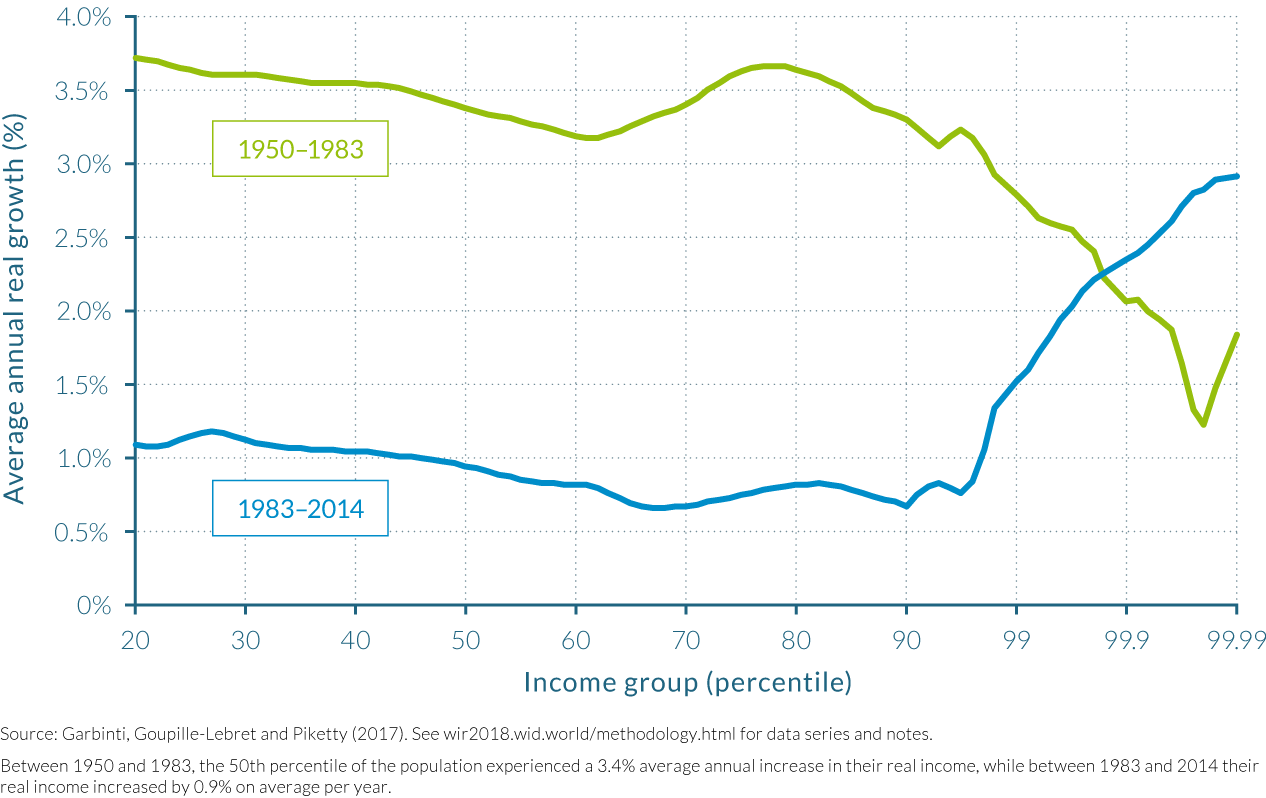

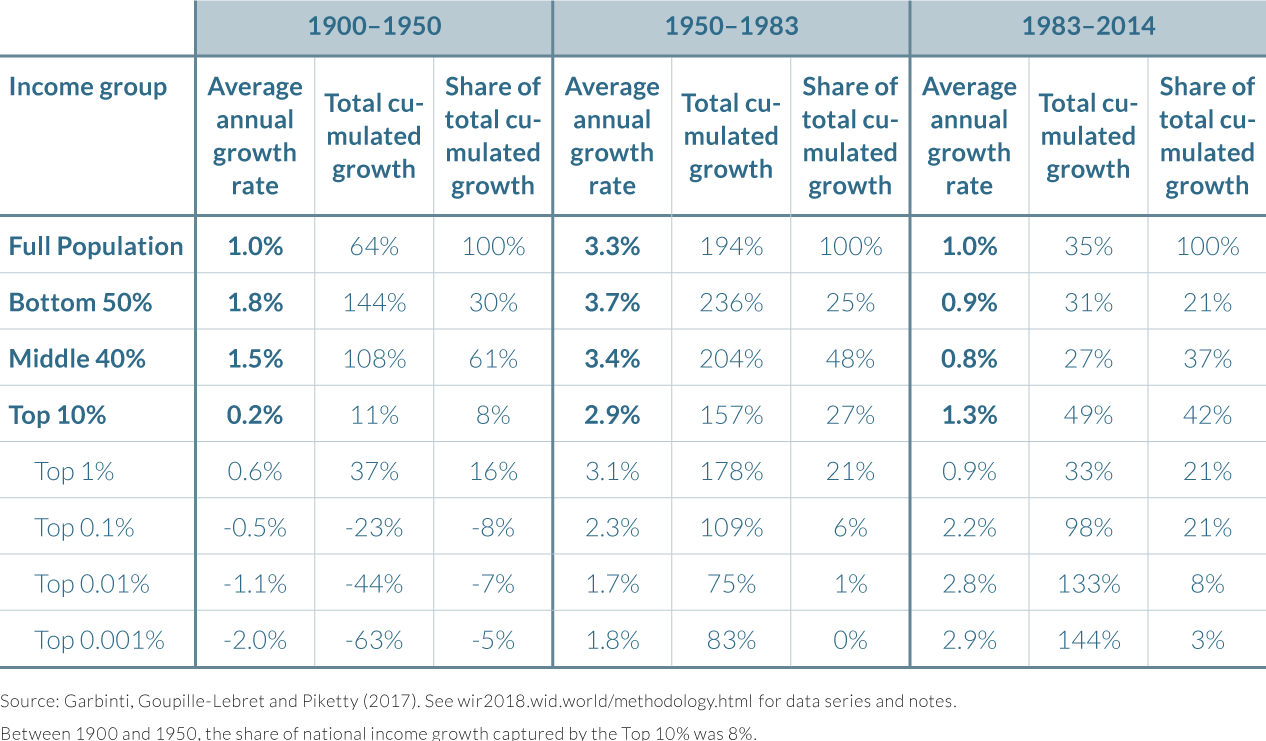

National income grew by 61% from 1980 to 2014 but the bottom 50% was shut off from it

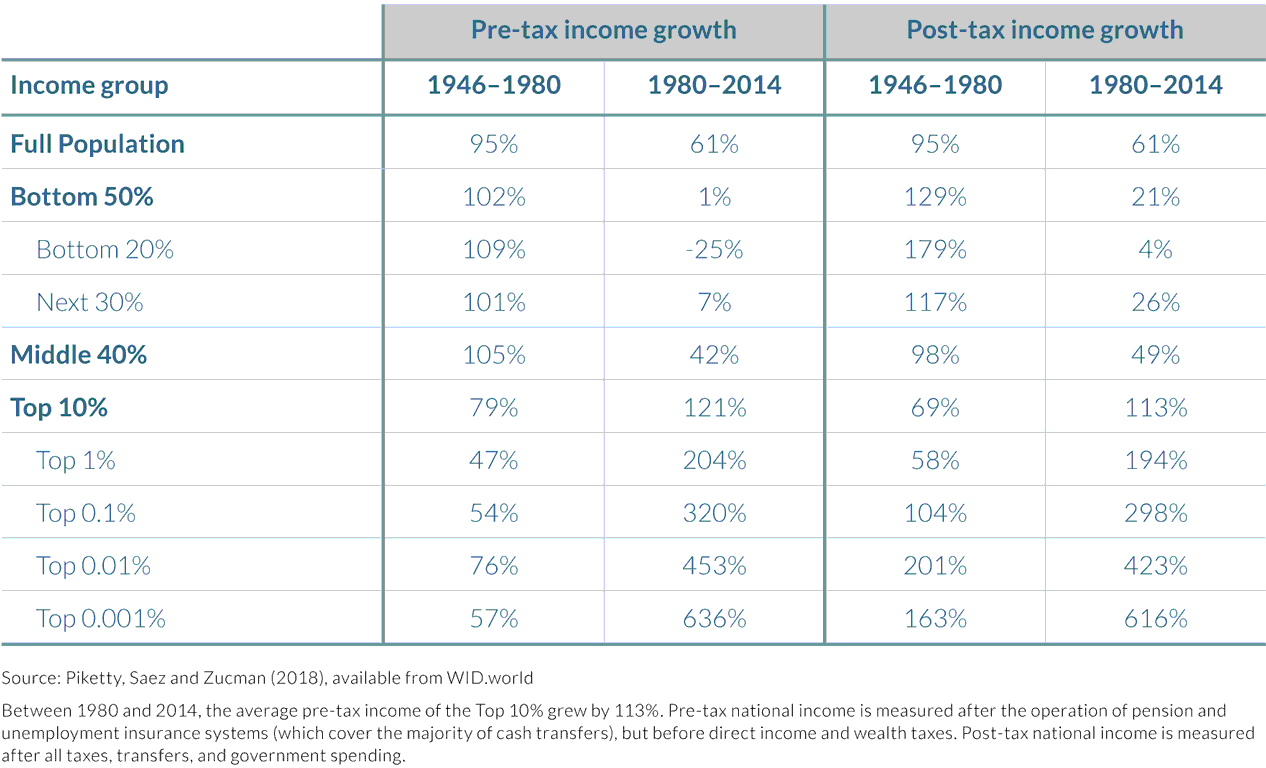

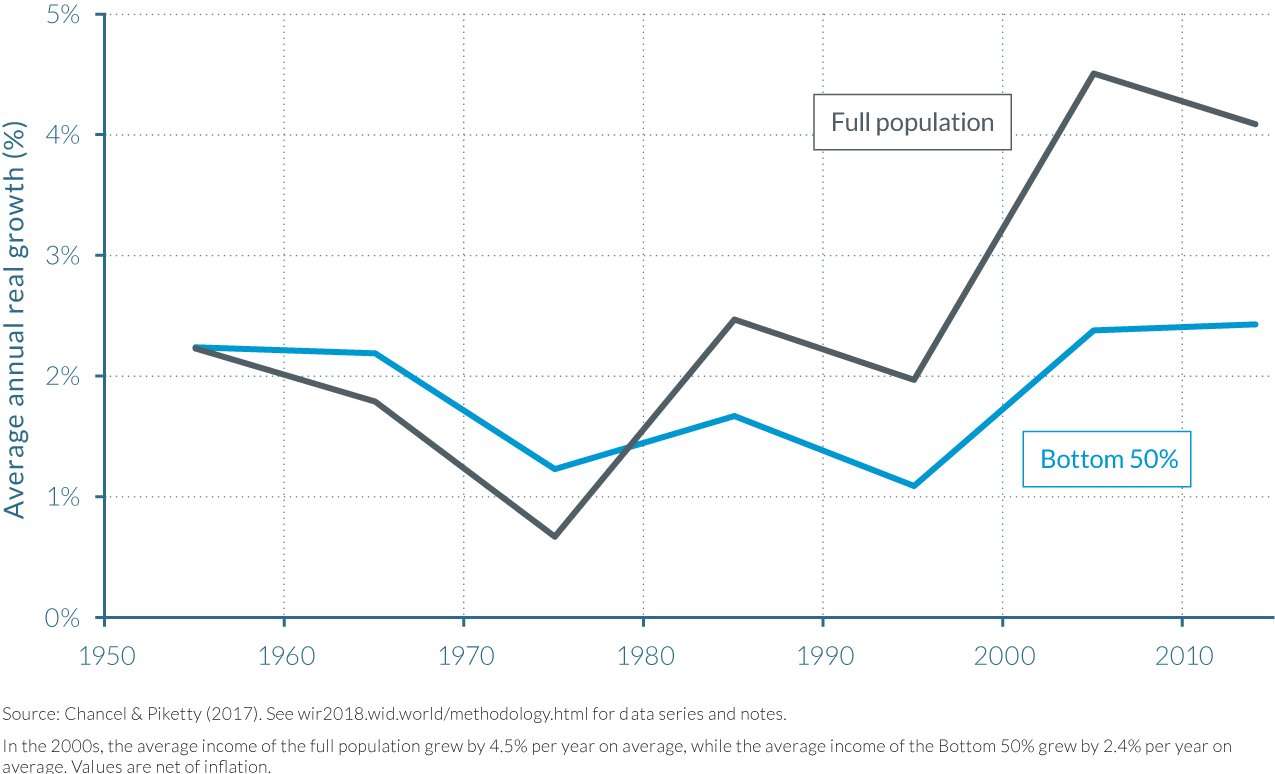

Income inequality in the United States in 2014 was vastly different from the levels seen at the end of the Second World War. Indeed, changes in inequality since the end of that war can be split into two phases, as illustrated by Table 2.4.2. From 1946 to 1980, real national income growth per adult was strong—with average income per adult almost doubling—and moreover, was more than equally distributed as the incomes of the bottom 90% grew faster (102%) than those of the top 10% (79%).10 However, in the following thirty-four-year period, from 1980 to 2014, total growth slowed from 95% to 61% and became much more skewed.

Table 2.4.2

The growth of national income since World War II in the US, 1946–2014